Revisiting Mortgage Lending in Detroit: New Insights From HMDA

- Mortgage lending continued to pick up in Detroit in 2014, but remains well below the rates seen in comparable cities.

- Neighborhoods with stronger purchase originations in 2013 have experienced strong home value appreciation in the two years since.

- Mortgage application denial rates have come down, particularly for conventional purchase loans.

Detroit’s housing market is – slowly, seemingly perpetually – “getting there,” recovering in fits and starts and unevenly throughout the roughly 150-square-mile city that is home to more than 600,000 residents.

The number of purchase mortgages written is rising, though remains disconcertingly low for a city of its size. The mortgage denial rate is improving, but still staggeringly high. Home values are showing robust growth in a small handful of the city’s most popular neighborhoods, while in the rest of the sprawling city, home value growth has been far more subdued.

Detroit is turning a corner, but is not yet through a tricky three-point turn.

Zillow visited Detroit in May as part of our Housing Roadmap to 2016. Our analysis of 2013 data from the Home Mortgage Disclosure Act (HMDA) illustrated some of the challenges of mortgage lending in communities where homes often require substantial investment, leading to low appraisals. Armed with the most recent (2014) HMDA data, we’ve revisited that analysis, and discovered that while much has changed for the better in Motown, the city’s housing recovery still lags substantially behind similarly hard-hit American cities.[1]

Mortgage Originations Better, But Still Low

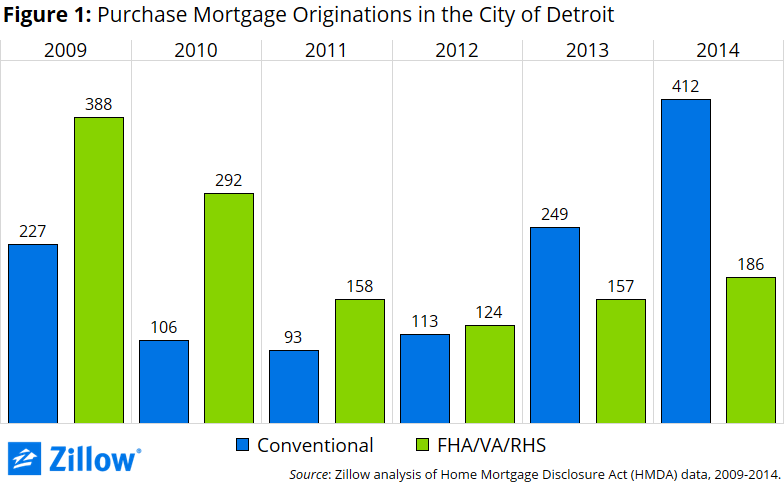

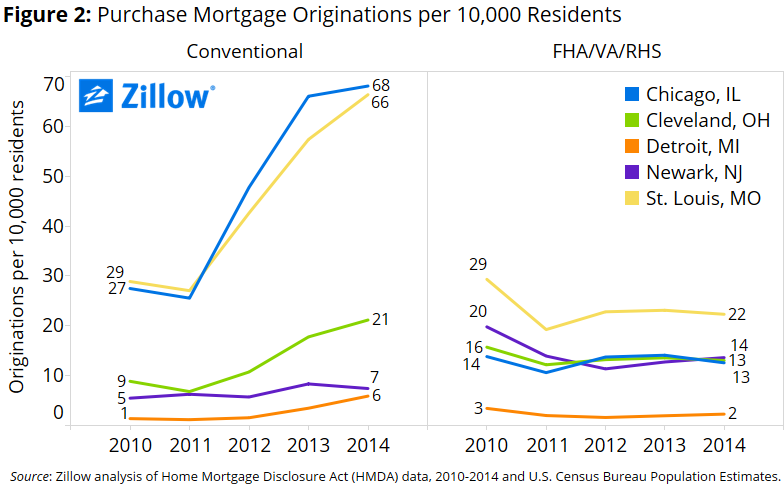

Purchase mortgage originations have continued to rebound in Detroit from historic lows recorded in 2011 and 2012, largely driven by growth in conventional mortgages (figure 1). But the overall number of originations remains well below origination rates for comparable, nearby cities. In 2014 there were only six conventional purchase mortgage originations per 10,000 Detroit residents, compared to 21 in Cleveland and 68 in Chicago (figure 2).

