Experts Explain Why Rent Control Doesn’t Work, and Homeownership Won’t Keep Falling

- Panelists surveyed by Zillow expect home values to end 2015 up 4.1 percent year-over-year, on average.

- On average, panelists said they expected the U.S. homeownership rate to rise only slightly, to 63.7 percent, over the next five years.

- Almost two-thirds of panelists said rent control policies are “government intrusions into the marketplace that, however well-intentioned, always create more problems than they solve.”

Home value growth will slow in coming years, eventually paving the way for a smoother transition from renting to homeownership and likely contributing to an uptick in the U.S. homeownership rate by the end of the decade, according to a Zillow-sponsored survey of more than 100 economists. But rental demand will remain high near-term, fueling a growing rental affordability crisis for which rent control is an increasingly visible, but ultimately unviable, solution.

The 2015 Q3 Zillow Home Price Expectations Survey, sponsored by Zillow and administered by Pulsenomics, LLC, asked panelists to predict annual changes in the U.S. Zillow Home Value Index through 2019. Additionally, experts were asked for their opinions on the future path of the U.S. homeownership rate, and on the efficacy and impacts of rent control policies.

Overall, the experts said they expect home values to rise more slowly in coming years and the homeownership rate to stabilize before rising slowly, and overwhelmingly advised against rent control policies they largely view as intrusions and – at best – only stopgap measures.

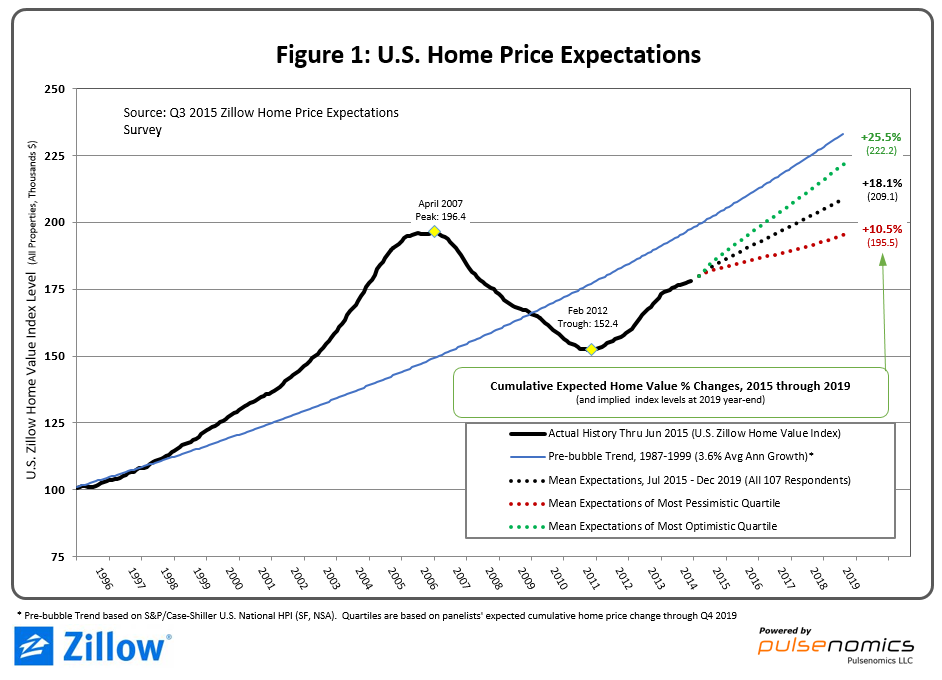

Panelists predicted home values to end 2015 up 4.1 percent year-over-year, on average, down from the 4.3 percent year-end prediction made by the same panel last quarter. Home value appreciation is expected to slowly level off beginning next year (3.4 percent average annual expected appreciation) and through 2019 (3.1 percent average annual expected appreciation).

This trajectory would see the median U.S. home value rise above the April 2007, bubble-era peak of $196,400, on average, by December 2017. The most optimistic panelists predicted home values would surpass bubble-era peaks as soon as February 2017, while the most pessimistic said pre-bubble peaks would not be met or exceeded before the end of the decade (figure 1).

