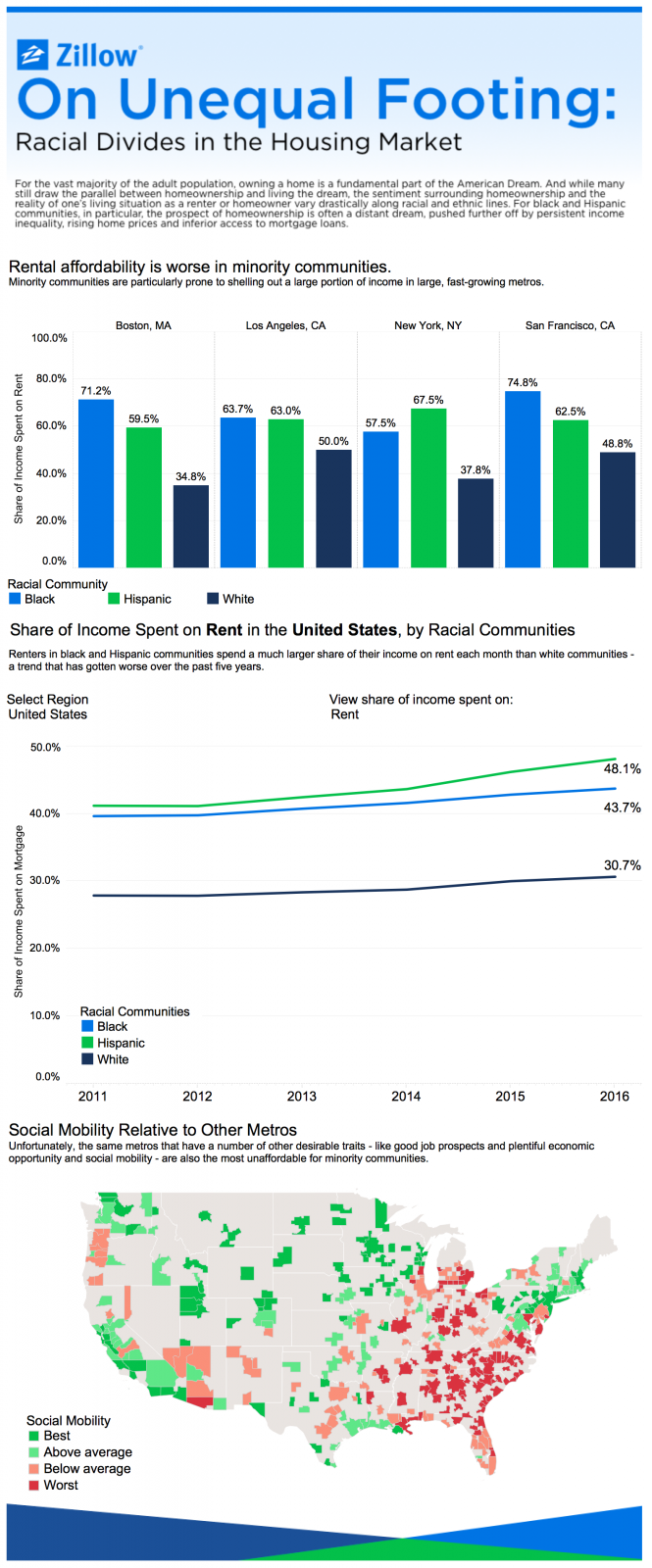

On Unequal Footing: How Housing Affordability Changes Across Racial Communities

- Nationwide, renters in minority communities spend a much larger share of their income on rent each month relative to those in white communities – a trend that has persisted over the past five years.

- Nationally, monthly mortgage payments consume less than 30 percent of income for most racial and ethnic groups. But saving for a down payment, particularly in minority communities, can be difficult when rents consume upwards of 40 percent of household income.

Nationwide and in many metro markets, rent in black and Hispanic communities consumes a much larger share of household income than in white communities, widening the great divide that already exists between white America and communities of color. This inequality in housing affordability also makes it difficult for blacks and Hispanics to afford living in those areas offering the best opportunities for social mobility, and almost impossible to save for a down payment and gain a foothold in the housing market that might set up future generations for success.

