Zillow: CPI Shelter Forecast, December 2025

Update Following 01/13/2026 CPI Release:

The December CPI release showed housing inflation following a gradual downward trajectory. After recent distortions, this print aligned with our expectations for continued declines in both major housing measures.

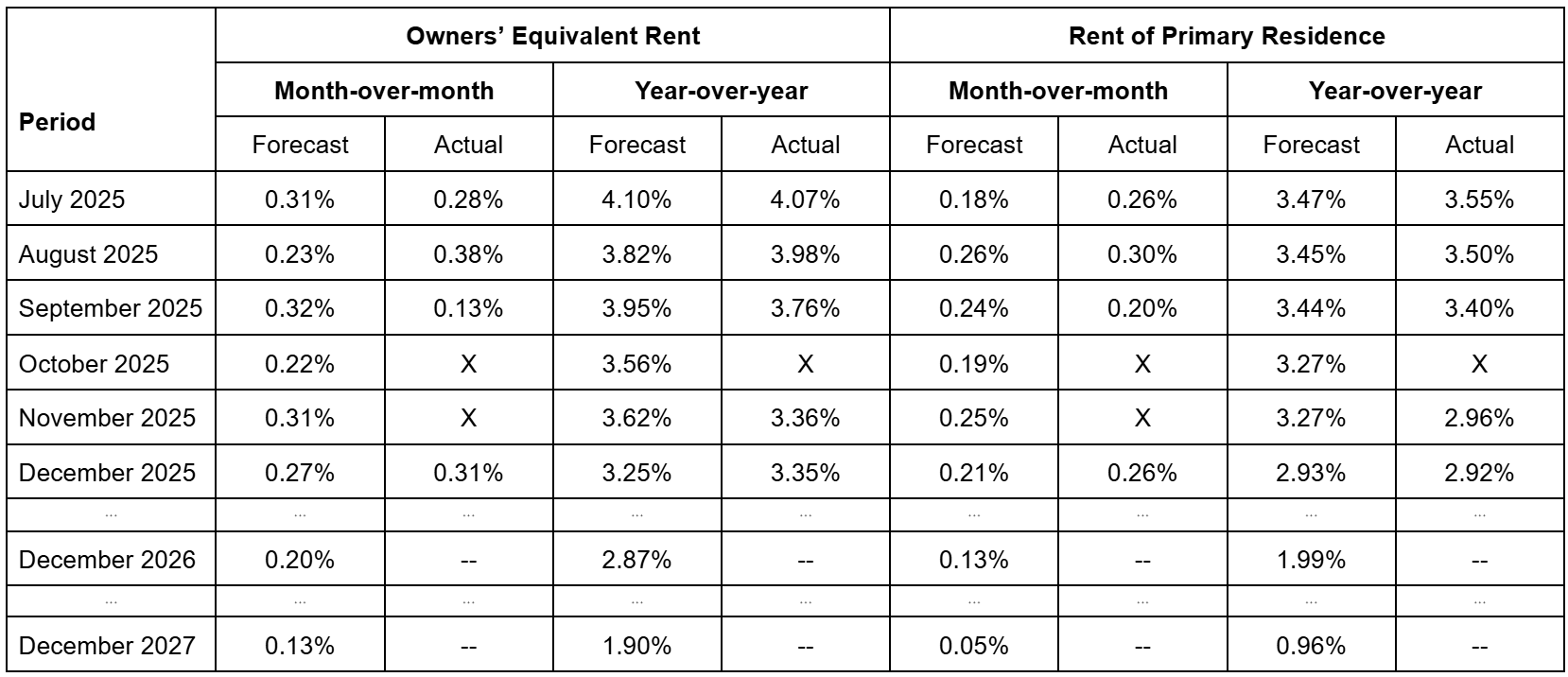

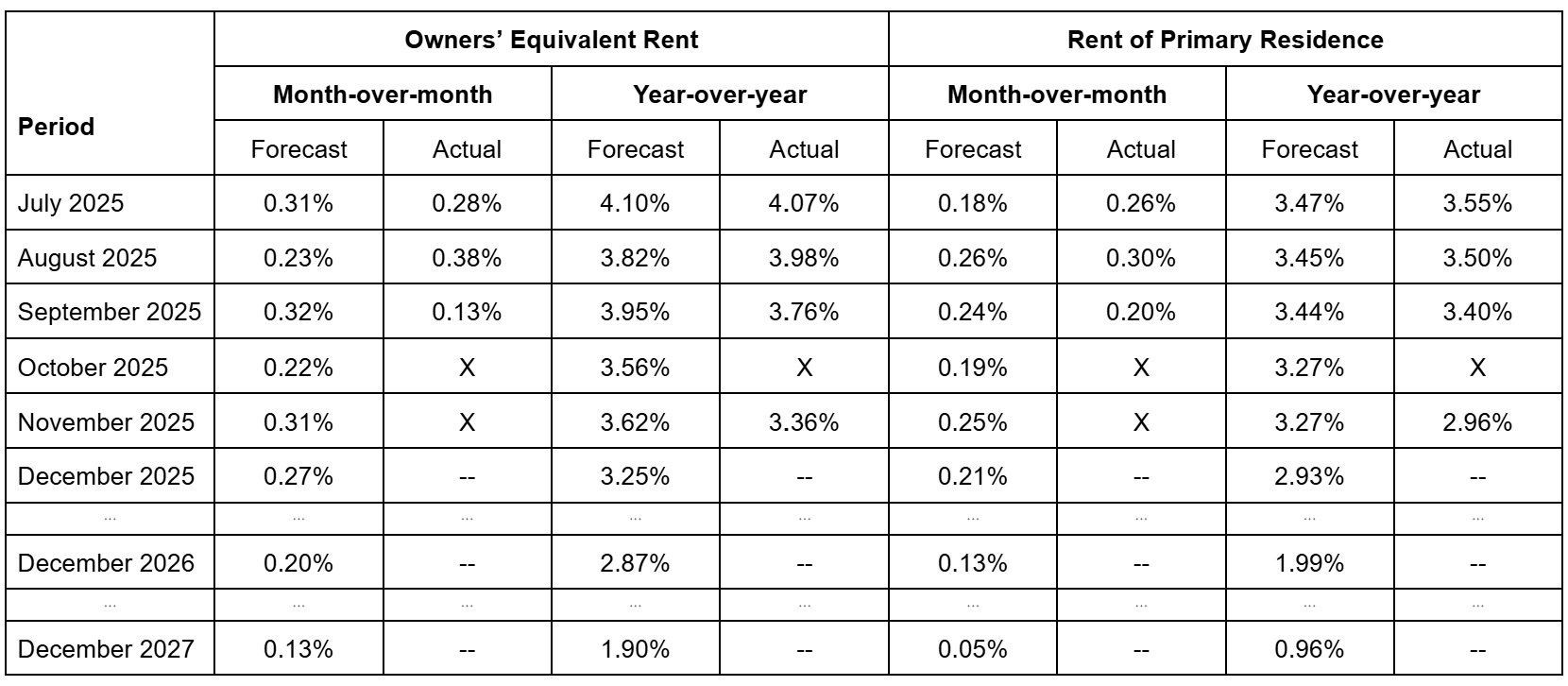

Seasonally-adjusted CPI for Owner’s Equivalent Rent (OER) increased 0.31%, consistent with our expectation of 0.27%. The index rose 3.35% over 2025, versus our expectation of 3.25%.

Seasonally-adjusted CPI for Rent of Primary Residence rose by 0.26%, slightly above our expectation of 0.21%. The index rose 2.92% over 2025, versus our expectation of 2.93%.

