Experts: Changes to GSE Affordable Housing Goals Likely to Reduce Lending to Underserved Groups

- Experts predict replacing Fannie and Freddie’s Affordable Housing Goals will result in decreased lending to underserved borrowers.

- Experts are split on whether potential changes will improve taxpayer protection or provide better targeting for borrowers in need.

A potential reduction in federal backing for home loans issued to underserved borrowers as a result of ongoing GSE reform efforts is likely to decrease lending in these communities, according to an expert panel. The possible impacts on taxpayer protections and appropriate borrower access are less clear.

The FHFA Duty to Serve Program and single-family/multifamily affordable housing goals instruct government-sponsored entities (GSEs) Fannie Mae and Freddie Mac to purchase a set amount of mortgages held by lower-income families and/or originated in minority, low-income or underserved communities. These mandates are now a key focus of the re-emerging GSE reform debate.

A draft Senate bill includes a framework to eliminate these well-established GSE affordable housing goals in favor of a new fee-based incentive system. Supporters say this will encourage lending to underserved borrowers, will be better targeted and could provide a larger subsidy for affordable housing than the current system. Detractors are concerned that a new approach would create too much uncertainty about the level of resources dedicated to affordable housing and meeting the needs of underserved borrowers.

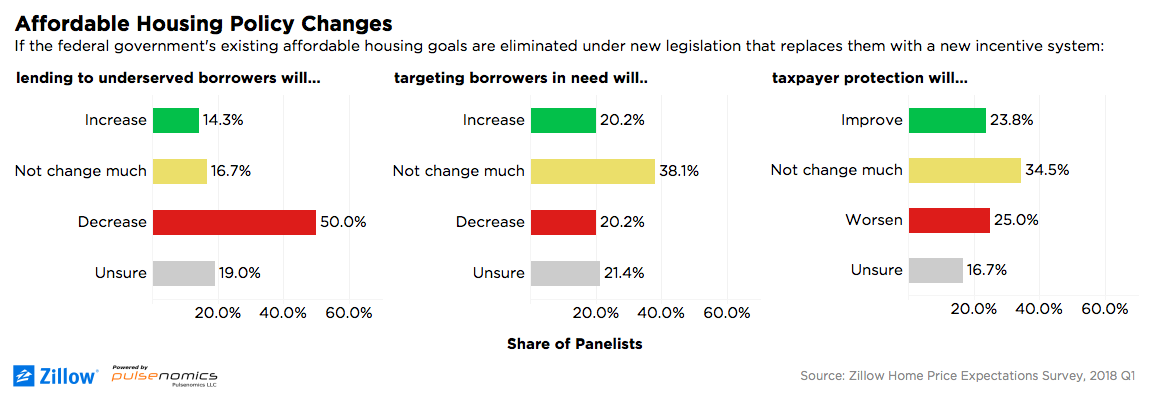

As part of the most recent Zillow Home Price Expectations Survey,[1] more than 100 economists and real estate experts nationwide were asked to determine how lending to underserved borrowers, targeting borrowers in need and taxpayer protection might change under the proposed modifications. Half of respondents said they expected lending to underserved borrowers would decrease if the affordability goals were eliminated; about a third thought lending would increase or remain unchanged, and the rest were unsure. In contrast, respondents were almost perfectly split on the questions how targeting of borrowers or taxpayer protections would change following a legislative overhaul.

Do Current Affordable Housing Goals Work?

Fannie and Freddie’s large footprint in buying mortgages, bundling them and guaranteeing the resulting mortgage-backed securities has kept lawmakers wary about taxpayer risk should the market experience leaner times. Taxpayers are currently on the hook for losses because Fannie and Freddie have been under conservatorship of the U.S. Government since the last recession. As such, lawmakers on both sides of the aisle have advocated for shaking up the current arrangement. However, major sticking points in reform negotiations – including the potential switch to a fee-based system – threaten to torpedo the deal.

Fannie and Freddie’s current affordable housing goals mandate a share of the loans they purchase come from low-income households, very low-income households, or households in low-income areas. There are similar goals for refinancing and multifamily mortgages. Fannie and Freddie meet these goals if they either exceed an assigned threshold, or purchase a higher share of low-income mortgages than the share represented in the overall market.

Because Fannie and Freddie don’t issue mortgages themselves, the intent of the goals is to encourage lending to low-income borrowers and communities that otherwise might have more limited access to home financing on favorable terms. Prior Zillow research found that the GSEs tend to meet their affordable housing goals, although the degree to which these goals affect the market and spur new low-income lending is up for debate.

[1] The Zillow Home Price Expectations Survey is a quarterly survey of more than 100 economists and real estate experts nationwide, sponsored by Zillow and conducted by Pulsenomics. The survey asks experts to offer their expectations for growth in the U.S. Zillow Home Value Index over the next five years, as well as offer their opinion on a series of supplemental questions determined by the survey authors. The most recent survey edition collected responses from 105 panelists and was fielded between Jan. 29 and Feb. 12, 2018.