In the Denver area, multifamily permitting activity is near all-time highs, while single-family permits have struggled to recover from the recession.

Strong population growth and rapidly rising rents in recent years have spurred multifamily developers into action.

But rental growth has cooled off recently, and concessions are on the rise.

In 2010, a majority of Denver households were homeowners. By 2014, a slim majority of Denver households were renters. This shift did not go unnoticed by Denver-area builders, with permits for multifamily properties hitting decade-long highs in recent years even as single-family home permitting activity remained stalled at a fraction of pre-recession levels.

But despite the surge in new renters, is Denver’s relative flood of new multifamily units set to come on line in coming years threatening to drown this new demand?

Multifamily Surge

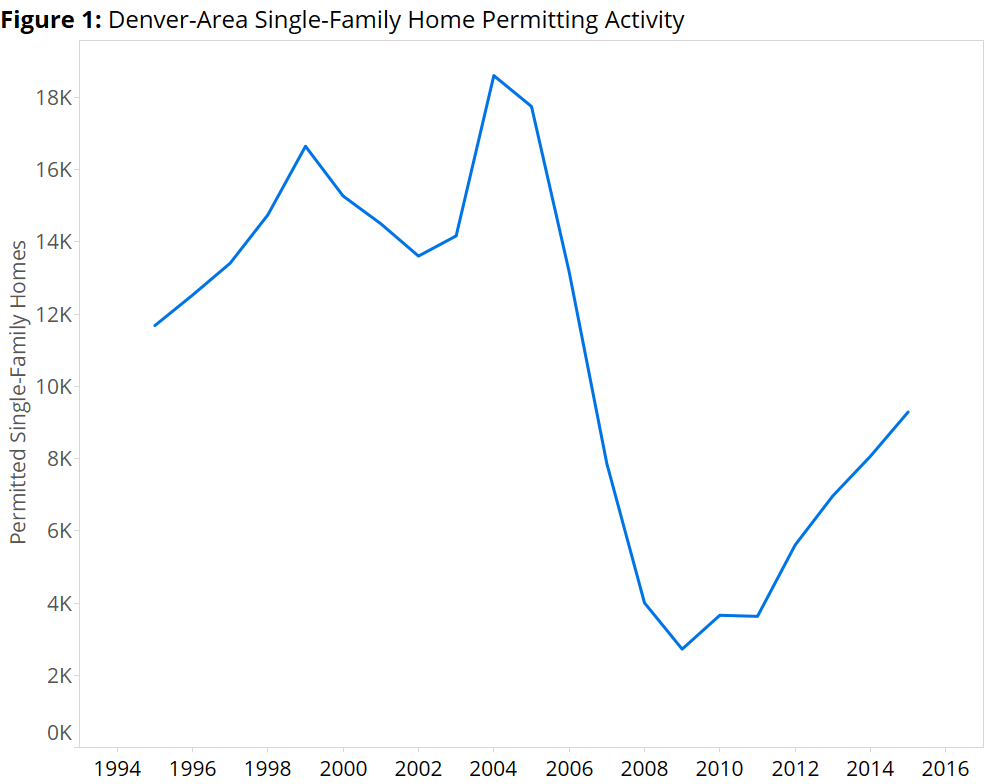

Like many markets nationwide, the new construction market in the Denver metro for single-family homes has been slow to recover from the housing recession. A decade ago, Denver-area builders were pulling permits for almost 15,500 single-family homes per year, on average. But since the housing crisis, less than 6,000 single-family home permits have been issued per year, on average, and activity has only recently shown signs of really taking off (figure 1).