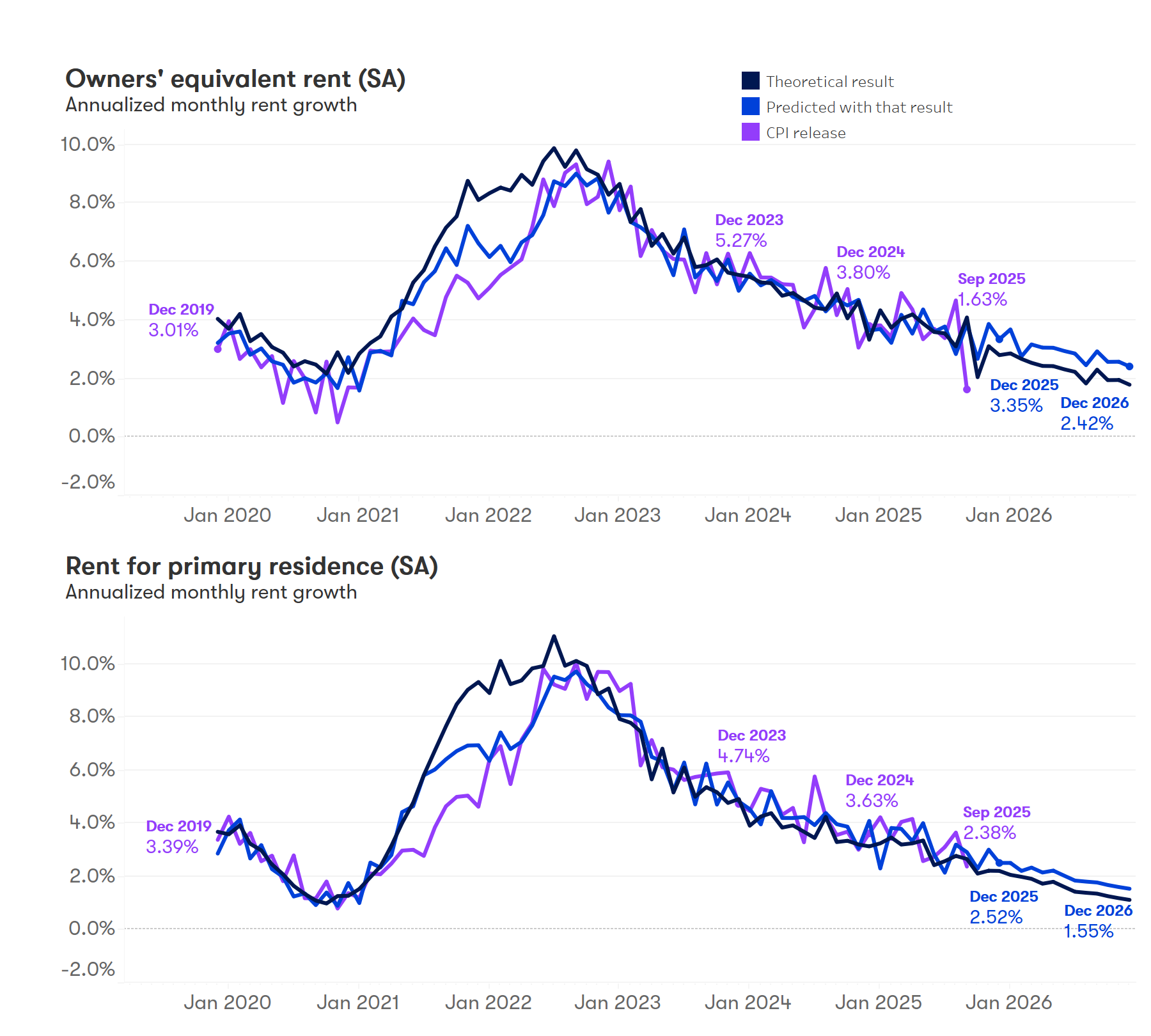

Housing inflation resumed its expected trend in December. Despite some extra heat relative to the last two prints, OER and Rent of Primary Residence both fell well within our bands based on data prior to shutdown-related disturbances. Both also saw declines, however slight, in year-on-year growth. We expect further deceleration ahead as low growth in market rents continues to take pressure off renter costs. Other smaller components of the Shelter category rose faster than the larger components, with spending on hotels up 3.5% and household insurance up 1.0% for the month, driving the summary number higher to 0.40%.

________________________________________________________________________________

New shelter inflation numbers from the Bureau of Labor Statistics are scheduled to be released on Tuesday, January 13, 2025 at 8:30 ET.

October and November CPI shelter readings were distorted by a data collection gap. Rent levels carried forward from April mechanically produced zero shelter inflation in October and reduced the measured two-month change by roughly half. To avoid embedding this mechanical noise in our outlook, our December forecast uses a three-month horizon anchored to September as the last representative month-on-month observation. This approach abstracts from temporary measurement artifacts while preserving the clear underlying trend in housing inflation.

Key Takeaway

CPI housing inflation measures are expected to continue moderating into 2026, driven by the deceleration in market rents. Expectations for a stagnant job market also contribute to a flatter outlook for housing costs.

The Forecast

Owners’ Equivalent Rent (OER)

Monthly outlook: Owner’s Equivalent Rent, which measures what homeowners would theoretically pay to rent their own homes, is projected to have increased 0.27% in December 2025 (95% confidence interval: 0.13% – 0.42%) in line with the gradual slowing over the year. This would bring the annual increase in the index to 3.25%, a moderation from 3.36% in November. We expect the monthly growth to continue trending downward to a 0.20% pace over the next year.

Annual outlook: We forecast OER to rise 2.9% over 2026, about a half-point slowdown from the 2025 increase. The index is expected to continue decelerating into 2027, increasing just 1.9% over the year.

Rent of Primary Residence

Monthly outlook: Rent of Primary Residence, which tracks rent payments, is projected to have increased 0.21% in December 2025 (95% confidence interval: 0.02% – 0.39%), consistent with the downward trend over the year. This would bring the annual increase in the index to 2.93%, a moderation from % in November. We expect the monthly growth to continue trending downward to a 0.13% pace over the next year.

Annual outlook: We forecast the Rent of Primary Residence index rise 2.0% over 2026, about a full point slowdown from the 2025 increase. The index is expected to continue decelerating into 2027, increasing just 1.0% over the year.

Market Rents

Single-family: Zillow’s expectations for on-market rent growth for single-family units remained relatively unchanged: single-family rents are expected to rise 1.6% in 2026, slowing to 1.1% growth in 2027.

Multifamily: Zillow’s expectations for on-market rent growth for apartments was revised upward: multifamily rents are expected to rise 0.2% in 2026, followed by a 0.8% decline in 2027.

The shelter components of the CPI continue to increase at a faster pace than these on-market rent trends, reflecting not only new lease pricing but also rent changes for renewing and longer-term tenants.

Methodology

These forecasts are based on predictions from a model that makes explicit the relationship between on market rents (measured by the Zillow’s Observed Rent Index) and the shelter components of the Consumer Price Index (CPI).

The model incorporates:

- Expected on-market rent growth (Zillow’s Observed Rent Forecast, ZORF)

- Assumptions about how landlords adjust rents at lease renewal

- Renter mobility rates, which determine what share of tenants face a market rent increase.