How to Address Concerns About Foreign Home Buyers

- Federal and local policymakers could do more to address Americans’ concerns about the role of foreign home buyers in the housing market.

- Though transaction taxes are most often discussed, a more productive policy approach could include making information more transparent, expanding financing options for foreign home buyers, and channeling foreign demand to incentivize new supply.

As cities around the world struggle with high housing costs, taxing foreign home buyers has emerged as a popular policy response in a handful of prominent global cities. The ultimate effects of these policies are still to be fully understood, but to date, they do not seem to have fundamentally shifted local market dynamics – especially considering that many such policies were implemented amidst broader initiatives to slow local housing markets.

But while the evidence is mixed, there are a handful of legitimate concerns about some foreign home buyers that likely contributed in some part to such policies being considered in the first place:

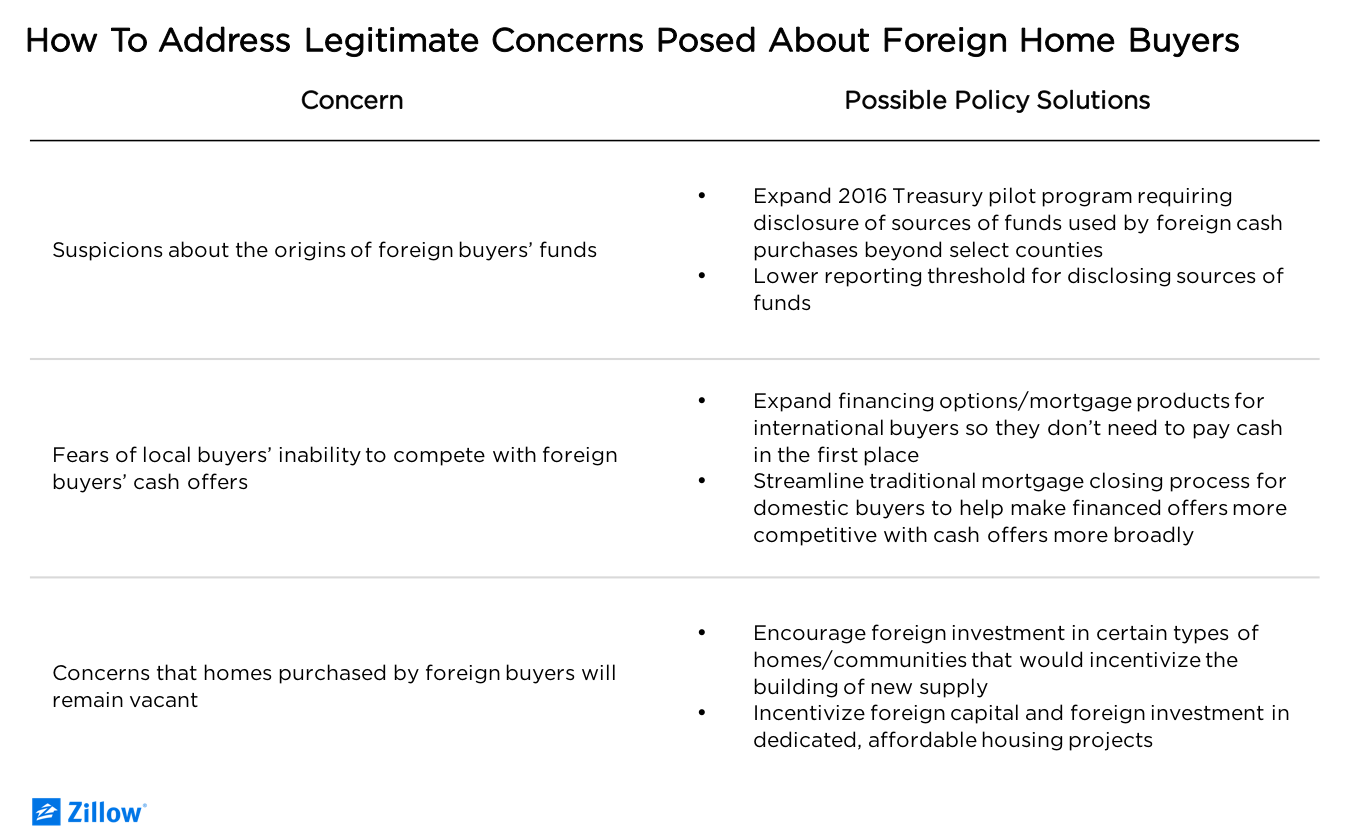

- Suspicions about the origins of the funds sometimes used to buy U.S. homes;

- Fears that sellers will always prefer foreign buyers’ cash offers to locals buying with a mortgage; and

- Concerns that homes purchased by non-resident foreign buyers that would otherwise find a full-time, local occupant are instead left temporarily or permanently vacant.

