Case-Shiller September Results and October Forecast: Underbuilding Continues to Take a Toll

The primary Case-Shiller indices paint a picture of a national housing market that’s largely stable and maybe even a bit boring from 50,000 feet, with home prices growing at roughly the same pace for the past year or more.

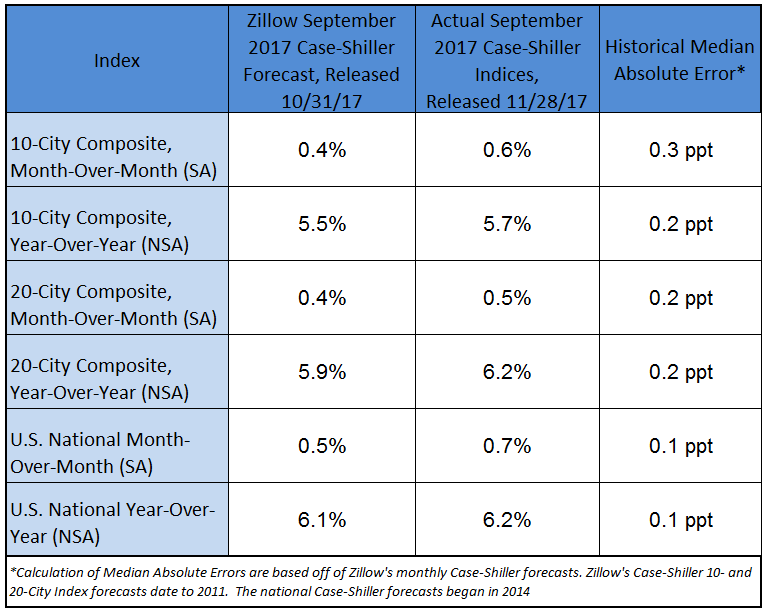

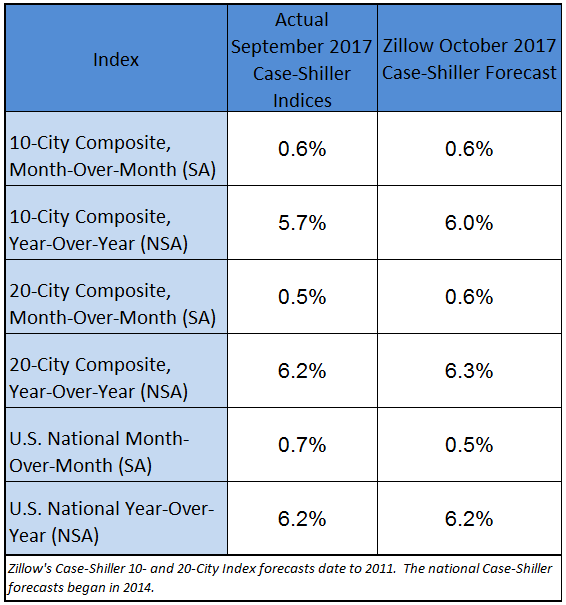

The U.S. National Index for September showed an annual increase in home prices of 6.2 percent. The month-over-month increase from August was 0.7 percent.

The 10-city composite gained 5.7 percent annually and 0.6 percent from August to September, while the 20-city composite grew 6.2 percent annually and 0.5 percent month-over-month. Seattle, Las Vegas, and San Diego continued to post the largest annual gains among the 20-city composite, climbing 12.9 percent, 9 percent and 8.2 percent, respectively.

But the real action is on the sidelines. Demand is coming first and foremost from buyers in the entry-level and mid-market segments, but available inventory is largely concentrated at the high end – causing the nation’s most affordable homes to grow in value at more than twice the pace of homes at the top of the market. The past two months have shown promising signs of life from builders who have had difficulty meeting intense demand in the face of rising land, lumber and labor prices – but it’s going to take a lot more than two good months to erase a housing deficit accumulated from years of underbuilding.

Income growth has been decent lately, but it has not kept pace with rising housing costs, giving renters in particular the feeling of trying to hit a moving target as they attempt to save a down payment for the jump into homeownership. There’s a lot happening just under the surface of this otherwise fairly predictable market, and not all of it bodes well as we look into 2018.