November Home Sales Forecast: The Housing Recovery’s Extended Adolescence

- After a weaker than expected October, Zillow expects existing home sales to fall 0.3 percent month-over-month in November, to 5.35 million units (SAAR).

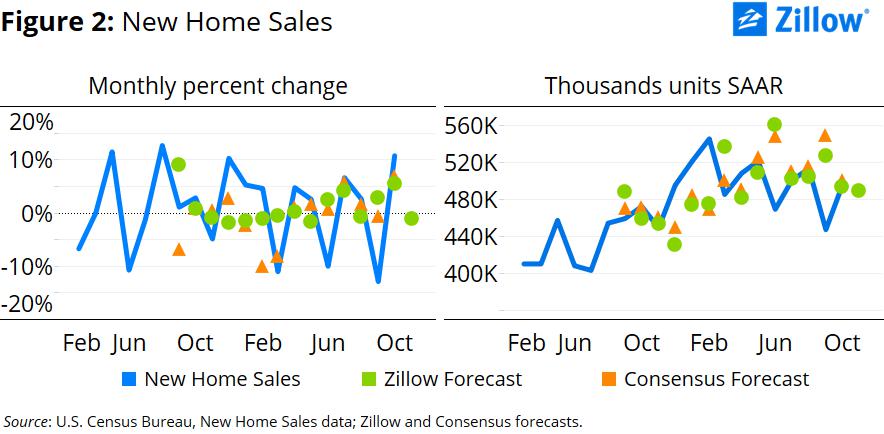

- For new home sales, Zillow expects a 1.2 percent drop to 490,000 units (SAAR).

- For much of the next year, we expect home sales to be flat.

Any parent of a wayward twenty-something is familiar with the concept of “extended adolescence,” the tendency of some young adults to fail at transitioning from the carefree aimlessness of adolescence into the more serious substance of adulthood. Looking back, 2015 appears to have been the housing recovery’s extended adolescence.

Like those directionless young adults who have held back household formation (at least in the popular imagination), home sales have so far failed to launch in 2015. And according to our November home sales forecast, we don’t expect that to change during the last two months of the year. But the question remains: Will sales finally takeoff in 2016?

Like many weary parents, we’re hopeful but skeptical.

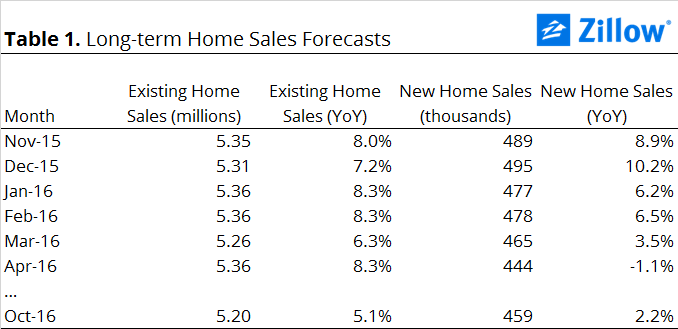

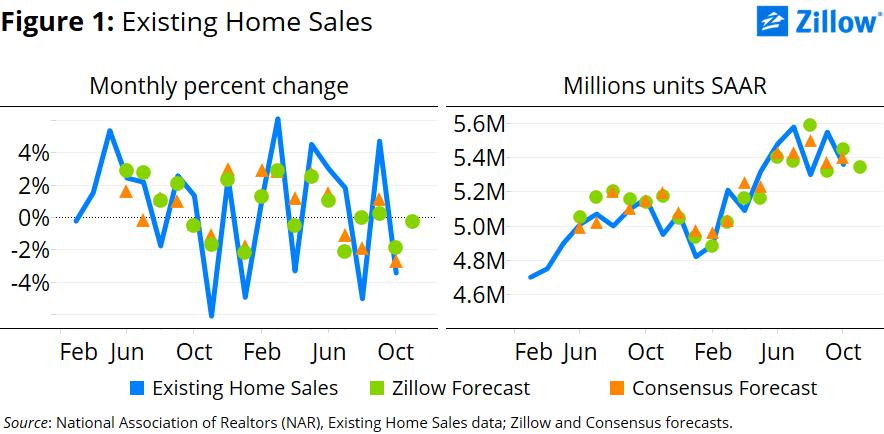

Our existing home sales forecast suggests that sales of existing homes should fall for the second month in a row in November, although by a much smaller margin than in October, declining 0.3 percent to 5.35 million units at a seasonally adjusted annual rate (SAAR) (figure 1). This would leave existing home sales essentially unchanged over 2015, although up 8 percent from November 2014.

The number of homes under construction is also rising, but remains below where it stood when financial markets crashed in September 2008 (and the financial crash itself occurred two-to-three years after home building first started to slow). Most new construction metrics (except price) suggest that new home construction is still at levels comparable to the early 1990s. Including multifamily construction makes the situation look somewhat less dismal: Multifamily starts per renter household have increased since the worst years of the recession, but are still below where they stood in the late 1990s.

One promising sign in the new construction market is the moderation in price growth in that segment of the market. After rising rapidly since 2010, the median price of new homes sold has stabilized in 2015, and has even declined year-over-year in two months so far this year. If this trend continues, it should imply better options for entry-level buyers.

Finally, interest rates held steady near historic lows in November, and it’s doubtful that, after a half decade at historic low interest rates, there is any demand out there that could reasonably be pulled forward by the prospect of small expected increases in interest rates this coming year. Any potential homebuyer waiting on the sidelines out of fear that interest rates will rise probably has already made the leap by now. Beyond December, rising interest rates could provide which is reflected in our longer term forecasts (Table 1).