As California Debates Rent Control, More Supply Is Contributing to a Slowdown in Rents

Perhaps no part of the country has seen rents rise as quickly in recent years as California, driven by population growth in the Golden State’s booming job centers and, in some areas, restrictive building codes that hamper the ability for cities and towns to add new supply to meet this demand. Rent affordability across the state is historically poor, and Californians are searching for policy solutions that might bring some relief.

Among the solutions being considered is Proposition 10, which would repeal a decades-old statewide ban on local governments enacting rent control, potentially paving the way for some local governments to enact new limits on how fast rents can increase. Although popular among voters, most economists say that blanket rent controls ultimately limit new construction, reducing the number of rental units on the market and pushing up rents in the long term.

But beyond the ongoing policy debates, the undercurrents of the California rental market are shifting on their own in response to more fundamental market forces. In the past two years, rent growth has slowed sharply across the state. And the slowdown in rent growth has been particularly large in the communities that have succeeded in adding the most new housing supply.

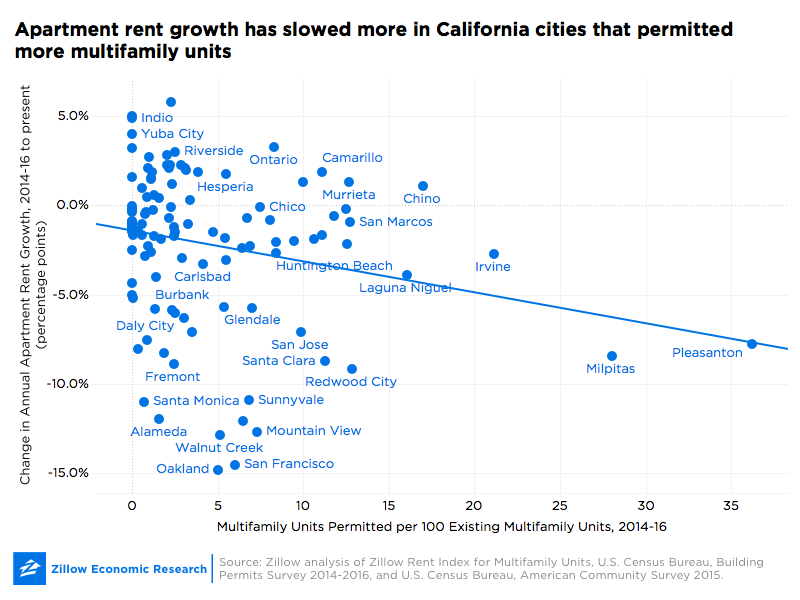

Zillow compared the number of new apartments permitted[1] in the past few years[2] to the slowdown in rents since that time. Across California cities for which we have data, those with the strongest permitting activity – which, at the median, permitted 11.5 new apartments for every 100 existing multifamily units – saw the average pace of annual rent appreciation slow by 2.0 percentage points. Those with the fewest new apartments permitted – which, at the median, permitted no new apartments – saw the average pace of annual rent appreciation slow by 0.9 percentage point over the past few years.

For example, Silicon Valley communities Milpitas and Pleasanton experienced the most aggressive permitting activity between 2014 and 2016 – respectively permitting a total of 28 and 26 apartments for every 100 existing multifamily units. Annual rent growth in those areas has since fallen approximately 8 percentage points, to the current annual pace of 2.4 percent and 0.2 percent, respectively.[3]

As Californians embark on an important debate about how to address the state’s housing crisis, the most recent data shows that rent growth does ultimately cool when new supply is allowed to catch up. Where supply has been allowed to catch up, rents are slowing or falling. Given the state’s steadily strong demand for housing, policies that reduce the rental supply can be expected to push up rents.

[1] Total new multifamily units permitted in 2014, 2015 and 2016 according to the U.S. Census Bureau’s Building Permits Survey.

[2] Median annual pace of growth in apartment rents in 2014, 2015 and 2016, controlling for the number of existing multifamily units in the city in 2015 according to the 2015 American Community Survey.

[3] Median annual pace of growth in apartment rents for the 12 months ending in August 2018, the most recent data available.