Rent Affordability

Over the past five years, as rents rose and income growth was weak at best, renters nationwide – regardless of racial or ethnic group – have been forced to dig deeper into their pockets to cover rent. But minority communities have taken the largest hit. In 2011, when the United States was still deeply mired in the housing bust, the typical renter in a black community could expect to spend 39.6 percent of his household’s income on rent. Today, that number has grown to 43.7 percent. Similarly, the typical renter in Hispanic communities could expect to spend 41.2 percent of their household’s income on rent in 2011, a figure that now stands at 48.1 percent. Rent affordability also suffered in white communities over the same time, but to a much smaller degree: Renters in these areas have typically spent somewhere between 27.9 and 30.7 percent of their income, within the old rule of thumb that says rent should not exceed 30 percent of income.

Renters in minority communities are particularly prone to shelling out a large portion of their income in large, fast-growing metro markets – unfortunately, the exact same markets that tend to offer many other desirable amenities including more plentiful economic opportunities and better social mobility. For example, in the notoriously unaffordable San Francisco metropolitan area, renters in white communities can expect to spend 48.8 percent of their income on rent each month – certainly a very large share of their income, but nevertheless small in comparison to minority neighborhoods. In these black and Hispanic enclaves of San Francisco, renters should expect to spend a whopping 62.5 percent and 74.8 percent of income on rent, respectively. Similar stories emerge in many other large metropolitan areas where incomes are generally much lower in largely black and Hispanic communities.

Mortgage Affordability and Homeownership

Across many large, thriving markets, home values have rebounded so quickly that even though monthly mortgage payments are relatively affordable, saving for a 20 percent down payment that often reaches into the tens of thousands of dollars even for a modest home is out of reach for many. And when rent consumes upwards of 40 percent of a household’s income, it leaves little room for saving at all.

But for those able to overcome the hurdle of saving for a down payment, mortgage payments are generally affordable, even across racial communities – thanks in large part to slowly rising, but still-low mortgage interest rates associated with a conventional 30-year mortgage today. In a typical white neighborhood, home buyers can expect to spend 15.2 percent of income on mortgage payments each month, solidly below the pre-housing boom average of 18.9 percent. Similarly, home buyers in predominantly black and Hispanic neighborhoods can expect to spend 13.6 percent and 22.8 percent of their income on mortgage payments each month, also among the lowest share in the past 20 years.

But while calculating the share of income spent on a mortgage each month in this manner allows us to compare across racial communities, it likely underestimates the true cost of a mortgage for many residents of minority-dominant communities. First, it is fairly common for potential home buyers in any community to put less than 20 percent down on a home. And inevitably, the less money paid upfront on a home purchase, the higher the monthly mortgage payment.

Additionally, it is well-known that mortgage applications from blacks and Hispanics are denied more frequently than applications from whites. In 2015, Hispanics were denied a conventional mortgage twice as frequently as whites; blacks were denied 2.6 times as often. As a result, minorities are more likely to apply for loans backed by the Federal Housing Administration (FHA), which have similar interest rates to conventional loans. But despite the similar interest rates, FHA loans often end up costing borrowers more in the end because they require a smaller down payment and have high insurance premiums, which borrowers must pay as part of the FHA process to protect the lender from a loss in the event of borrower default. As a result, even though it may appear as though black communities, in particular, can expect to spend less of their monthly income towards mortgage payment than white communities do, the reality may not be quite so bright.[1]

For the vast majority of the adult population, owning a home is a fundamental part of the American Dream. And while many still draw the parallel between homeownership and living the dream, the sentiment surrounding homeownership and the reality of one’s living situation as a renter or homeowner vary drastically along racial and ethnic lines. For black and Hispanic communities, in particular, the prospect of homeownership is often a distant dream, pushed further off by persistent income inequality, rising home prices and inferior access to mortgage loans.

Methodology

To estimate the percent of income spent on monthly rent and mortgage payments by racial communities, we categorized census tracts by their racial pluralities. Once census tracts were categorized as predominantly black, white, or Hispanic, we used census tract-level median household income from the U.S. Census Bureau alongside the Zillow Home Value Index (ZHVI) and Zillow Rent Index (ZRI) to calculate rent and mortgage burdens in census tracts. We then aggregated census tracts up to the metropolitan area and national level, requiring that a given racial community make up at least 1% of the population in the metro.

Related:

- Age and Affordability: Why an Affordable Rental Home is More Often an Older Home, and Why That Matters

- Q4 2016 Housing Affordability: Accelerating Home Values, Rising Rates Cause Rapid Deterioration

- Local Opportunities: Finding Relatively Affordable Housing, Even in Largely Unaffordable Markets

[1] Home values in predominantly black communities also have a tendency to be much lower than home values in predominantly white communities, which means that the typical homebuyer in such a community can expect to spend less on a conventional mortgage payment than the typical homebuyer in a white community.