The War at Home: Examining Home Values Near Military Facilities

- Homes near military bases are valued, on average, 34.8 percent more than the median U.S. home.

- Homes near Army bases are the most affordable, but are still valued roughly $50,000 more than the U.S. median. Homes near Navy, Coast Guard and Marine bases are valued at $90,000 or more than the national median.

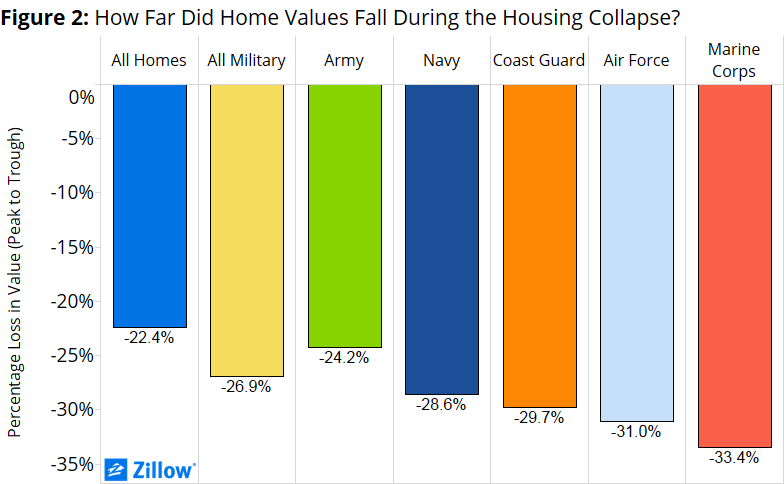

- Home values near military bases fell harder during the recession, down on average 26.9 percent from the peak of the market to the trough, compared to 22.4 percent for all U.S. homes.

The decision to purchase a home is complex and filled with uncertainty for any potential homebuyer. Add in the uncertainty already inherent as an active-duty military member, along with sometimes-volatile home values near military bases, and things can get even more difficult.

On top of the normal decisions faced by homebuyers, members of the military must decide if living on- or off-base best suits their financial and social needs. They also face unplanned reassignments, often needing to list and sell their current home at a moment’s notice, which has huge implications on the decision to rent or buy.

In order to gain a greater understanding of some of the issues facing members of our armed forces, Zillow analyzed the value of homes near military bases over time as a means of gauging just how volatile they can be. This is the first in a planned series of analyses examining housing issues among military members and their families.

Home Values on the High Ground

As it turns out, homes near military bases are worth substantially more than the national average. In March, the median U.S. home was valued at $178,400. But the average home near a military base was valued at $240,553, a 34.8 premium. This trend wasn’t confined to homes near bases of any specific branch, either: Homes near bases for all five of the major U.S. military branches (Army, Navy, Air Force, Marines and Coast Guard) are worth more than the national average (figure 1).

Homes near U.S. Army bases are the most affordable, but they’re still valued $50,000 more than the national average. At the high end of the spectrum, members of the Marines, Navy or Coast Guard searching for a home near their base can expect to find homes valued at $90,000 or more than the national median. This may be unsurprising, given that these bases – and, subsequently, nearby homes – are typically near the coast, and living close to the coast comes at a premium.

Collateral Damage

When the housing market reached bottom in the wake of the Great Recession, U.S. home values on average had fallen by 22.4 percent. But homes near bases of every branch of the military fared worse. On average, homes near military bases lost 26.9 percent of their pre-recession value.

This is especially concerning, given the frequency at which military personnel must uproot and move. When home values fall drastically, many homeowners can simply wait out the fall and sell if and when values rebound. Members of the military don’t necessarily have this luxury. If they get notice of a permanent change of station, they typically have no other option but to sell their current home – which could mean a substantial financial loss at best, or may be near impossible at worst if they’ve fallen far enough into negative equity.

If military members do end up needing to sell their home for less than what they currently owe on their mortgage, there are specific programs available to them where the Department of Veterans Affairs (VA) will step in and cover the difference (a VA compromise sale). While this helps prevent military personnel from owing money on a home they no longer own, this protection doesn’t extend to a homeowner’s equity stake in their home. For example, consider the following two military homeowners:

| Military Homeowner A | Military Homeowner B | |

| Purchase Year | 2007 | 2005 |

| Purchase Price | $250,000 | $500,000 |

| Sale Year | 2010 | 2010 |

| Sale Price | $200,000 | $400,000 |

| Outstanding Mortgage | $230,000 | $375,000 |

| VA Covers | $30,000 | $0 |

| Owner Equity Loss | ($20,000) | ($100,000) |

Homeowner A bought his home for $250,000 and had to sell for $200,000. Because he still owed $230,000, the VA would cover $30,000 left on the mortgage. The owner would still lose the $20,000 he had invested in the home.

Homeowner B bought her home for $500,000 and had to sell for $400,000. Since the remaining balance on her VA loan was only $375,000, the VA would not have covered any of her losses, meaning that $100,000 loss would fall squarely on the homeowner.

Additionally, this protection (however limited) only applies to those homeowners with a VA loan. While most military members are eligible to apply for VA financing, not all choose to finance their home purchase through the VA. For those that don’t, very little protection – if any – is available in the event of negative equity.

Off-Base

While the national numbers are compelling, home values can vary from base to base. For this reason, we also analyzed home values in the areas surrounding 18 of the largest military bases in the country (figure 3)[i].

Methodology

Our analysis covers 391 military bases across the country. To capture the cost of living near a military base, we assumed military personnel would be willing to cross one full ZIP code during their commute. Meaning for each military base, we included the base’s ZIP, all neighboring ZIPs, as well as all ZIP codes surrounding those direct neighbors.

We also weighted each ZIP by the proportion of active duty U.S. military residing there[ii]. This weighting offers two advantages. First it allows us to better capture where military personnel actually concentrate around bases.[iii] Second it enables us to control for the size of each base when we aggregate up to calculate a national number. Otherwise we would be giving equal weight to all bases, regardless of how many citizens each employs.

[i] Here is a list of which bases comprise each of these base groupings:

San Diego (MCB Camp Pendleton, Naval Base San Diego, MCAS Miramar, NAS North Island, Naval Base Point Loma, NTC San Diego, USCG San Diego, San Diego Naval Medical Center); Norfolk (Naval Shipyard Norfolk, Naval Station Norfolk); Camp Lejeune; Joint Base Bragg-Pope; Vandenberg AFB; Colorado Springs (Fort Carson, Peterson AFB, Schriever AFB); NAS Pensacola; Fort Hood; Joint Base Lewis-McChord; Fort Campbell; Joint Base Andrews; Fort Benning; Joint Base Pearl Harbor-Hickam; Jacksonville (NAS Jacksonville, Naval Station Mayport); Naval Base Kitsap; Twentynine Palms; Joint Base McGuire-Dix-Lakehurst; USCG Elizabeth City

[ii] Source: five-year 2013 ACS data.

[iii] ZIP codes vary both in size and number of residential properties, meaning that in some cases we may be incorporating ZIPs that are unreasonable areas for military personnel to reside. We account for these potential problems by weighting the ZIPs by the proportion of the military who reside there.