Home Sales Flat For Now, But Things Could Be Looking Up

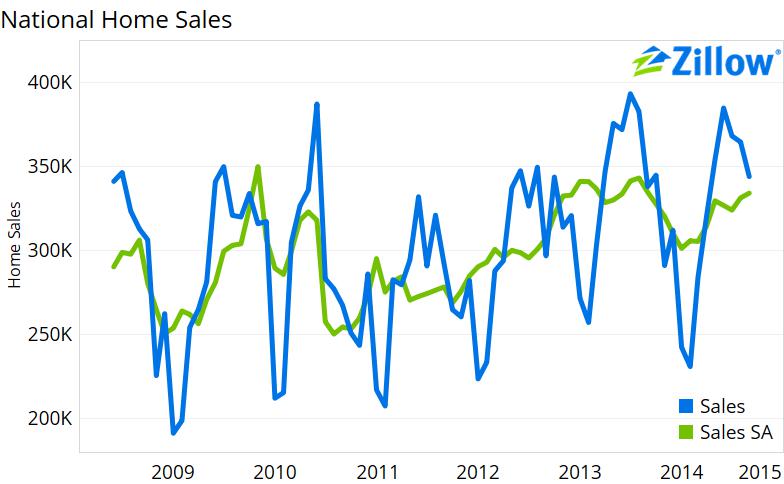

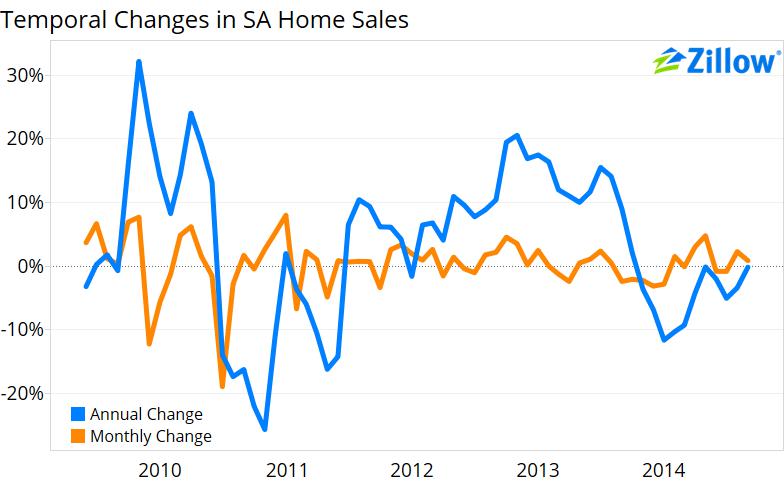

- New and existing home sales in September rose 0.8 percent month-over-month, to a seasonally adjusted value of 334,093. Sales growth was essentially flat year-over-year, falling just 0.2 percent.

- September’s numbers represent a sales level only 2.6 percent off the non-tax-incentive-driven, post-recession peak in August 2013.

- Confidence among millennial renters, strong job growth, an increasingly distant recession and easing fears abroad offer glimmers of hope for sales volumes to rise.

The number of homes trading hands has been falling, a casualty of lackluster demand from younger buyers and an overall lack of affordable homes for sale, even as home affordability in general remains very high. But looking ahead, there’s reason to be optimistic that sales volume will soon pick up.

New and existing home sales in September rose 0.8 percent month-over-month, to a seasonally adjusted value of 334,093. Sales growth was essentially flat year-over-year, falling just 0.2 percent, a significant improvement after three straight months of annual declines of more than 2 percent. After the housing market collapsed in late 2007 and into 2008, home sales briefly peaked at 349,891 in November, 2009, but that number was inflated by the surge of home buying spurred by generous federal tax credits passed as part of the American Recovery and Reinvestment Act (commonly known as the Stimulus Act). Excluding this, sales peaked last August at 343,086, but have not risen annually since then.

But September’s numbers represent a sales level only 2.6 percent off this peak, leading to hopes that as we exit 2014, home sales may again start to show more robust growth and move toward pre-crash levels. And there are a number of factors that could help.

Many have speculated that one of the primary factors holding back home sales is the lack of millennials (young adults aged roughly between ages 23 and 34) entering the market, either by force or by choice. A recent Zillow analysis showed that millennials’ desire to own a home has not dropped, rather the demographics among millennial groups who typically own homes has changed. Millennials who can afford it—i.e., those with a full time job—are still buying homes. Given the recent strong jobs report, this is a positive sign, particularly if wage growth picks up. Moreover, young renters are confident they will be able to buy a home at some point.

Additionally, we are approaching the six year mark since the recession officially ended. That’s an important milestone, because it typically takes about that long for the homeownership rate of young adults who graduated from college during a recession to catch up to the homeownership rate of those who graduated during more normal economic times. Finally, if overseas fears ease and recent volatility in financial markets settles, it is reasonable to expect these factors to lift future sales.