As Fed Raises Interest Rates, Homebuyers’ Plans May Bend, But Not Break

- Americans are broadly aware that interest rates are poised to increase, particularly home shoppers currently on the market.

- The prospect of higher mortgage rates is giving some current and prospective home buyers pause – particularly younger adults and Hispanics.

- For most home shoppers, there are other more pressing concerns about the housing market that rank above rising mortgage rates.

It’s all but certain the Federal Reserve Board’s Open Market Committee will vote next week to raise its benchmark interest rate for the first time since 2006, likely marking the end of a six-year period of historically low interest rates – including mortgage interest rates.

Americans are broadly aware of these looming changes, and they are certainly giving some would-be home buyers pause. For a few key demographic groups – including current renters and younger would-be buyers – rising interest rates could lead to changes in their home buying plans. But overall, a modest increase in mortgage interest rates is unlikely to completely de-rail most buyers’ plans, and Americans are more concerned about finding an affordable home and saving for a down payment, according to a recent Zillow survey of likely home buyers.

Most Americans Read the Headlines, But a Few Don’t

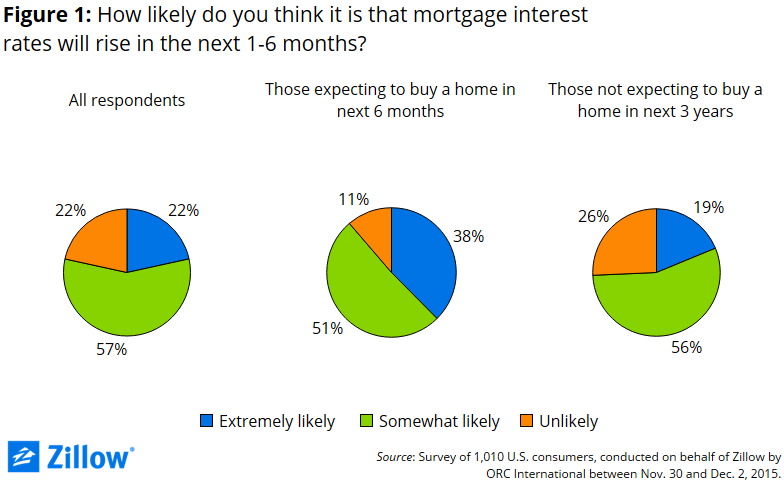

Most Americans surveyed are broadly aware that interest rates are poised to increase, with 78 percent of respondents saying they think it is “extremely likely” or “somewhat likely” that mortgage rates will rise in the next one to six months (figure 1).

Still, more than one in five Americans (22 percent) said they think it is unlikely that mortgage rates will rise in the next six months – the same share who indicated it is “extremely likely” that mortgage rates will rise.

Rising Rates Likely to Bend, Not Break, Home Buying Plans

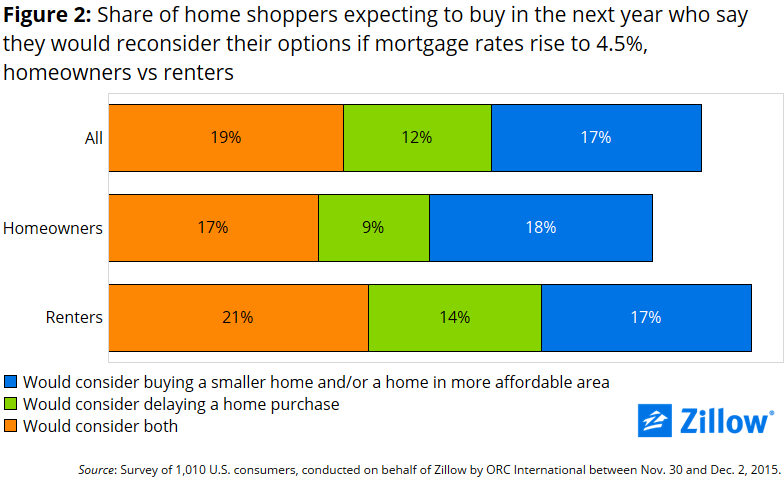

An increase in mortgage rates from around 4 percent currently to 4.5 percent – roughly the level most economists expect by mid-2016 – would certainly give American home shoppers pause.

Almost half (47 percent) of home shoppers who indicated they are currently searching for a home, or expect to search for and buy a home in the next year, said an increase in this range would lead them to reconsider their options (figure 2). Among these home buyers, 17 percent said they would search for a smaller home in a more affordable neighborhood, 12 percent said they would consider delaying their purchase, and 19 percent said they would consider both strategies.

