Conforming Loan Limits Jump by Record Amount To Keep up with Rapid Home Price Appreciation

- The baseline conforming loan limit increased by the largest dollar amount and percentage on record for 2022, in order to keep up with rapid home value appreciation.

- There are 159 counties that have a higher loan limit than the national baseline.

- In January 2022, almost 3 million fewer homes would have required a jumbo loan under the higher limit compared to December 2021.

The conforming loan limit rose to $647,200 in most counties for 2022, up 18% (almost $100,000) from 2021 – the largest one-year increase ever as regulators sought to keep pace with a housing market appreciating at a record pace.

Conforming loan limits – set annually by the Federal Housing Finance Agency – represent the largest amount mortgage lenders can loan to borrowers and still sell the loans conventionally to Fannie Mae and Freddie Mac, quasi-governmental agencies that are by far the nation’s two largest mortgage securitizers. Borrowers seeking loans above these limits will typically need to take out a so-called “jumbo loan,” which can sometimes come with additional expenses and/or more rigorous qualification standards.. The 18% bump in loan limits roughly coincided with home values that grew 19.6% in 2021, according to the Zillow Home Value Index. The next-highest loan limit increase was in 2006, when the limit increased by 15.9% from 2005 (at the time, a $57,350 bump).

And in 159 U.S. counties determined to be medium- and high-cost (accounting for around 5% of all counties nationwide, but more than 20% of the U.S. population) the conforming loan limit is higher. In 57 medium-cost counties, the limit was increased by varying levels above the $647,200 base limit, but below the absolute maximum limit of $970,800 imposed in the nation’s 102 highest-cost counties – largely concentrated in the nation’s most expensive metro areas along the coasts and mountain west.

Given the higher limits, the number of homes valued highly enough to require a jumbo loan (assuming a 20% down payment) fell by roughly 2.9 million from December 2021 to January 2022, when the new limits took effect. This shows the importance of continual increases in the conforming loan limit, especially as home values continue to rise so quickly. Rapid monthly home value appreciation is already starting to reduce the number of homes that would qualify for a conforming loan. In February, the number of homes worth enough to potentially require a jumbo loan (again, assuming a 20% down payment) rose by roughly 217,000 from January. And because we anticipate the spring home shopping season to be very competitive – pushing home prices even higher – that trend will continue.

Because conforming loan limits are only increased once per year, in January, buyers shopping for more-expensive homes should consider the time of year they are looking to buy – especially if they are worried about qualifying for stricter jumbo loan mortgages. For example, a buyer seeking a $700,000 home in December 2021 would have needed to put down at least 21.7% to get their loan amount under the typical 2021 loan limit and avoid a jumbo loan. But in January 2022, the down payment necessary to obtain a standard mortgage for less than the conforming loan limit was only 7.5%, owing to the big jump between 2021 and 2022 baseline limits. So shopping off season, at the very beginning of the year, might make the home buying experience a little easier for buyers in markets where a large share of homes are likely to require jumbo loans.

Another consideration for buyers shopping in higher cost markets is the recent increase in upfront fees on ‘super conforming’ loans. A super conforming loan is a loan in a higher-cost area where the conforming loan limit is higher than the national baseline of $647,200, but below the area limit. So for example, a $700,000 loan in a place like Honolulu County, HI, that has a conforming loan limit of the maximum $970,800, would be considered a super-conforming loan. This new fee increase would add an upfront cost of 0.25%-0.75% of the entire loan – totaling between $1,750 and $5,250 for a loan of that value, which can be a significant addition to a laundry list of other buying costs. The good news is that this fee will not apply to first-time buyers who have an income at or below the area median income, potentially saving some first-time buyers thousands of dollars.

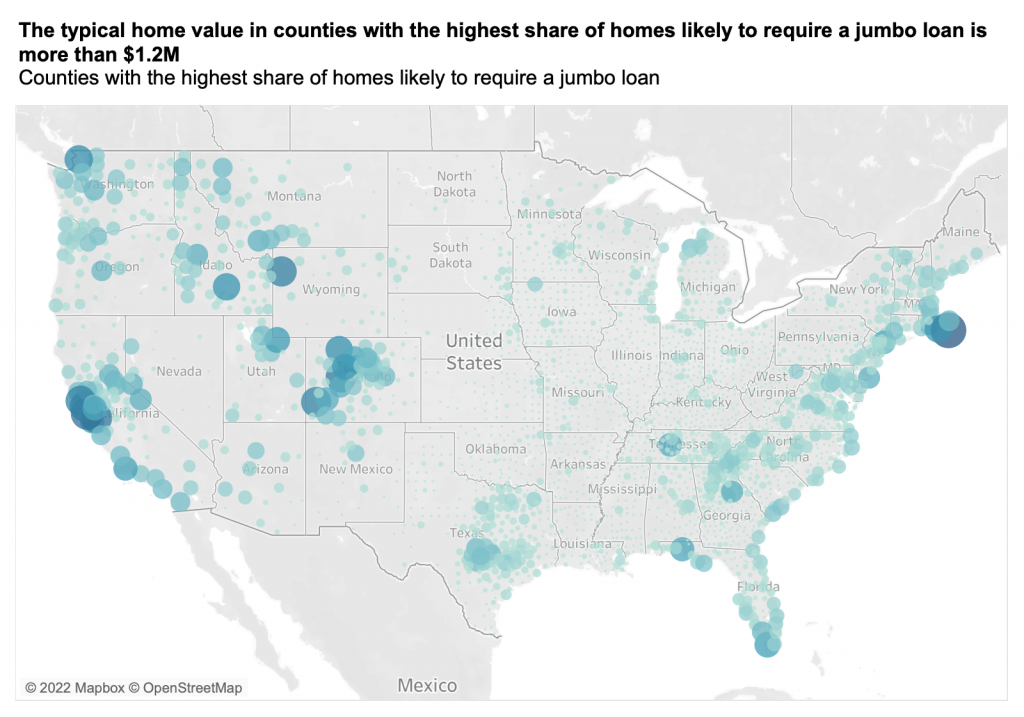

Counties with the highest share of homes likely to require a jumbo loan (again, as always, assuming a 20% down payment) are: Nantucket County, Mass.; San Mateo County, Calif.; Santa Clara County, Calif.; San Francisco County, Calif.; Pitkin County, Colo.; Teton County, Wyo.; and Marin County, Calif. In each of these areas, a clear majority – more than 60% – of homes are worth enough to require a jumbo loan, and the typical home value in each is more than $1.2M.