June Home Sales: Positive Signs for Summer Home Sales as New and Existing Expected to Rise

- Zillow expects existing home sales to rise 1 percent month-over-month to 5.40 million units (SAAR) in June, and new home sales to rise 2.5 percent to 560,000 (SAAR).

- These increases would bring combined new and existing home sales to their highest level since November 2009 when the first-time buyer tax credit boosted home sales.

- Anticipated interest rate hikes sometime this year will likely hurt home sales to some degree, though the impact could be muted by stronger income growth recently and a healthier job market.

Sales of existing and newly built homes are expected to move in the same direction in June, with new home sales volume rising more from May than existing home sales, according to a Zillow forecast of data scheduled for release next week.

Zillow expects Wednesday’s June existing home sales data from the National Association of Realtors (NAR) to show a monthly increase of about 1 percent, to a seasonally adjusted annual rate (SAAR) of 5.40 million units, up from 5.35 million units (SAAR) in May. We expect Friday’s June new home sales data from the U.S. Census Bureau to show a monthly increase of about 2.5 percent, to a seasonally adjusted annual rate (SAAR) of 560,000 units, up from 546,000 units (SAAR) in May. The combined increase would bring total new and existing home sales to their highest level since November 2009, when federal homebuyer tax credits helped boost home sales.

Zillow expects the median price of a new home to rise to $282,800 (SA) in June, up 1 percent from May, and the median existing home price to rise to $223,400 (SA), up 1.3 percent from May[i].

Background

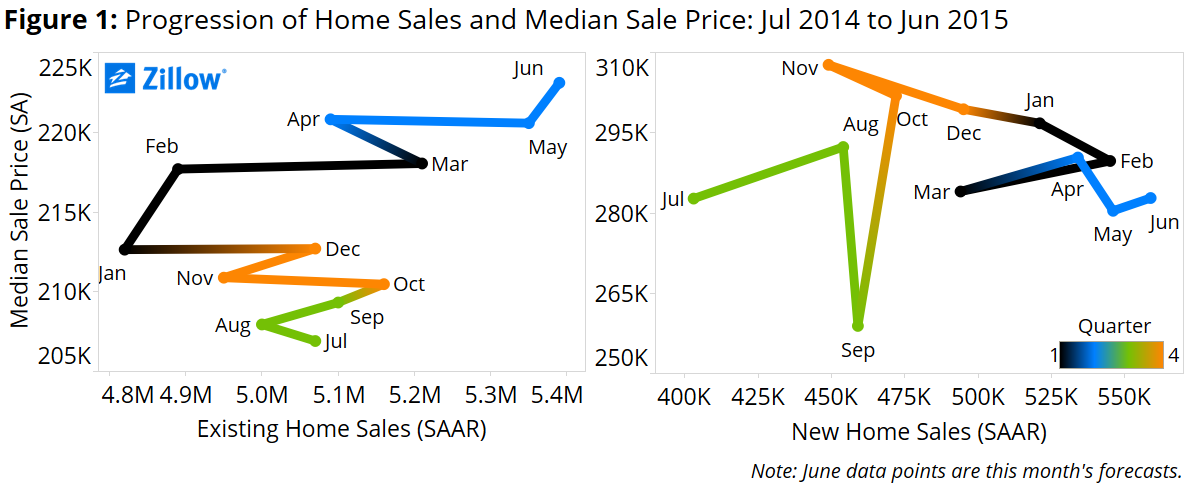

Both new and existing home sales made positive strides through the first five months of 2015, and we expect they will end the second quarter on a high note. Existing home sales have increased in four of the past five months compared to the month prior, with 1.93 million sales recorded so far this year, up 6.3 percent from the same period last year. As sales have grown over this time, prices have also risen, up 7.9 percent in May from a year earlier. The median price of an existing home is currently $220,600, up from $204,400 a year ago.

Sales of newly constructed homes have also increased in four of the past five months, accumulating 232,000 sales, a 22.8 percent spike from the same period last year. But unlike existing homes, the price of a typical new home has been declining as builders construct less expensive homes aimed at a more modest segment of the market. The median price of a typical new home is currently $280,400, down about 1 percent from $283,000 a year ago (figure 1).

Housing demand should pick up through the summer home shopping season, given recent improvements in the job market and rapidly improving income growth. After six long years of persistently high unemployment, the unemployment rate has finally reached (and is actually slightly below) [i] the estimated natural rate of unemployment.[ii] Monthly personal income grew by 3.7 percent year-over-year during the first half of 2014, on average. That growth has accelerated in 2015, growing 4.4 percent year-over-year, on average. Accelerating income growth has been accompanied by persistently low mortgage rates, making a mortgage itself more affordable relative to historic norms. The share of income devoted to a mortgage payment on the typical U.S. home, assuming the borrower makes the U.S. median income, fell to 14.6 percent compared to 15.4 percent in 2014 Q1 and 21 percent historically.

But interest rates have been ticking up recently, and are expected to increase more in the near future, which will likely cause mortgage affordability to suffer somewhat. Despite unease over the latest Greek bailout, Federal Reserve Chairman Janet Yellen’s recent monetary policy testimony before Congress remains consistent with the belief that an increase in the federal funds rate will likely come towards the end of 2015.

