Existing Home Sales to Rise Modestly in August

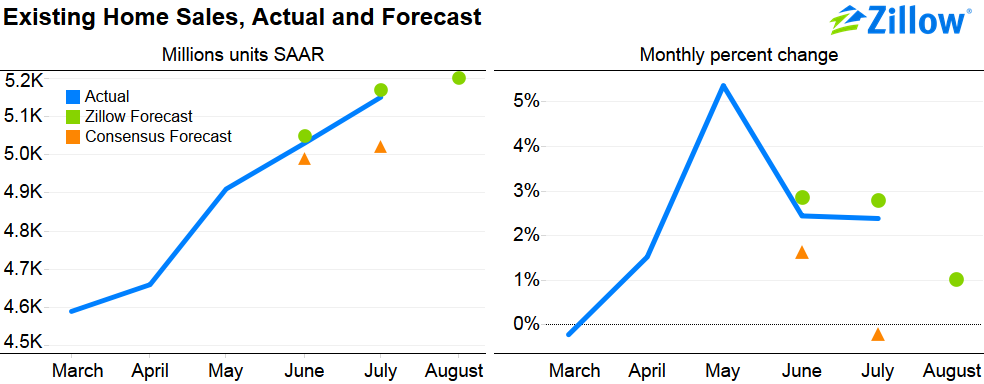

- We expect existing home sales to increase to between 5.20 million and 5.22 million units (SAAR) in August.

- This would translate into a percent increase between 1.0 percent and 1.3 percent over the month.

- Interest rates were flat in July and provided a modest impetus to sales; slow income growth and a low homeownership rate (relative to historical trends) contributed to lower sales.

On Monday, the National Association of Realtors (NAR) will release data on August 2014 existing home sales. We expect sales of single family residences, condos and co-ops to increase 1.0 percent to 5.20 million units (SAAR) from 5.15 million units in July.

Background

Existing home sales totaled 5.15 million (SAAR) in July, up 2.4 percent from June, but 4.3 percent lower than a year earlier. Sales had been slowly but steadily increasing since late 2010 before dropping sharply during summer 2013 after interest rates rose. They began to recover in spring 2014, regaining about half of the decline recorded between July 2013 and March 2014.

Despite recent gains, there remain considerable doubts about the strength and durability of recent gains. Policymakers and market observers continue to point to sluggish home sales as one of the key restraints holding back a broader economic recovery.

Forecast

We use two models to develop our expectation for incoming existing home sales data.

- A “fundamentals” model that estimates home sales as a function of macroeconomic fundamentals. (More information about this model can be found in our earlier brief.)

- A “historical” model that estimates home sales as a function of past movements in existing home sales as well as recent pending home sales data. (More information about this model can be found in our earlier brief.)

Several additional assumptions are necessary for the “fundamentals” model, which are described in greater detail below.

Overall, we estimate that August 2014 existing home sales should total between 5.20 million (according to the “fundamentals” model) and 5.22 million units (SAAR) (according to the “historical” model)—an increase of between 1.0 percent and 1.3 percent respectively from July.

Explanation

Interest rates were essentially flat in August, providing a continued (if modest) boost to home sales. Similarly, the gap relative to historical rates was virtually unchanged.

However, slower median family income growth and a low homeownership rate (relative to historical trends) played a more important role in restraining existing home sales in August.

Forecast Risks

Median Family Income

The first, and most prominent in our view, risk to our estimate of existing home sales concerns the rate of change of median family income in recent months—a key input in our “fundamentals” model. Since data on median family income are currently only available through March 2014, we must extrapolate forward.

In our baseline forecast described above, we assume that median family incomes grew in line with the Consumer Price Index (CPI) between March and August 2014. (The CPI and median family income level series have a correlation of 0.99 between April 1976 and March 2014; the annual change series have a correlation of 0.72.) Under this assumption, median family incomes would have grown by 3.0 percent for the year ending in August 2014.

While the CPI is strongly correlated with median family income over a long history and has the advantage of being available through August 2014, in more recent years, Personal Consumption Expenditures (PCE) have demonstrated a stronger correlation with median family income. One limitation is that PCE data are currently only available through June 2014. If we index median family income forward from March 2014 through June 2014 using PCE data, and then index the series forward through August 2014 using CPI data, we get slightly higher annual median family income growth of 3.2 percent. Under this assumption, existing home sales in August 2014 would total 5.22 million units (SAAR), up 1.3 percent from July.

Homeownership Rate

A second risk concerns the homeownership rate. Our model assumes that the homeownership rate increased 0.2 percentage point to 65.0 percent between June 2014 (latest data available) and August 2014—in line with the percentage point increase in the homeownership rate between June and August 2013.

If we hold the homeownership rate constant at its June 2014 level of 64.8 percent in our baseline model, then existing home sales would fall 1.1 percent to 5.09 million units (SAAR); if we assume median family incomes also grow in line with PCE growth, then existing home sales would fall 0.1 percent to 5.11 million units (SAAR).

However, the homeownership rate has trended downward in recent years: Over the past two years, it has declined by an average of 0.03 percentage point each month. If this trend continues and the homeownership rate falls to 64.7 percent, then our baseline model suggests existing home sales would fall 1.7 percent to 5.06 million units (SAAR); if we assume median family incomes also grow in line with PCE growth, then existing home sales would fall only slightly more modestly, down 1.3 percent to 5.08 million units (SAAR).

Other assumptions

Other assumptions have more modest effects on the estimates produced by our “fundamentals” model.

We assume that the homeowner vacancy rate remains constant at its June 2014 level. The homeowner vacancy rate tends to move broadly with the business cycle but over the past two years, it has fluctuated between 1.95 and 1.55.

For the median sales price of existing homes, we forecast the series one-month ahead using a best-fit ARIMA model estimated over the period April 1976 through July 2014—an ARIMA(2,1,3) process in this instance. This produces an estimated median sales price for existing homes in August 2014 of $211,599—up 0.6 percent from $210,233 in July.

Finally, we forecast the number of households two months ahead using a best-fit ARIMA model, estimated over the period April 1976 through June 2014—an ARIMA(0,2,1) process in this case. This produces an estimate of 115.227 million households in August 2014, up 0.1 percent from 115.097 million in June.

Given the relatively small coefficients associated with these variable in our model, we believe that these assumptions are reasonable and conservative.