Some Groups Are More Sensitive Than Others

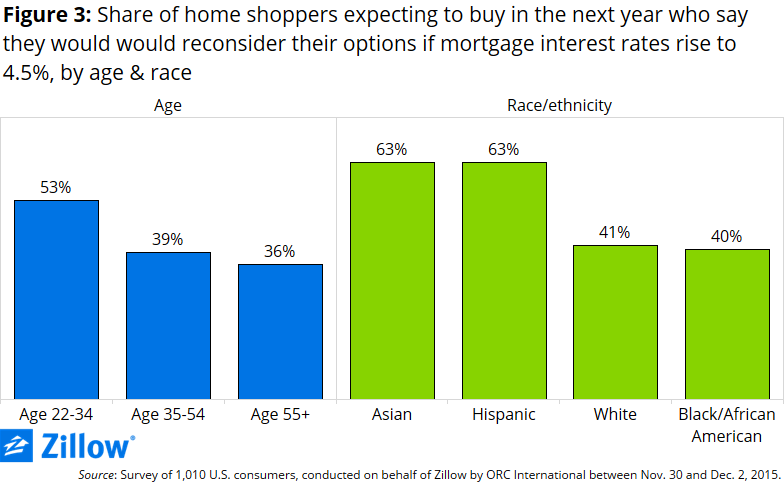

Young adults and Hispanics indicated they are much more likely than other demographic groups to adjust their home buying plans in response to rising interest rates.

Among respondents currently in the market or expecting to buy a home in the next year, almost two thirds of Asians and Hispanics (63 percent in both cases) said they would rethink their buying plans if rates were to rise to 4.5 percent, compared to 40 percent of blacks and 41 percent of whites. Changes to these plans could include delaying a purchase and/or adjusting the type of home they are searching for or the neighborhood where they are searching. Similarly, 53 percent of potential buyers aged 22 to 34 indicated they would rethink their home buying plans in some way, compared to 36 percent of adults aged 55 or older (figure 3).

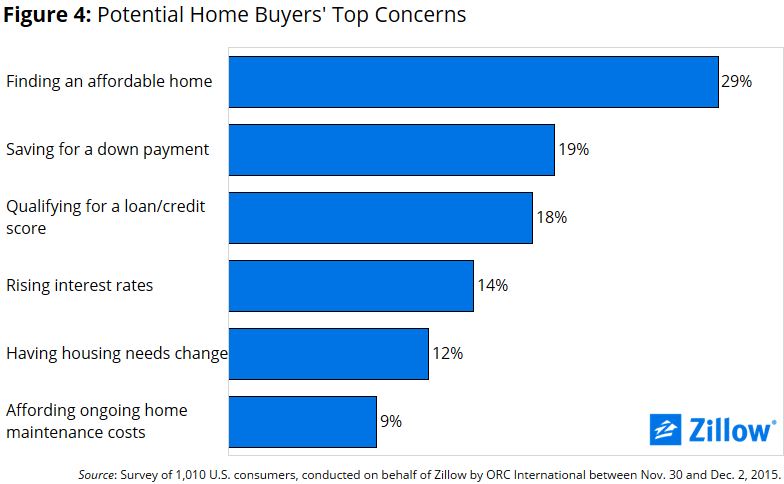

But really, rising interest rates rank relatively low among the top concerns of home buyers. Price and availability of homes within a given budget are the leading concerns among respondents currently in the market or who expect to be in the next year. More than a quarter (29 percent) of respondents cited “finding an affordable home” (which we broadly interpret as concerns about inventory and price) as the top factor that may impact their ability to buy a home within their preferred timeline (figure 4). The next most commonly cited concerns were saving for a down payment (19 percent) and qualifying for a loan/concerns over credit scores (18 percent). Rising interest rates ranked fourth among the six options given (14 percent).

Of course, interest rates are a key part of the overall affordability of a given home. But the reality is that even after interest rates begin to rise, they’ll rise slowly and mortgage rates will remain near historic lows for a while yet. And even when rates rise above 5 percent and even 6 percent, buying a home is likely to continue to be more affordable than it has been in the past. In more than 80 percent (410) of the country’s largest 500 metro markets, the monthly mortgage payment would increase by less than $50 per month on the area’s median-priced home (assuming a 20 percent down payment). For the median home in the United States, the monthly mortgage payment would increase by $43 per month, or $516 per year – a meaningful sacrifice for many, but hardly devastating, especially assuming a potential home buyer buys a home within their means and isn’t overly stretched to begin with.

And finally, it’s important to remember that what a home buyer earns today is likely not going to be what they earn tomorrow. Especially considering that the vast majority of home buyers will lock in their mortgage rate and expenses for 30 years (and may soon forget their precise mortgage rate anyway), even modest income growth after one year will help cover the added expenses of a rise in rates to 4.5 percent. Assume a home buyer has an annual household income of $50,000 (slightly less than the national median household income of $53,657), and gets a 1.5 percent cost of living raise after a year – not a given, but also not a stretch, considering incomes overall grew by 2.3 percent last year.

That small raise would translate into an extra $750 per year, more than making up for added housing costs of around $50 per month.