What Modern-Day Housing Discrimination Looks Like: A Conversation With the National Fair Housing Alliance

Lisa Rice, President and CEO National Fair Housing Alliance

For many Americans, housing discrimination is a fact of life. Redlining and other policies and practices have contributed to a widening in the black-white homeownership rate gap over the past century, despite legal protections that apply by race and 11 other legally protected designations.

Zillow teamed up with the National Fair Housing Alliance (NFHA) to survey 10,000 adults in the largest 20 metro areas nationwide about housing discrimination. The Zillow Housing Aspirations Report (ZHAR) survey conducted in October 2018 found that roughly one in four adults believe that over the course of their lives, they’ve been treated differently in their search for housing due to illegal discrimination.

NFHA President and CEO Lisa Rice works every day to combat housing inequality and discrimination. Zillow Research had a conversation with Lisa on her insights about some of the eye-opening results gleaned from the ZHAR survey.

Zillow Research (ZR): In this survey, 27 percent of Americans said they believe they’ve been treated differently in their search for housing because of their status in a protected group – which, applied to the U.S. population, would mean about 68 million adults. Does that seem high, low or about right to you?

Lisa Rice (LR): It is not surprising at all that more than roughly one in four of surveyed adults believe they have experienced a form of housing discrimination in their lifetimes.

In 2004, NFHA commissioned John Simonson, an economist with the Center for Applied Public Policy at the University of Wisconsin, to project the level of discrimination experienced by people of color who are either attempting to rent an apartment or purchase a home. He projected that roughly 4 million people who fit this category experience illegal discrimination each year.

When you add together the additional protected classes – people with disabilities, people experiencing barriers based on their gender, religious affiliation or national origin, families with children, etc., it is not difficult to see how this number could easily reach the 68 million that resulted from the ZHAR survey. In fact, the 68 million projection might seem low.

ZR: What forms of discrimination do people typically experience around housing now? Has that changed over the decades?

LR: The largest category of official fair housing complaints is disability status. That has changed over time. Historically, race-based complaints made up the largest complaint category; it is now the second-largest basis for complaints. But it is important to note that only about 28,000 total discrimination complaints get reported each year. With an estimated 68 million believing they have experienced housing discrimination, that means that the vast majority of fair housing violations do not get reported. This is in large part because most discrimination is hard to detect. Or when people believe they’ve experienced discrimination, they don’t know where to go for help.

ZR: Does discrimination look different depending on what protected class someone is in? For example, how would people searching for housing experience discrimination by skin color versus gender versus disability status versus Social Security income or disability insurance?

LR: Discrimination can take on different forms — making it really hard for someone to recognize that they are experiencing unfair treatment.

- Real estate agents can refuse to return phone calls.

- Loan officers can steer borrowers to higher cost loan products.

- Landlords can give false information about the availability or cost of a unit.

- Insurers can tell prospective customers that they don’t meet eligibility requirements.

- Appraisers can artificially deflate property values.

- Property managers can deny a request to install a wheelchair ramp.

- Lenders can deny a woman’s application because she is on maternity leave or not allow a person to use their SSI income.

- Single mothers, especially women of color, who are the head of their households are disproportionately impacted by landlords who use aggressive eviction techniques.

- Victims of domestic violence, who tend to be women, can be negatively affected by Zero Tolerance policies.

So discrimination does not always look the same – even for the same groups of people.