“The panel’s expectation for U.S. home values fell to a 3.4 percent average annual rate for the five-year forecast horizon. This is the first time in 18 months that this proxy for experts’ housing market sentiment has weakened, and it’s the lowest rate recorded in three years,” said Pulsenomics Founder Terry Loebs. “With slow wage growth persisting and monetary policy liftoff looming, home price expectations may continue to drift lower for some time.”

Homeownership On the Rise – Slowly

But there is a silver lining to slower home value growth. A slower-moving market gives renters, particularly younger renters, more breathing room to save for a down payment and prepare for the jump to homeownership. The national homeownership rate is currently 63.4 percent and has been falling steadily over the past several years. But more than two-thirds of panelists (69 percent) said they expect the homeownership rate to rise over the next five years, however modestly, coinciding with a slowdown in home value growth. On average, panelists said they expect the homeownership rate to rise to 63.7 percent by 2020.

In the short-term, however, panelists said they expected the national homeownership rate to remain at 63.4 percent, on average, over the next two years. Fewer homeowners means more renters, and high rental demand coupled with limited rental inventory and stagnant wages is contributing to a growing rental affordability crisis. A rising homeownership rate will help take some of the pressure off of rents, but both this most recent survey and prior surveys indicate the rental affordability problem is likely to loom large for at least the next few years, even as cities struggle to cope today.

Why Rent Control Doesn’t Work

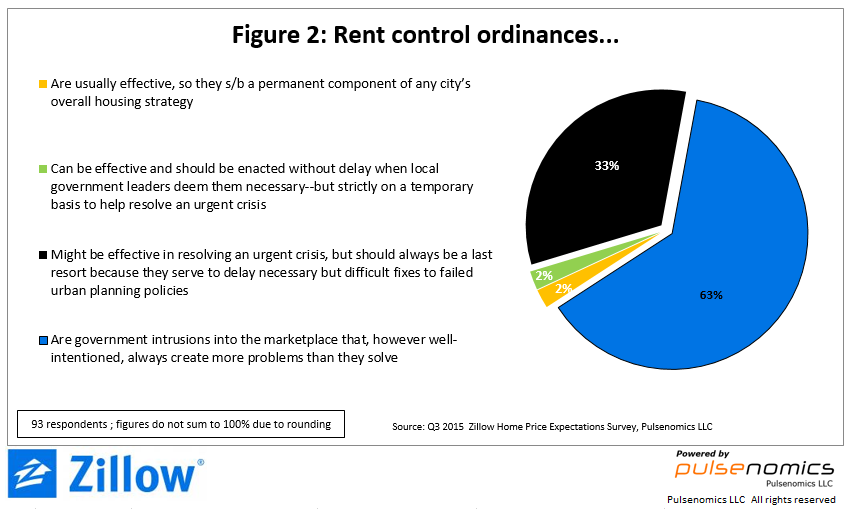

To combat the rental affordability problem, officials and planners in a number of American cities are increasingly considering capping rents through overt rent control policies, or through mandated inclusionary zoning regulations that force developers to cap rents on a certain share of new units. But according to the panelists, this turn toward rent control as a permanent solution is misguided. Almost two-thirds of respondents with an opinion (63 percent) said rent control policies were “government intrusions into the marketplace that, however well-intentioned, always create more problems than they solve.” The next-largest group, 33 percent, said rent control might be effective in a crisis, but should be a last resort. Just 4 percent of respondents said rent control policies are either usually effective or can be at least temporarily effective (figure 2).

Panelists largely cited rising rents on non rent-controlled apartments and less incentive or resources for maintenance and improvements among rent-controlled properties as the main effects of rent control policies. Three-quarters of respondents (75 percent) said they would expect rents for nearby units not subject to rent control to rise somewhat or significantly within areas where rent control policies are in effect. Almost all (92 percent) said building improvements by property owners would fall somewhat or significantly, while 85 percent said they would expect building maintenance would suffer somewhat or significantly.

In other words, while tenants tend to benefit from rent control, there’s little incentive for their landlords to update appliances, install air conditioning or build out a great rooftop deck if they can’t pay for it by hiking rents. It may be OK to defer this kind of maintenance and improvement while the rental market is tight. But if and when homeownership starts to rise and rents begin to come down, landlords subject to strict rent control may be left with outdated units that are more difficult to rent in the face of competition from other landlords who had the means to invest in their properties when times were better.