For Many Low-Income Households, Even Low-Valued Homes Aren’t Affordable

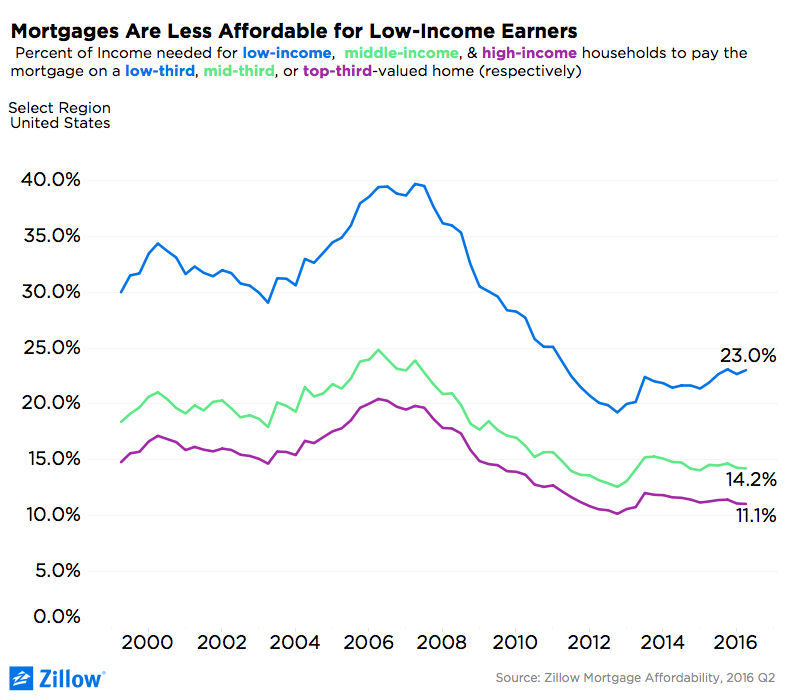

- Households with incomes in the bottom third spend 23 percent of their incomes on mortgages for homes valued in the lower third.

- That’s more than twice the 11.1 percent that a typical high-income homeowner pays for a home valued in top third of homes nationally.

- That inequality worsens in pricey coastal markets.

Historically, the typical homeowner spent about 21 percent of her income on a mortgage. That share of income has declined to 15.9 percent, making homeownership in general more affordable. Although home values have grown more quickly than incomes in recent years, low mortgage rates have made monthly mortgage payments fall relative to income.

The financial picture is far different for low-income homeowners. Households with incomes in the bottom third nationally now spend 23 percent of their incomes on mortgages for homes valued in the bottom third of homes. That’s not far off the historical average – but it’s more than twice the 11.1 percent that a typical high-income homeowner pays for a home valued in top third of homes nationally.

The inequality worsens in pricey coastal metros. In Los Angeles, low-income homeowners pay 79 percent of their incomes on a mortgage for a lower-end home, while upper-income homeowners pay just 26.7 percent for homes at the pricey end.

The gap is widening, in part because high-end homes are appreciating more slowly than low-end homes, and in part because incomes among the top third of earners are growing faster.

As unequal as the situation is, it’s worse among renters. While renters overall pay about 29 percent of their incomes on rent, at the median, low-income renters in 24 out of 25 of the country’s largest metro areas pay more than 45 percent for low-end rentals.