July Real Estate Market Reports: When Turning Negative is Actually a Positive

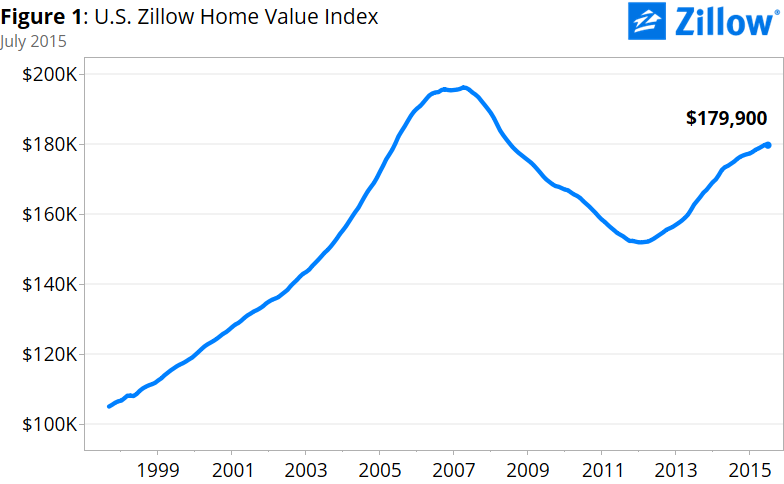

- In July, the median U.S. home value was $179,900, up 3 percent from a year ago, but down 0.1 percent from June – the first monthly decline since January 2012.

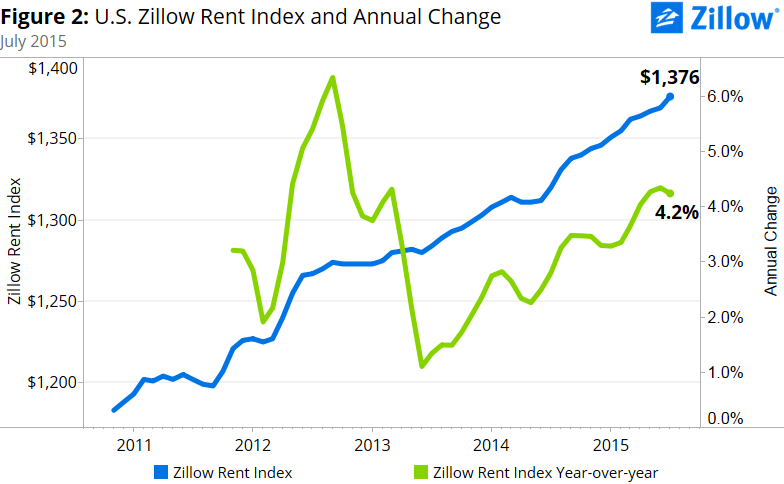

- Rents continued their rapid appreciation, up 4.2 percent from last July.

- Slower home value growth could be a boon for potential buyers and may entice some potential sellers to list their homes, boosting inventory.

In July, for the first time in almost four years, the typical U.S. home was worth less than it was a month ago.

The median U.S. home value fell by 0.1 percent in July from June, to $179,900 from $180,000. Year-over-year, home values grew 3 percent, down from a 3.4 percent annual pace in June. The slowdown comes on the heels of years of very rapid monthly and annual U.S. home value growth in the period immediately following the market’s bottom in late 2011 and early 2012.

As recently as April 2014, national home values were growing 0.9 percent per month and 8.6 percent year-over-year. Even very hot markets including Denver, Dallas, San Jose and San Francisco – all of which experienced double-digit annual home value growth in July – saw their monthly appreciation rates ease from June.

The monthly decline may be something not seen on a national stage in years, but locally, monthly growth has been sputtering for months. Home values in both Baltimore and Washington, D.C., for example, have fallen month-over-month in each of the past three months. In Chicago, monthly home value growth was negative for three consecutive months in December, January and February before rebounding in the spring and early summer. Even Los Angeles, where recent home value growth has been among the highest in the nation at times, experienced a small home value decline in December from November.

