Why Getting a Mortgage Is Getting Harder for Borderline Borrowers (And Why It May Get Worse)

- The Zillow Mortgage Access Index stood at 62.7 at the end of Q2, down from 67.8 a year ago.

- Lenders appear to be raising the bar on minimally acceptable credit scores. And the number of mortgage quotes received by borrowers with less than ideal credit scores has not kept pace with the growth in quotes received by more ideal borrowers.

- Looking forward, debt-to-income ratios may become a problem for borrowers as mortgage rates rise over the next year.

For the first time since 2012, getting a mortgage today is harder than it was a year ago, largely because lenders are raising the bar on what they think is a minimally acceptable credit score.

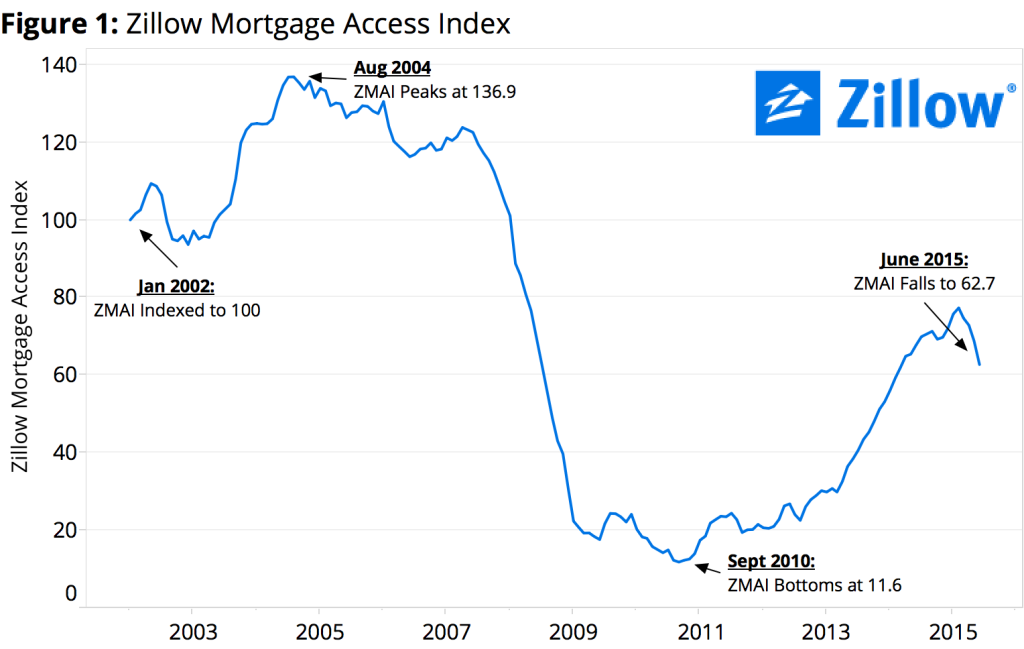

The Zillow Mortgage Access Index (ZMAI) – a measure of how easy or difficult it is to get a mortgage relative to pre-bubble norms – stood at 62.7 at the end of Q2 2015, down from 67.8 in Q2 2014 and the first annual decline in three years (figure 1). A reading of 100 indicates the ease in obtaining a mortgage is equivalent to conditions in January 2002. Readings below 100 signal it is more difficult for borrowers to obtain a mortgage than in 2002, while readings above 100 indicate it is easier to obtain a mortgage than in 2002.

Despite the rare dip in Q2, it’s worth noting that even though it has gotten modestly more difficult to get a mortgage compared to a year ago, it remains far easier than during the depths of the recession in 2011, when the index bottomed at 11.9.

There are a few key factors driving the recent tightening in access to mortgage credit, most notably a shift upward in the minimally acceptable credit scores of successful mortgage applicants. Among the seven key metrics tracked within ZMAI is the 10th percentile of conventional credit scores – the credit score of the lowest 10 percent of borrowers (those at the bottom of the approved credit score spectrum). Potential homebuyers with a credit score below the minimally acceptable 10 percent are going to have difficulty acquiring a conventional mortgage.

Prior to the housing collapse, the minimally acceptable credit score among the bottom 10 percent of successful applicants was 635. In the years following the collapse, as lenders drastically tightened standards, the minimally acceptable credit score consistently topped 700. In December 2012 the 10th percentile conventional credit score finished the year at 712, before consistently falling for the next two years.

Other indicators tracked by ZMAI tell a similar story. Data from Zillow is used to track how many mortgage quotes potential borrowers receive, based on several variables submitted with their request for a quote, including their credit score. ZMAI tracks the number quotes a typical user with a credit score between 600 and 640 (the lower end of the credit spectrum) receives compared to the number of quotes received by a borrower with a credit score of 760 or above (the higher end of the credit spectrum). As of the end of Q2, quotes to users in the higher credit score bucket were generally up, while quotes received by those in the 600-640 bucket stayed flat. This indicates that lenders are showing a higher preference for safer borrowers with higher credit scores than they have in the recent past.

