How Mortgage Payments Vary With Interest Rates, Loan Products

The 30-year, conforming, fixed-rate mortgage has become the bedrock of housing finance in America. But as discussions evolve around reforming mortgage giants Fannie Mae and Freddie Mac (so-called GSE reform) — the two institutions largely responsible for enabling the affordable 30-year mortgage in the first place — it’s worth taking a look at how monthly mortgage payments on the typical U.S. home would change if rates rose and/or other mortgage products became more popular.

We don’t know what impact GSE reform might have on the 30-year mortgage, and it’s possible any resulting dominant mortgage product would be wildly or only mildly different from what we have today. The figures below provide a glimpse at mortgage alternatives, and illustrate how sensitive monthly mortgage payments on the nation’s median-valued home might be to changes in interest rates and loan duration (use our comparison tool to see the differences across metro areas). All figures assume a 20 percent down payment.

30-Year Fixed-Rate Mortgage, at Current Rates

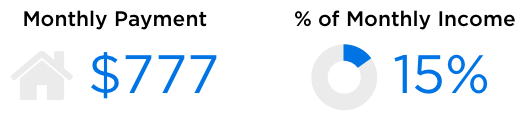

- The most common mortgage product today is the 30-year fixed rate mortgage. Last month, to buy the typical U.S. home with a 30-year fixed rate mortgage, the monthly payments would be $777, or 15 percent of the country’s median household income.

Adjustable-Rate Mortgage, at Current Rates

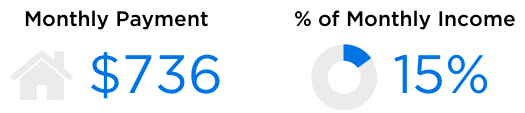

- If the terms of 30-year fixed-rate mortgages become less favorable after GSE reform, more buyers could choose adjustable-rate mortgages (ARMs). While ARMs often provide a better deal for the first few years of the loan, rates and payments eventually increase unless a borrower refinances. Last month, to buy the typical U.S. home with an adjustable rate mortgage, the first year’s monthly payment would be $736 or 15 percent of the country’s median household income. But those payments would rise when the adjustment takes place.

Non-Conforming Jumbo Loan, at Current Rates

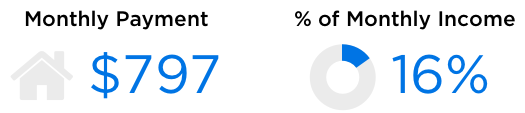

- Another possibility as a result of GSE reform is that interest rates could climb in response to the elimination of a government guarantee. We don’t know how much they might climb, but they could resemble rates on current loans that don’t have a government guarantee: non-conforming, jumbo loans (a relatively small market currently skewed toward the wealthy). So the exact terms of today’s jumbo loans may not scale to the larger housing market. Last month, to buy the typical U.S. home with a 30-year, fixed rate, non-conforming jumbo mortgage, the monthly payments would be $797 or 16 percent of the nation’s median household income.

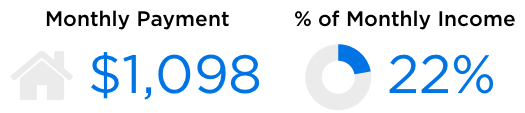

30-Year Fixed-Rate Mortgage, at 7 Percent Rate

- Interest rates overall are at historic lows, but reforms to Fannie and Freddie in tandem with other trends in the economy could raise mortgages rates across the board. If they reach 7 percent, a rate common 20 years ago, monthly payments could rise substantially. Last month, to buy the typical U.S. home with a 30-year fixed rate mortgage common in the late ‘90s, the monthly payments would be $1,098 or 22 percent of today’s national median household income.

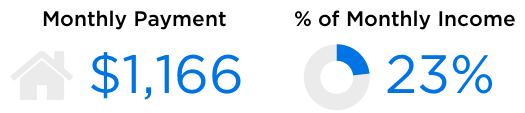

15-Year Fixed-Rate Mortgage, at Current Rates

- Even if rates remain similar to today, more buyers may shift toward shorter-term loans as a result of GSE reform and/or other economic shifts. While today’s 15-year, fixed-rate mortgages usually provide lower interest rates, the shorter time frame makes each payment larger. Last month, to buy the typical U.S. home with a 15-year fixed rate mortgage, the monthly payments would be $1,166 or 23 percent of the U.S. median household income.

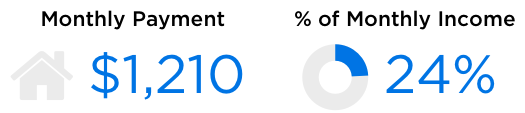

15-year Fixed-Rate, Non-conforming Jumbo Mortgage, at Current Rates

- Finally, it’s possible that rates rise and buyers move toward shorter-term loans. In that case, new loans could resemble 15-year, fixed-rate, non-conforming jumbo loans. Last month, to buy the typical U.S. home with a 15-year fixed rate non-conforming mortgage, the monthly payments would be $1,210 or 24 percent of the country’s median household income.