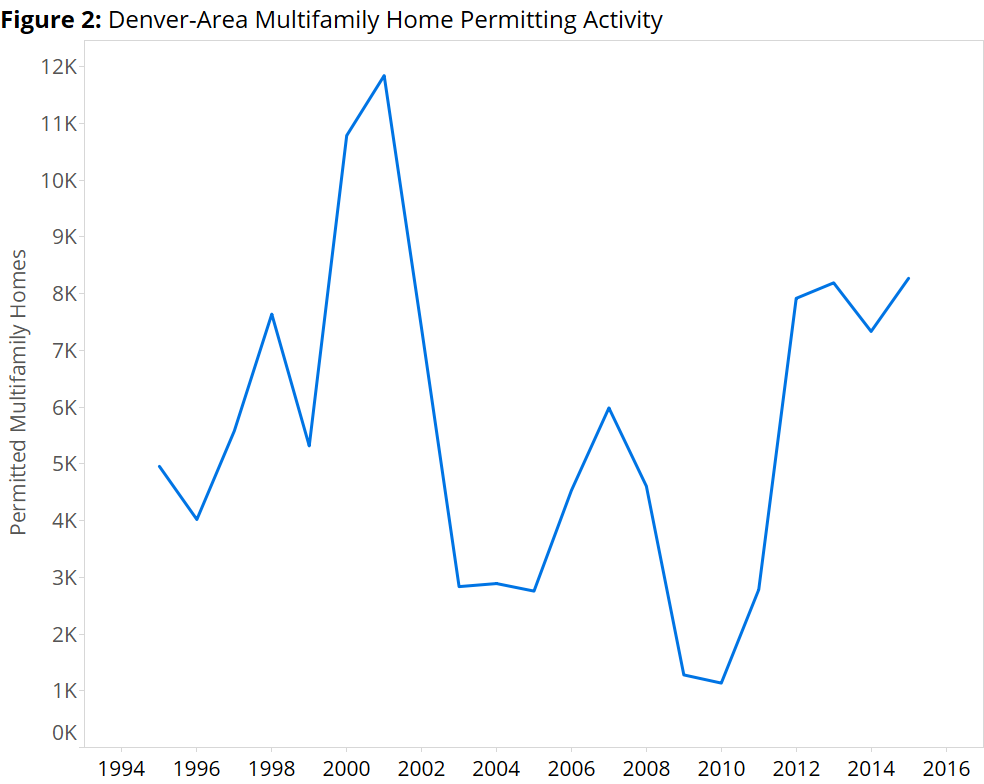

But if single family construction has been slow to recover, multifamily has been anything but. Multifamily permitting activity in each of the past four years exceeds permitting activity in all but two years on record. More than 31,000 new units have been permitted in the past four years combined (figure 2).

Of course, it does take some time to move from the permitting phase all the way to a completed multifamily unit, and many of these new units have yet to hit the market. But when they do begin coming on line, this new supply will represent a substantial increase in the Denver area’s total stock of multifamily units, currently about 350,000 strong.

So, is Greater Denver ready for the coming flood of multifamily units?