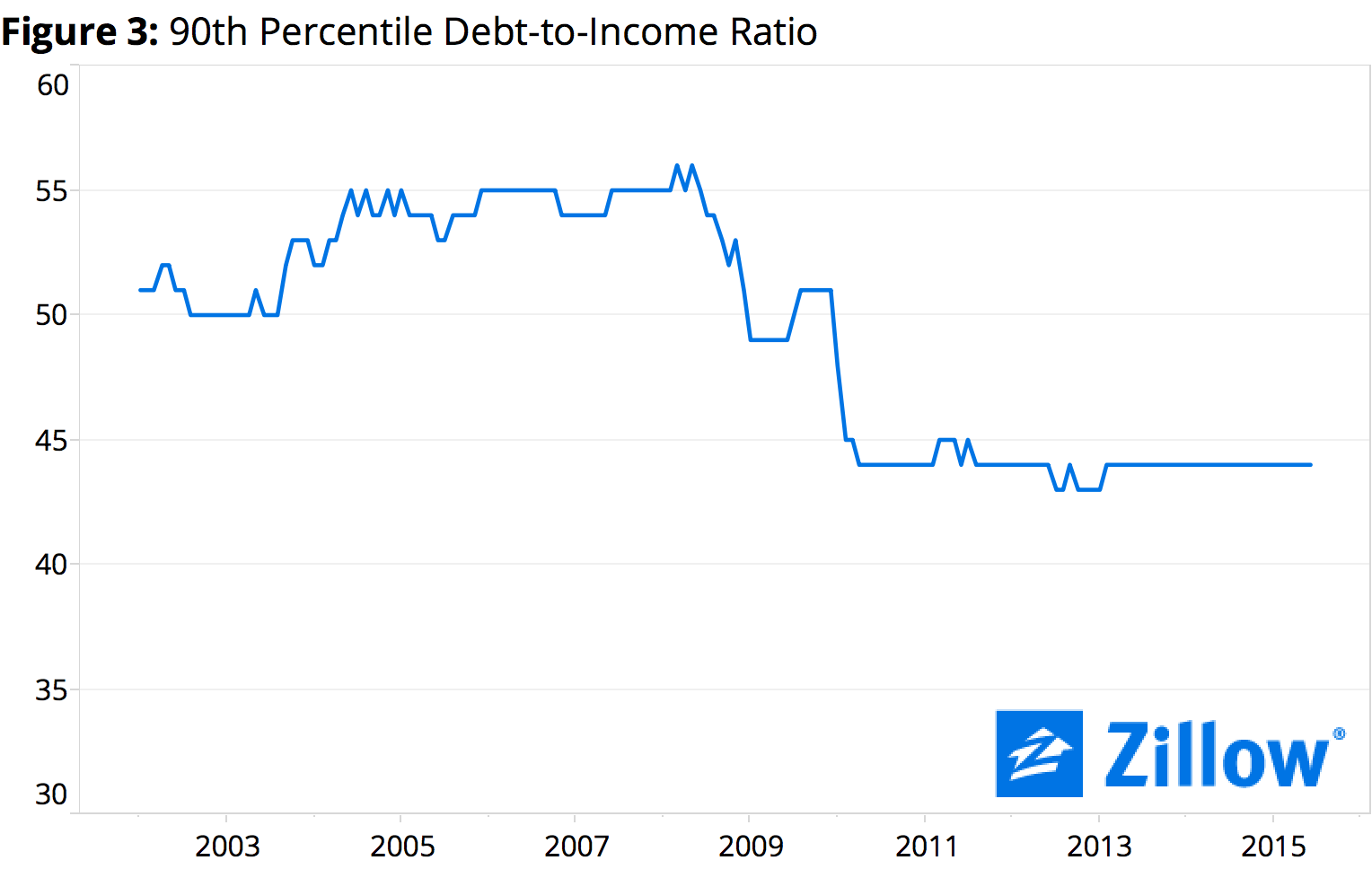

Except in very rare circumstances, a borrower’s DTI typically cannot exceed 45 percent (their debt payments cannot consume more than 45 percent of their income) in order to be eligible for a conventional loan backed by Fannie Mae or Freddie Mac. As such, acceptable DTI ratios haven’t moved much (figure 3).

Getting a Mortgage: Here Today, Gone Tomorrow?

But looking ahead, as mortgage interest rates rise, more income will be needed to cover even marginally more expensive mortgage payments. Those potential borrowers currently bumping up against the 45 percent DTI ceiling may be pushed across the threshold when considering these higher payments.

