The 5 Markets Most Likely to Be Impacted by New 2016 Conforming Loan Limits

- Conforming loan limits will increase in 39 counties nationwide in 2016, with the largest changes in the Boston, Denver, Nashville, San Diego and Seattle metro areas.

- The changes will push about 60,000 U.S. homes below the conforming loan limit.

- Denver will feel the largest impact of the changes – both in the number of jumbo homes and the share of homes requiring a jumbo loan.

Just before the country collectively left the office for Thanksgiving last week, the Federal Housing Finance Agency published updated 2016 Conforming Loan Limits. While a large majority of U.S. homes won’t be impacted, about 61,000 homes nationwide – including 50,000 homes in and around Denver, Seattle, San Diego, Boston and Nashville where loan limits shifted upward – may no longer need to be purchased with a jumbo loan.

The limits, updated annually and published at the county level, set the maximum loan amount for mortgages eligible for insurance and securitization by Fannie Mae and Freddie Mac, the government-sponsored entities that back a majority of mortgages originated nationwide. Mortgages above the limit are known as jumbo loans, and often (though not always) carry higher interest rates. When limits rise, fewer homes are likely to require a jumbo mortgage.

Conforming limits are set to rise in 39 counties nationwide, including 35 around the Boston, Denver, Nashville, San Diego and Seattle metros, and will remain the same as 2015 in the rest of the country. We’ve previously examined the share of homes nationwide likely to require jumbo loans, including how these shares vary within major metros. [1] This analysis examines the impact of different limits for 2016 in these five metros.[2]

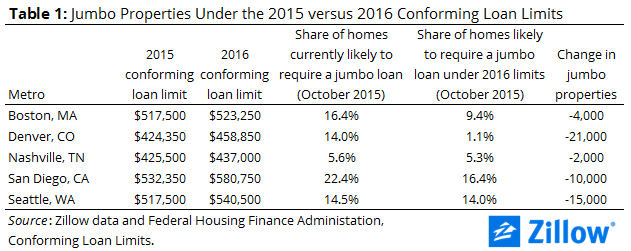

Of these five markets, Denver – where the conforming loan limit will increase from $424,350 to $458,850 – will experience the biggest impact, with about 21,000 fewer homes likely to no longer require a jumbo loan under the revised 2016 limits. In Seattle, roughly 15,000 fewer properties are likely to require a jumbo loan. San Diego (10,000 fewer properties likely to require a jumbo loan), Boston (4,000 fewer properties likely to require a jumbo loan) and Nashville (2,000 fewer properties likely to require a jumbo loan) round out the list (table 1).

[1] We compare the share of properties requiring a jumbo loan in October 2015 under current conforming loan limits, and the share of properties requiring a jumbo loan in October 2015 if the 2016 conforming loan limits were in force. We continue to assume that these homes are purchased with a 25 percent down payment, which is typical for borrowers seeking jumbo loans on Zillow.

[2] The remaining 11,000 homes nationwide outside of the homes in the five metros noted are in the Salinas (CA), Napa (CA), Santa Rosa (CA), and Boulder (CO) metro areas which also had small increases in the conforming loan limit.

[3] One limitation of this analysis is that home values are very likely to increase in these areas before the new loan limits come into force on January 1, 2016. In a place like Denver or Seattle, where home values are increasing at a pace of around 0.4 percent per month, some properties currently valued below the loan limit – but close to it – may appreciate in value enough to cross above the threshold again on or before Jan. 1.