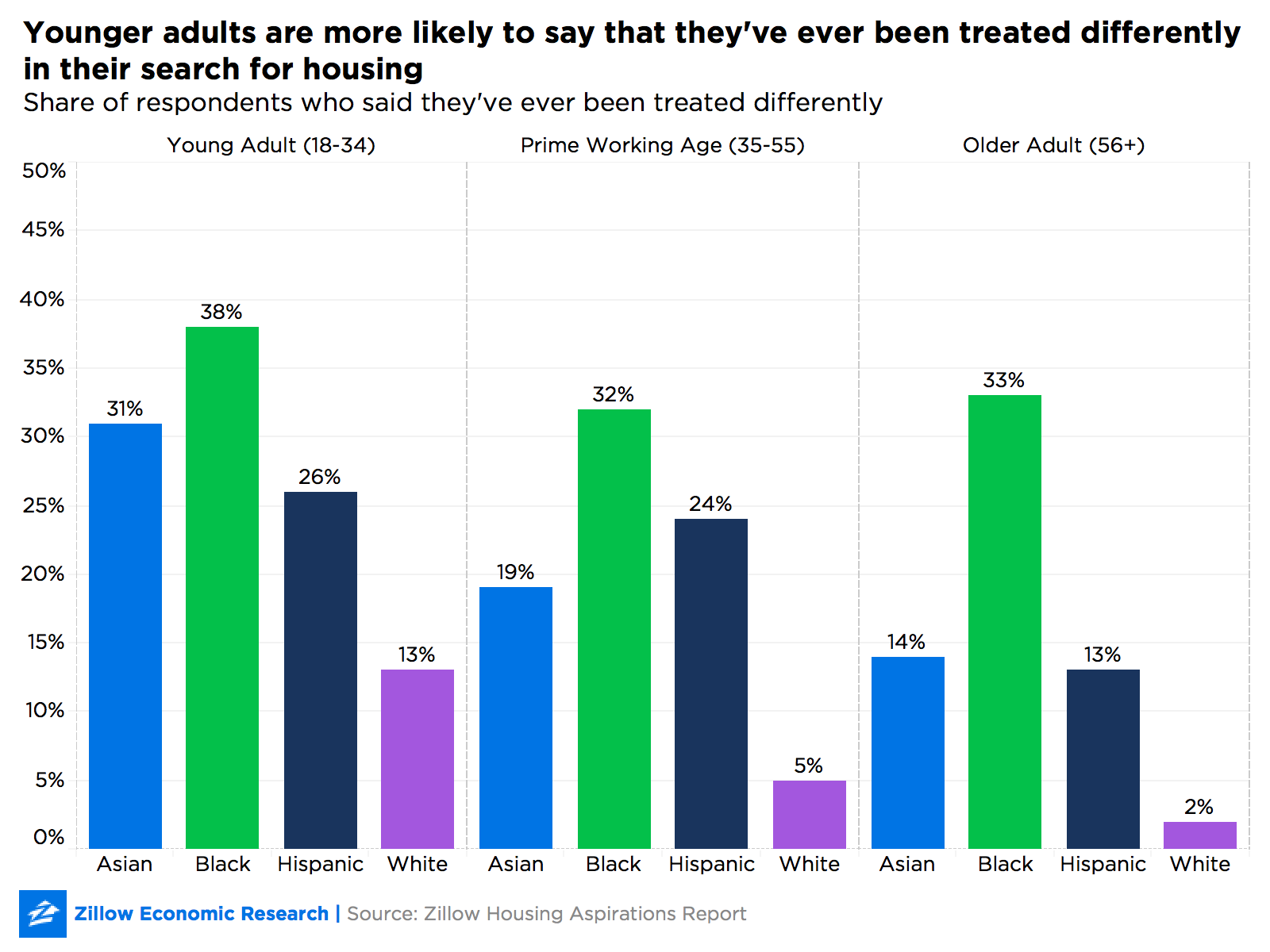

ZR: What might account for the perceived differences by age, with younger people being more likely to say they were treated differently?

LR: Younger people account for the largest percentage of moves and in 2017 were 19 percent more likely than those aged 35 to 54 to move. Younger people were 32 percent more likely to move than those aged 55 and up. It may just be that because younger people are moving at higher rates, they are more likely to be exposed to discriminatory barriers in the housing market. Moreover, compared to previous generations like the Baby Boomers and Generation Xers, millennials are the most racially and ethnically diverse generation and consumer base. If past practices are any indication of current consumer experiences, it stands to reason that this group will see more instances of discrimination.