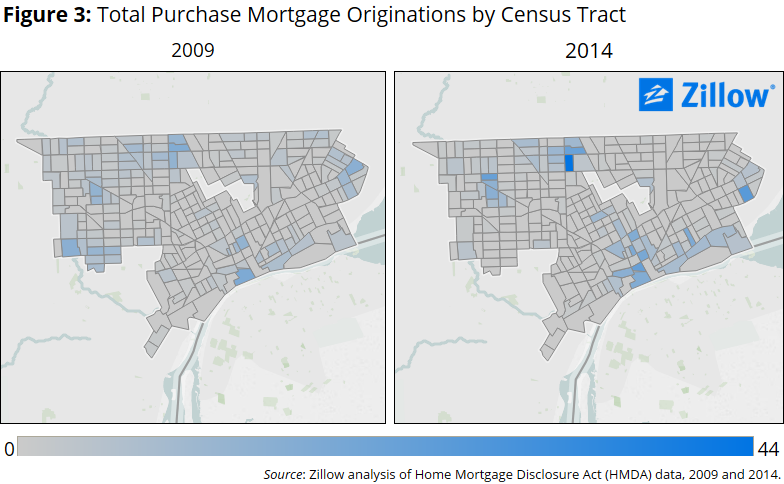

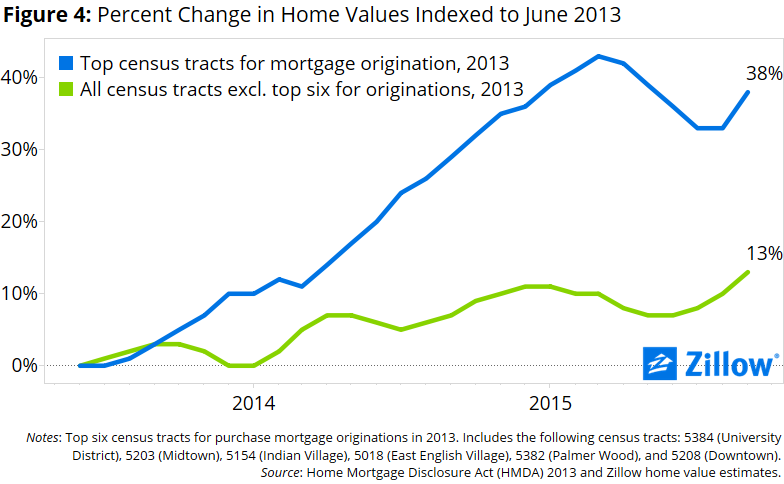

Purchase Originations, Appreciation Concentrated in a Few Neighborhoods…

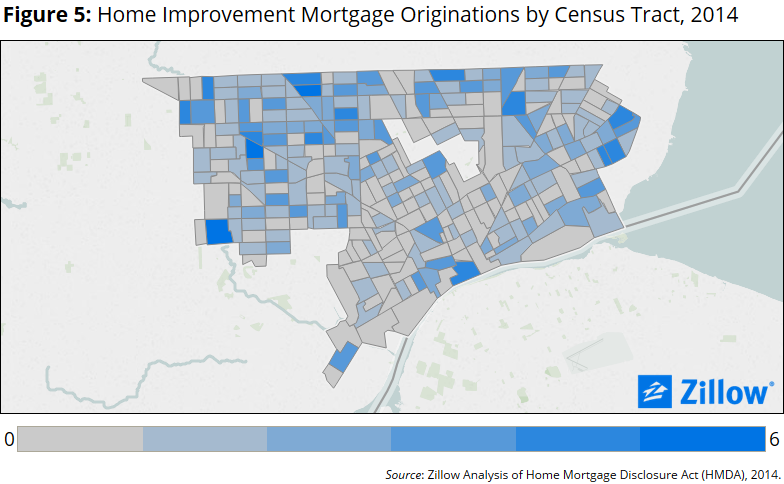

…But Home Improvement Loans are Increasingly Popular Citywide

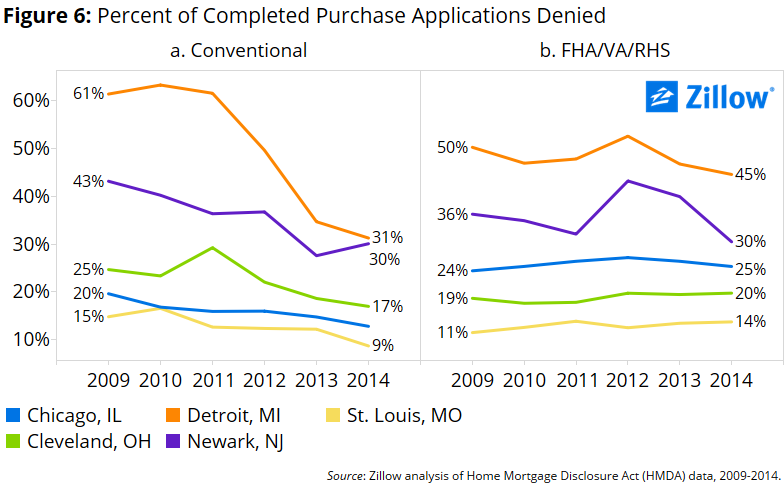

Mortgage Denial Rates Have Improved Remarkably

But while conventional mortgage denials have fallen precipitously, the decline has been less impressive for FHA and VA mortgages, and remains substantially higher in Detroit than in other cities (figure 6b). Last year, almost half (45 percent) of FHA/VA purchase mortgage applications were denied in Detroit, compared to 30 percent in similarly blighted Newark, and 14 percent in St. Louis.

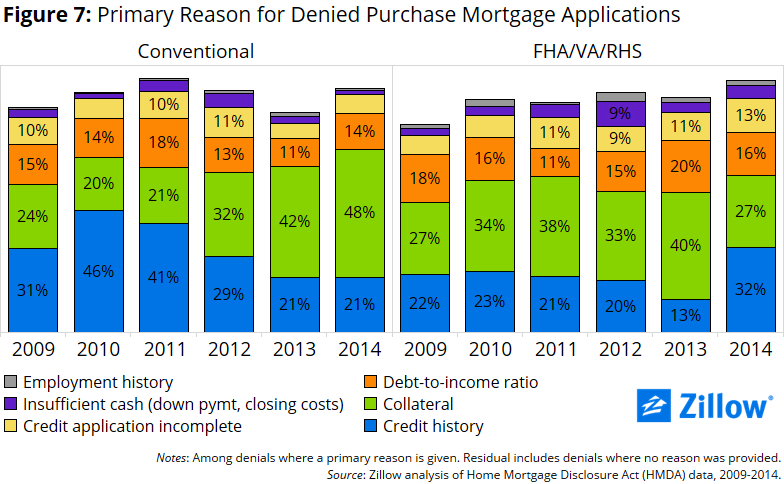

Collateral Still a Barrier, Along With Credit History

As in 2013, insufficient collateral remained the most common reason cited for denying conventional purchase mortgage applications in Detroit last year, followed at a distance by insufficient credit history and too-high debt-to-income ratios (figure 7). Among FHA/VA purchase mortgage applications, credit history overtook collateral as the most common reason for application denials in 2014.

Two Steps Forward…

Detroit’s decline, culminating in recent years with the city’s 2013 bankruptcy, was decades in the making. In light of this long history, it’s unreasonable to expect its recovery to be quick, or even complete. Instead, the city is recovering in fits and starts. Some areas are prospering, while others still hope for a more robust turnaround. Compared to other nearby cities, Detroit’s housing market continues to confront enormous challenges. But green shoots are very clearly starting to emerge.

[1] Unless otherwise noted, data presented here are at the city level.