How sensitive will home sales be to a hike in the federal funds rate? In June 2013, when then-Fed Chairman Ben Bernanke announced the Fed would scale back its “quantitative easing” program, the 30-year conventional mortgage rate jumped 95 basis points between May and September (the so-called “taper tantrum”). Sales of new homes fell almost 19 percent in the month following the announcement, while existing home sales fell 12 percent between July 2013 and January 2014. An increase in mortgage rates in coming months will likely hurt home sales as markets begin to anticipate interest rate hikes. Stronger job markets and more robust income growth now compared to 2014 may help mute the overall impact.

Existing Home Sales Outlook

For sales activity to pick up in the coming months, the supply of homes for sale, both existing and new, needs to be large enough to support anticipated strong demand. While inventory constraints have been tight recently, as of May, the supply of homes available for sale was slightly higher than a year ago[iii]. Paired with expectations of future rate hikes that may spur more potential buyers to pull the trigger on a home purchase sooner rather than later, this suggests the potential for a better summer selling season than last year.

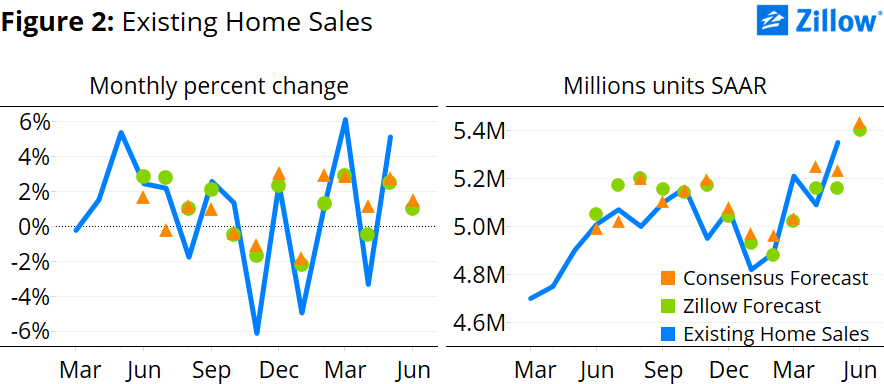

Pending home sales have increased in every month this year, and were up 10 percent year-over-year in May, according to NAR. The supply of existing homes for sale was almost 2 percent higher in May than a year ago, the highest level since October 2014. Higher pending sales typically indicate higher existing sales volume over the next few months, as pending sales transition to closed sales. And with short-term inventory constraints lighter than last summer, this should provide some boost to existing sales in June (figure 2).

While there are some positive signs for inventory in the short-term, longer-term inventory shortages are likely to remain. Persistently high negative equity is preventing millions of mortgaged homeowners from listing their homes for sale and subsequently buying a new home, particularly those at the bottom end of the market stuck in homes likely to be attractive to first-time buyers. With many homeowners relatively deep underwater, home value growth alone may not be enough to lift them above water, meaning negative equity-driven inventory shortages may persist for years.

New Home Sales Outlook

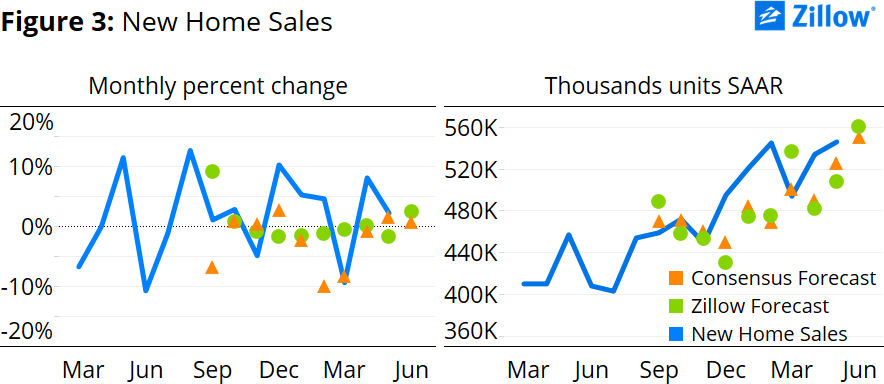

The combined number of new homes completed and ready for sale in April and May was up 8.3 percent from the same time last year, which bodes well for summer sales (figure 3) as it typically takes about four months for a new home to sell once it is completed.[i] But longer-term, inventory of new homes will likely remain low. Growth in the rate of construction of new homes so far in 2015 has surpassed the 1990’s rate of roughly 4 percent year-over-year. If construction starts continue to grow at the current year-over-year rate of about 7 percent[ii], home construction levels won’t reach their 1995 level until 2021, and won’t get back to their pre-Crisis levels until 2030.

June Forecast

Our home sales forecast estimates an error correction model that takes into account the estimated long-run relationship among housing market fundamentals and monthly changes.

According to this model, both existing home sales and new home sales are below their estimated long-run relationship in the market. The error correction mechanism alone suggests a 3 percent increase in sales for both new and existing homes. But monthly changes in other housing market data – including pending home sales, inventory, new home construction, median sales prices and mortgage expenses – should dampen the effect of the correction, more so for existing home sales.

[i] According to the U.S. Census Bureau.

[ii] The current growth rate of new home construction of is calculated as the average monthly year-over-year growth rate over the past 12 months.

[i] According to the U.S. Bureau of Labor Statistics and U.S. Congressional Budget Office estimates obtained from the St. Louis Federal Reserve Economic Data (FRED).

[ii] The unemployment rate can be misleadingly low. If discouraged and marginally attached workers are included, the unemployment gap would be more than 1 percent.

[iii] According to the National Association of Realtors (NAR).

[i] The forecast of the median sale price is determined within the error correction model, and helps us get a sense of where the housing market will be this month in terms of a supply and demand framework.