The Fed Watch: The Impact of Uncertainty

- National homeowner affordability eroded dramatically, introducing a whole new uncertainty, and rate sensitivity, to buyers.

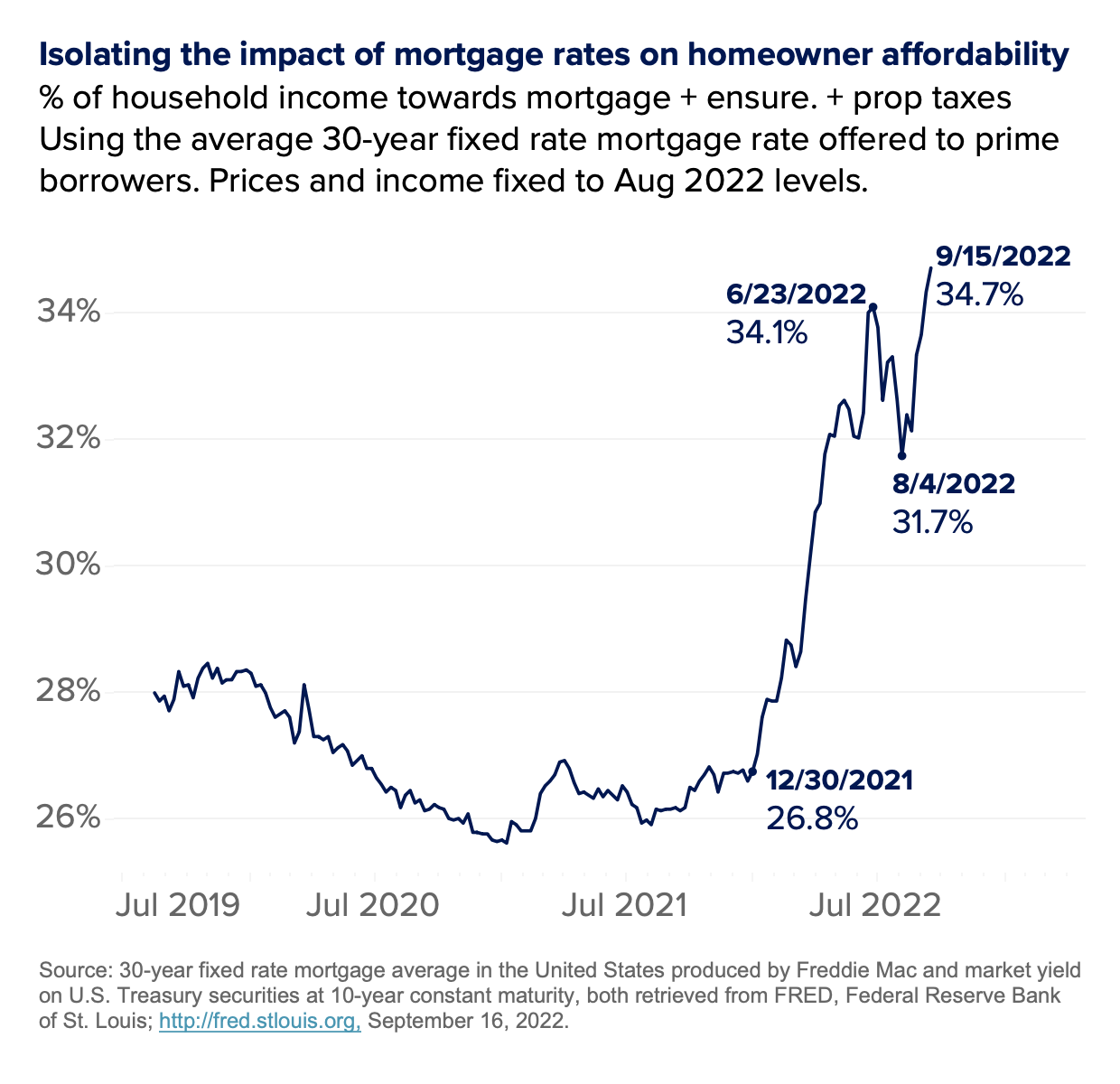

- Weekly swings in mortgage rates means swings in homeowner affordability. The share of income spent on the mortgage payment, taxes, and insurance has exceeded 34% – above the simplified rule-of-thumb of around a 3rd of income – only to fall below 32% six weeks later, and burst back up to 36% six weeks after that (current).