At both the federal and local levels, there is more that policymakers could and should do to address these specific concerns, regardless of buyers’ nationalities. And there are already some promising efforts.

Room for Improvement

In 2016, the United States Treasury Department began requiring foreigners who pay cash for luxury real estate in a handful of counties to report the sources of the funds used for the purchase. The initiative was launched as a pilot, but disclosure thresholds could be lowered and the program could be expanded, giving Americans more confidence their housing market is not being used as a safe haven for illicitly obtained wealth.

Still, these initiatives have their limits. The pilot program’s purpose is to strictly prevent illicit funds – for instance, from the sale of drugs, bribery, or illegal weapons – from finding their way into the U.S. housing market. This narrow focus would not include proceeds from legal enterprises that may still feel suspect to many Americans, even if they are not strictly illegal – for instance, using proceeds from monopolistic or environmentally harmful businesses.

On the second set of concerns, policymakers are admittedly limited in their ability to address fears about sellers preferring foreign buyers’ cash offers to locals seeking to buy with a mortgage. Holding all else equal, sellers will almost always prefer a cash offer to an offer with financial contingencies, regardless of the buyers’ nationality, since it implies a faster closing and lower risk of the sale falling through. The decision about which offer to accept (if there is more than one) and under what terms is ultimately the seller’s. But there are a handful of common strategies that improve a buyer’s ability to compete with cash offers.

And it must be acknowledged that cash purchases are and will continue to be an important part of the market, and are by no means exclusive to foreign buyers: Investors, downsizing (typically older) homeowners and those relocating to cheaper markets also often pay in cash. It is also important to recognize that foreign home buyers often pay in cash only because it is extremely complicated – often impossible – for them to obtain a mortgage. Streamlining mortgage closings to make buyers with traditional financing more competitive with cash offers, and expanding financing options for international home shoppers, could help mitigate some of these concerns.

Finally, there is no doubt that in densely populated cities, vacant units might be viewed as an inefficient use of space. But determining when exactly a unit is vacant raises complicated questions with only partial, and sometimes arbitrary, answers. Policies discouraging vacancy – taxing owners of multiple properties, or through supplemental taxes on properties that are not a primary residence – are difficult to implement and prone to loopholes. Proposals must be designed to avoid ensnaring seasonal residents, including retirees, and must plan for periodic downturns in the housing market when vacancies may rise because of weak demand.

More Data, More Answers

It is easy to overstate the number of foreign buyers looking for homes in the United States, even in the handful of markets where they tend to focus, and to overgeneralize their motives. But where it is a concern, a more productive regulatory approach might include channeling foreign demand to incentivize new supply and promote transparency.

For those foreign buyers motivated exclusively by a relatively safe investment opportunity in the American housing market, and not by the prospect of moving to the United States, there are ways to more effectively direct this demand and capital to the benefit of the overall American housing market. In Australia, foreign home buyers are limited to buying new construction. This approach has the benefit of encouraging new supply, but it also risks skewing new construction toward a (typically high-end) market segment and price point of more interest to foreign buyers than locals. And the extent of the spillover of this new construction into affordable housing supply is debatable. An alternative approach might be to incentivize foreign capital and foreign investment in dedicated, affordable housing projects. Portugal, for instance, has encouraged foreign investment in its housing market to revitalize struggling communities.

If there is one extremely important area of consensus, it is on the need for more information. Data on foreign home buyers are sparse, and more information could go a long way in demystifying what has long been a murky phenomenon. Zillow has always believed in the mission of bringing data to shed light on the American housing market. Transparency makes markets work better for all participants involved. And while it is true that data can sometimes be used to mislead, it is much easier to mislead or misunderstand where there are no data at all.