A Growth Story

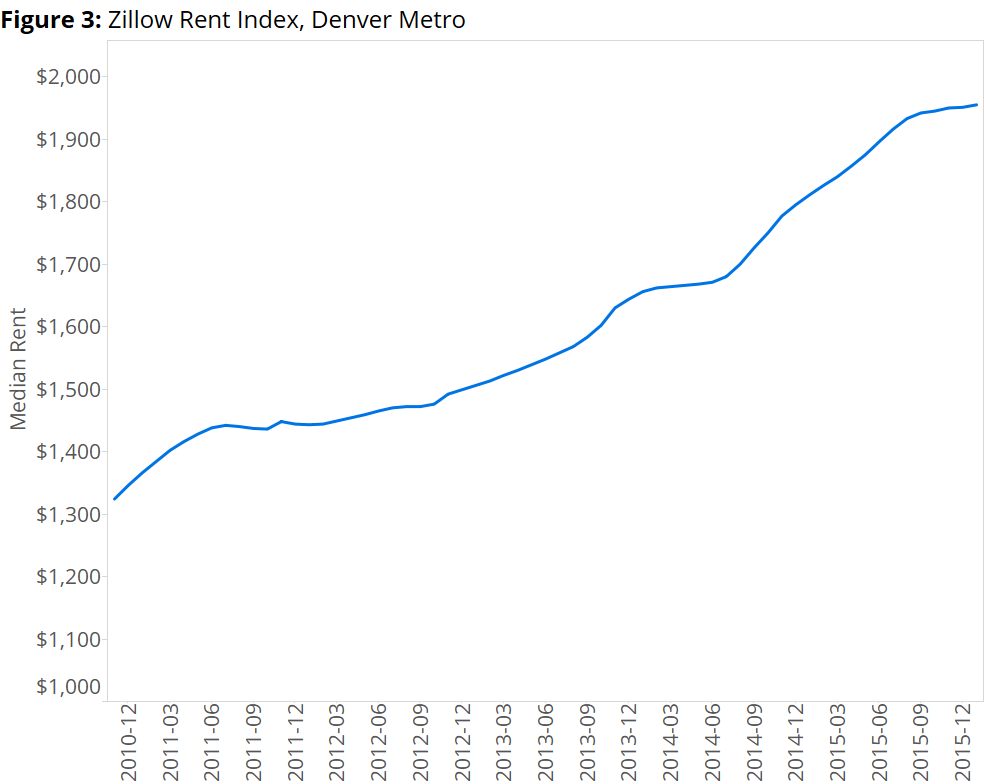

At first blush, the answer might be yes. Builders in Denver have been chasing a rental market, in particular, that is simply on a tear. In 2015, the median rent in the Denver area rose 8.7 percent year-over-year, fourth-fastest among the nation’s 35 largest metro markets and almost triple the national rate of 3.3 percent annual growth last year. Median rent in the Denver area reached $1,959 per month in February (figure 3), in the top tier of most expensive large rental markets nationwide, ahead of other fast-growing markets like Seattle and just behind the notoriously expensive rental markets of Boston and Washington, D.C. This rapid growth in rents suggests healthy demand for new rental units.

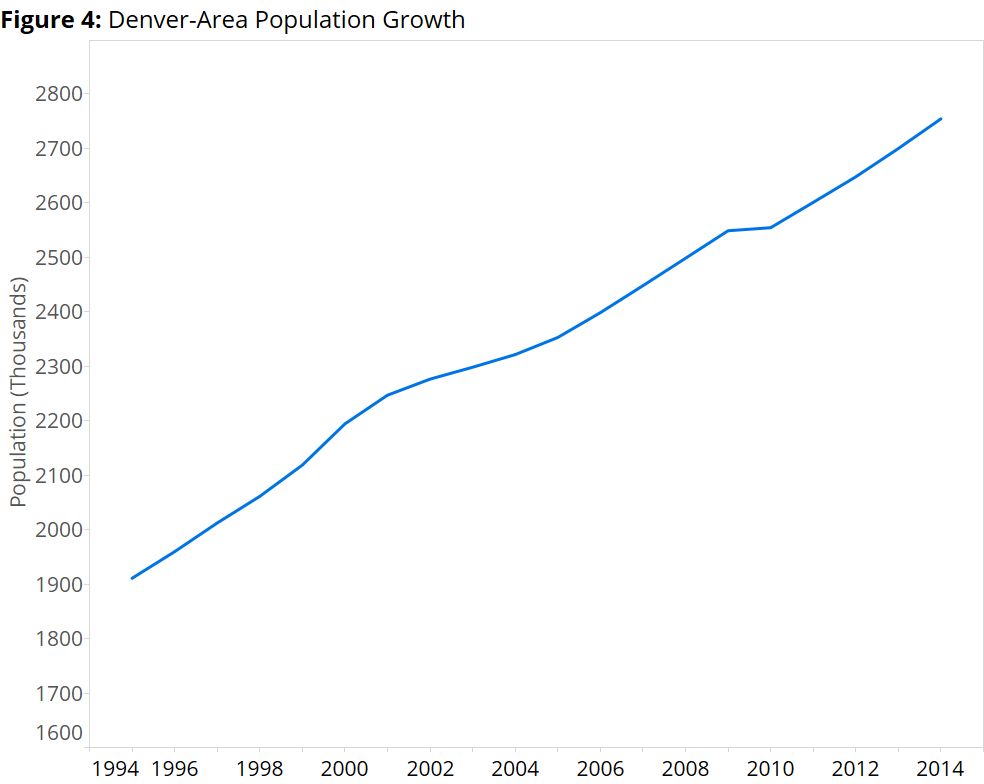

And population growth has also been strong, another indicator of strong demand. In the decade from 2004 through 2014, the overall population of the Denver metro area grew by more than 430,000 residents, or more than 18 percent, according to the Census Bureau (figure 4). This trend shows few signs of fading, buttressing the argument that demand for housing will remain strong – particularly rental housing, which is generally more attractive to new residents of an area looking to get their bearings before buying a home.