- Buyer hesitancy and the impulse to wait for price declines could be contributing to low demand.

- To watch mortgage volatility in many ways is to watch the much-debated calibration of monetary policy to market data, both prices and jobs, and the reactions of financial markets.

Housing affordability in the U.S. is the worst it’s been in decades after mortgage rates shot up following two years of low-rate-plus-pandemic-fueled price growth. But that’s not the only thing making it hard for buyers to move forward. Mortgage rate volatility, the result of uncertainty introduced by the sea change in Federal Reserve policy early in the year, also plays a big part. Resolve the uncertainty and a large population of buyers currently frozen in their decision could become unblocked and move forward again.

Since the Fed announced the switch from accommodating to cooling, mortgage rate volatility has dramatically increased – the line is far more jagged than we’ve seen in decades. The prime mortgage rate fell as low as 4.99% in early August yet by mid-September rose as high as 6.02% (the most recent PMMS release at this writing). Weekly swings of more than 20 basis points seem commonplace.

Even buyers able to afford a house at current rates could feel frozen, waiting for mortgage rates to fall dramatically again like they did from the end of June to mid-July, when rates dropped 50 basis points in just two weeks.

Combine recent volatility on top of the original 4+ month transition out of the pandemic-era low rate environment from January to April earlier this year, and the picture is even more challenging. In an affordability-strained environment, substantial day-to-day, week-to-week rate movements mean that more buyers are able to qualify for a loan one week, but not the next, or vice versa, making it far more difficult for many borrowers to plan their next step.

In less than five months, the average rate for prime 30-year fixed rate mortgage borrowers (as tracked by Freddie Mac) jumped more than two percentage points – a substantial increase that translates to an extra $360 on a monthly payment for a 30 year fixed mortgage on the typical U.S. home (using raw ZHVI in August).

And that’s a problem. When housing payments – for many households the biggest monthly fixed expense – take up a significant share of your monthly income, that can leave little for variable spending like groceries, transportation or savings so to ensure financial resiliency, it’s often suggested to keep the housing payment below a third of income.

Despite faster than normal income growth too, the mortgage rate increase piled on top of pandemic-era home price appreciation to decidedly pushed national homeowner affordability – the median household income’s share of the mortgage payment, property taxes, and insurance on the typical home – from the mid-20s earlier this year into the mid-30s by May. That’s a strain on national affordability not experienced since the mid-2000s.

Hitting the rule at the national level is significant. For one, it means half of households would be pushing beyond it. On an individual or household level, that can be totally reasonable if you expect a higher income soon or you get more of your satisfaction from free amenities nearby (like public parks and nice weather), but for most households evidence suggests it comes with hardship and tradeoffs.

On a market level, without a healthy spending buffer, a small change in mortgage rate could be fairly impactful on household decisions. That means rate sensitivity is heightened even while mortgage rate volatility has been extreme. By mid-June, mortgage rates had pushed homeowner affordability beyond the threshold to 34%. Yet just six weeks later it was back down below 32. Today, rapidly changing market expectations since pushed homeowner affordability to a record national high of almost 35%.

Under such conditions, made even more extreme when you factor in pandemic-era inflation, many households are uncertain whether to dig deep and put up more to buy down points, postponing their search to save more and lower their debt load, or keep looking and wait for the rates to drop the basis points they need. And it shows. National new listings and sales continue to soften.

If you’re active in the for-sale market but stretching to achieve the next stage of your life, form a good relationship with a trusted lender (or a few – volatility shows up in a lot of ways) who can alert you when it’s a good time.

Aside from ensuring you can afford the next step on a monthly basis, the most financially successful buyers will be those able to find the right home to put down roots, stay past the softer price growth over the coming year into a (hopefully) more stable housing market in the not too distant future.

How far distant? That’s hard to say. For more detailed insight on the Fed’s progress on their mandate, check out Fed Watch: Where is all the volatility coming from?