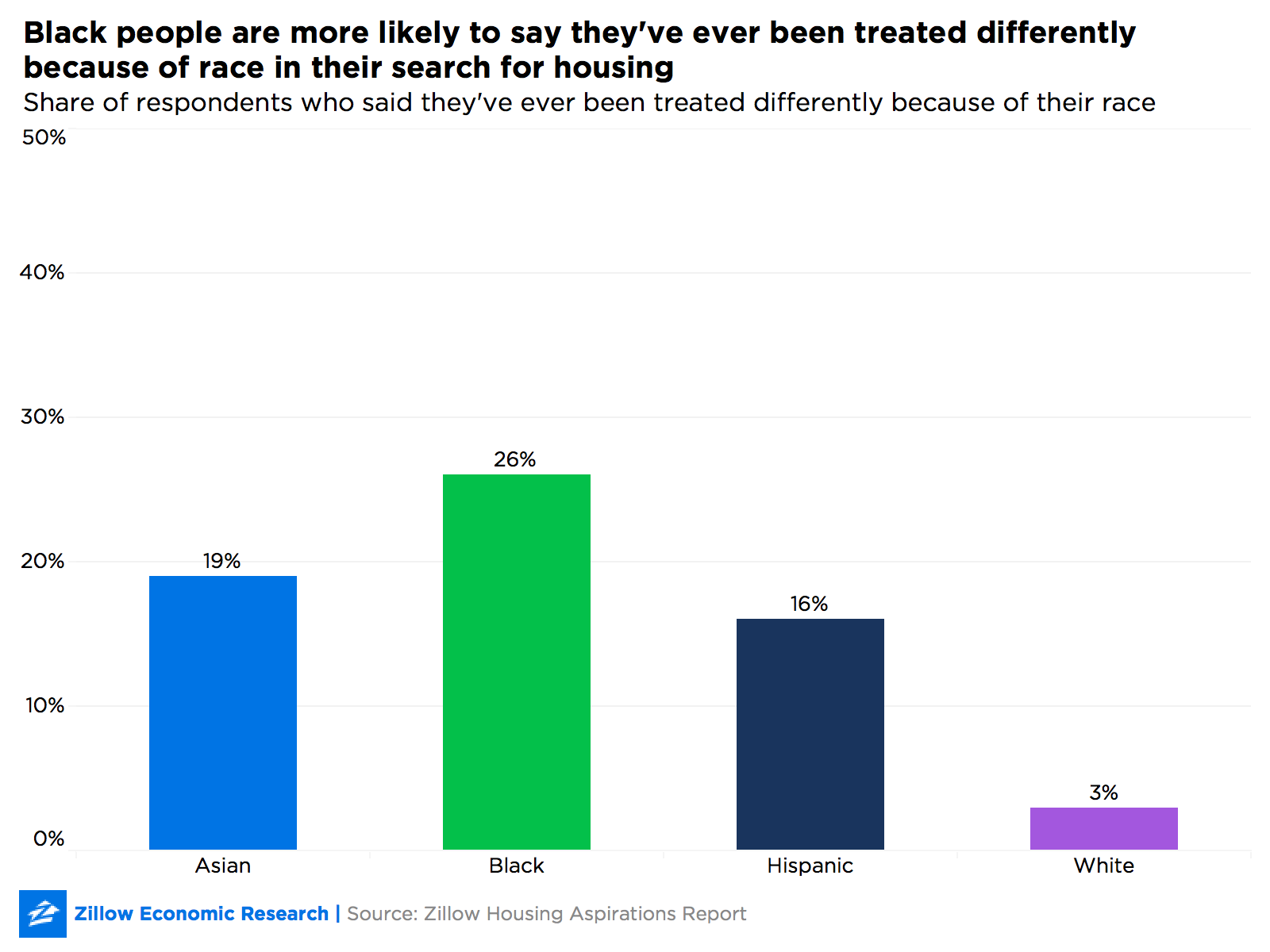

ZR: Black respondents are far more likely (26 percent) to say they’ve been treated differently because of race than Asians (19 percent), Hispanics (16 percent) and whites (3 percent). Does that fit with the reality you see, and if so, why do you think that is?

LR: Recent news accounts describing how African Americans are targeted with violent or discriminatory treatment highlight what these consumers face in many areas, including the housing market. Studies show that African Americans are more likely to face discrimination in employment, housing, health, criminal justice and other sectors.

These types of systemic barriers have far-reaching implications and affect things like your credit or insurance score and are a partial explanation of why African Americans feel more impacted by discrimination.

ZR: One of the most striking survey results is that 30 percent of blacks consider discrimination a barrier to owning a home, far higher than any other group surveyed. That was historically true because of redlining, racial covenants and other racist behaviors in the market. What is happening now to keep black people out of homeownership? What barriers do they face that people in other racial and ethnic groups do not?

LR: The historical barriers that were designed to deny housing opportunities to African Americans and create residential segregation are still with us today. We are more segregated today than we were 100 years ago. Communities of color still have less access to the amenities and services that people need to thrive. African Americans and Latinos were disproportionately impacted by the foreclosure crisis and these communities still have not fully recovered. In fact, the homeownership rate for African Americans is where it was 50 years ago when the Fair Housing Act was passed. Homeownership gains made by African Americans were wiped out as a result of these consumers being targeted by subprime lenders. The United States has a 200-plus year history of implementing government-sponsored policies that deliberately discriminated against African Americans.

But our government has never done anything to rectify the harm it caused to communities of color. The challenge is that the explicit biases built into our housing and finance systems are today manifested implicitly in the way we assess borrower risk and price consumers for accessing housing and housing related services. African Americans still face outright discrimination but they are also disproportionately credit invisible and more likely to have deflated credit scores. The widespread discrimination in our lending and housing markets is something this nation must face and effectively address if housing equality and broader economic justice is to become a reality.

ZR: What should be done to expand equal housing opportunities? Is there a role for the housing industry to play? Is there a role for government to play?

LR: Answering this question is not easy because, as described, housing discrimination has a long history in our country. There have been many players, and problems still persist. The ZHAR survey results represent real people who are struggling with accessing housing – a basic life need. There is a role for everyone to play in ameliorating this problem. People who believe they are experiencing discrimination should contact their local fair housing organization. These groups are extremely helpful. The housing industry can educate itself about fair housing laws, partner with fair housing organizations, examine policies and procedures to ensure they are non-discriminatory, hire diverse staff, and provide consistent customer service to all consumers. Local, state, and federal governments can take their obligation to affirmatively further fair housing seriously by partaking in comprehensive fair housing planning that connects with local Consolidated Plans, supporting fair housing agencies, educating the public about equal housing opportunities, and enforcing and bolstering fair housing laws and regulations.