Too Much, Too Fast?

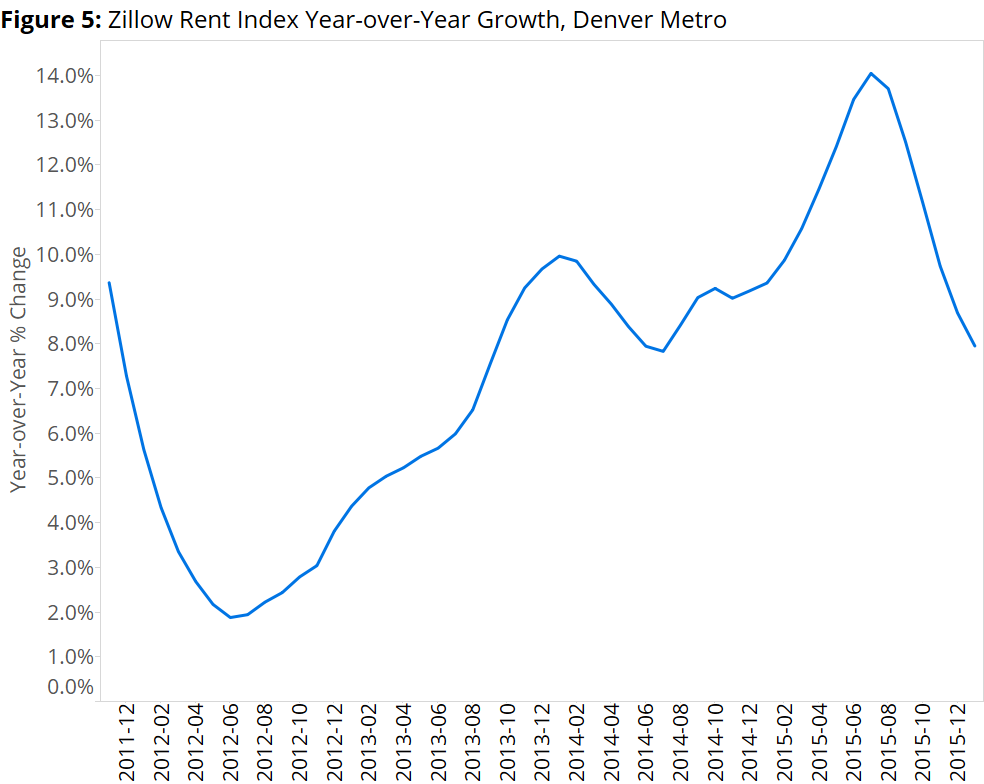

But there are signs that multifamily builders may be getting ahead of themselves. The pace of annual rental growth, while still strong, has been slowing down. Year-over-year growth rates have fallen in half, from a high of 14 percent as recently as July to 7.2 percent in February (figure 5). And after hovering below 5 percent for much of this recent boom, rental vacancy rates jumped to 6.8 percent in the last quarter of 2015, a significant increase, with the vacancy rate in downtown Denver reportedly rising above 11 percent. And to combat this rising vacancy rate, landlords and property managers are offering more concessions to get renters in the door. The average concession or discount granted to tenants totaled roughly 10 percent of monthly rent in the second quarter of 2015, up from less than 9 percent in the fourth quarter of 2014.

Taken together, all of this suggests that while demand so far has been sufficient to absorb those units that have already come online, it may be stretched to accommodate the tens of thousands of units builders are planning to deliver over the coming years. And in those coming years, Denver’s run as one of the hottest rental markets in the country may come to an end as supply finally catches up to (and passes) demand.

On March 30, Zillow will make Denver the seventh stop on its Housing Roadmap to 2016 tour of America, aimed at discussing housing challenges in the cities most impacted by them. Over the past decade, Denver has become one of America’s fastest-growing cities, with droves of new residents attracted by the city’s legendary beauty and quality of life, and its abundant job opportunities.

But growth does not come without growing pains, and Denver is not immune. Prior to our March 30 discussion, Zillow will publish new research detailing the factors driving Denver’s enviable growth, as well as some of the side effects.