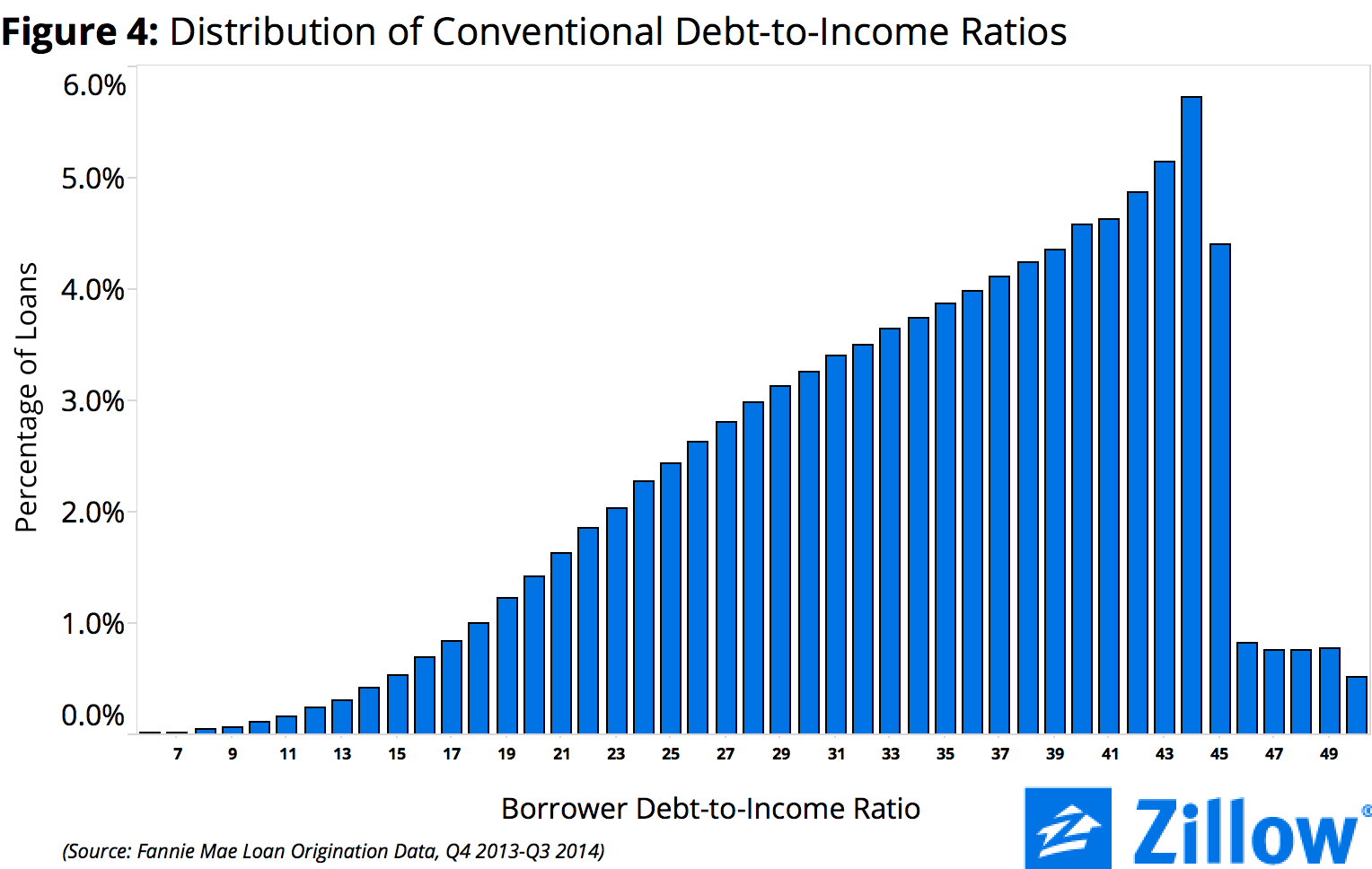

Between Q4 2013 and Q3 2014 (the most recent four quarters for which Fannie Mae loan data is available)[1], the median interest rate on a conventional, 30-year, fixed-rate mortgage quoted on Zillow was 4.2 percent. If rates were to rise to 5 percent by the end of 2016 (holding all else equal) the typical monthly mortgage payment would likely rise by $101 after factoring in the 80 basis point interest rate hike.

In the end, while higher mortgage interest rates may not translate into big changes in monthly payments, they may help tighten the screws on those potential buyers looking to spend as much as possible on a home while still qualifying for a conventional loan.

[1] Includes data on 611,757 conventional borrowers who took out 30 year fixed-rate mortgages.

[2] Median household income among homeowners with a mortgage who moved into their home within the past year. U.S. Census Bureau, American Community Survey 2014, made available by the University of Minnesota, IPUMS-USA.