As the market continues to stabilize and find its true footing after the boom, bust and recovery periods of the past decade or so, these kinds of slowdowns should be expected to crop up more often. But far from being a cause for concern, a month of home value declines here and there is actually a welcome sign of normalization. Slowing home value growth could provide more opportunities for hopeful buyers who have been waiting on the sidelines for the market to cool off. A slower-moving market gives these buyers more time to save for a home and find a home to buy, and also may entice some potential sellers to list their homes for sale if they begin to figure they’ve ridden the wave of home value growth long enough.

For millions of Americans, our homes are often our fairy tale castles. And an old fairy tale adage holds true for housing: Slow and steady wins the race, and a return to a slower, steadier housing market will be a big benefit in the long-run.

Monthly Home Value Growth Turns Negative

In July, seven of the 35 largest markets covered by Zillow experienced monthly declines in home values (Washington, D.C.; Cincinnati; Baltimore; Phoenix; Sacramento; Minneapolis and Boston), while another three were flat compared to June (Pittsburgh; Riverside and Philadelphia). Two of the largest 35 markets also experienced annual declines in home values in July (Washington, D.C., and Baltimore).

But even as the national market cools off a bit, a handful of local markets continued to sizzle this summer. Four of the largest 35 markets analyzed by Zillow experienced double-digit growth year-over-year in July: San Francisco, San Jose, Dallas and Denver. Among all markets analyzed, annual home value growth was higher than the nation as a whole in 244 (47.2 percent), slower in 269 (52 percent) and the same in three.

Rents Keep Rising

All but two (Chicago and Pittsburgh) of the 35 largest markets covered by Zillow experienced annual rental growth in July. Among large markets, year-over-year rental growth was highest in San Francisco (up 14.1 percent), Denver (up 12.6 percent) and Portland, Oregon (up 11.2 percent). Rents rose year-over-year in 631 of the 861 metropolitan and micropolitan areas covered by the ZRI (73.3 percent).

Rental affordability is a growing issue in many local markets. Nationally, as of the end of Q2, renters making the U.S. median income and looking to rent the median-priced rental home should expect to pay 30.2 percent of their income each month to their landlord, up from 29.5 percent at the midpoint of 2014 and 24 percent historically. In 28 of the largest 35 metro areas analyzed by Zillow in the second quarter, rental affordability worsened in the past year.

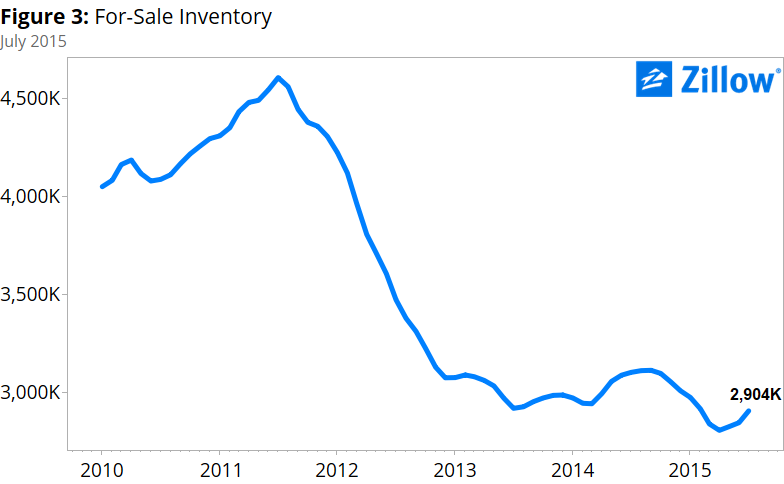

Inventory Remains Down

Outlook

Over the next year, home value growth is expected to slow even further, to 1.5 percent through July 2016, according to the Zillow Home Value Forecast. Over the past year, home values grew 3 percent.

We’ve been expecting home values to turn negative on a monthly basis for some time, so the slight dip is not very worrisome to us, and is a sign of the times and of a market getting back to more normal, sustainable levels. This dip is not like the bubble bust, and we’re not going to start seeing 10 percent annual declines again any time soon. The market is leveling off, and that’s good news, particularly for buyers, because it will ease some competitive pressure.