How Rising Rates Affect Mortgage Affordability

Climbing home prices are just one factor in the rising cost of home ownership. Another major contributor going forward is likely to be rising mortgage interest rates — something home buyers haven’t experienced on a wide scale in years.

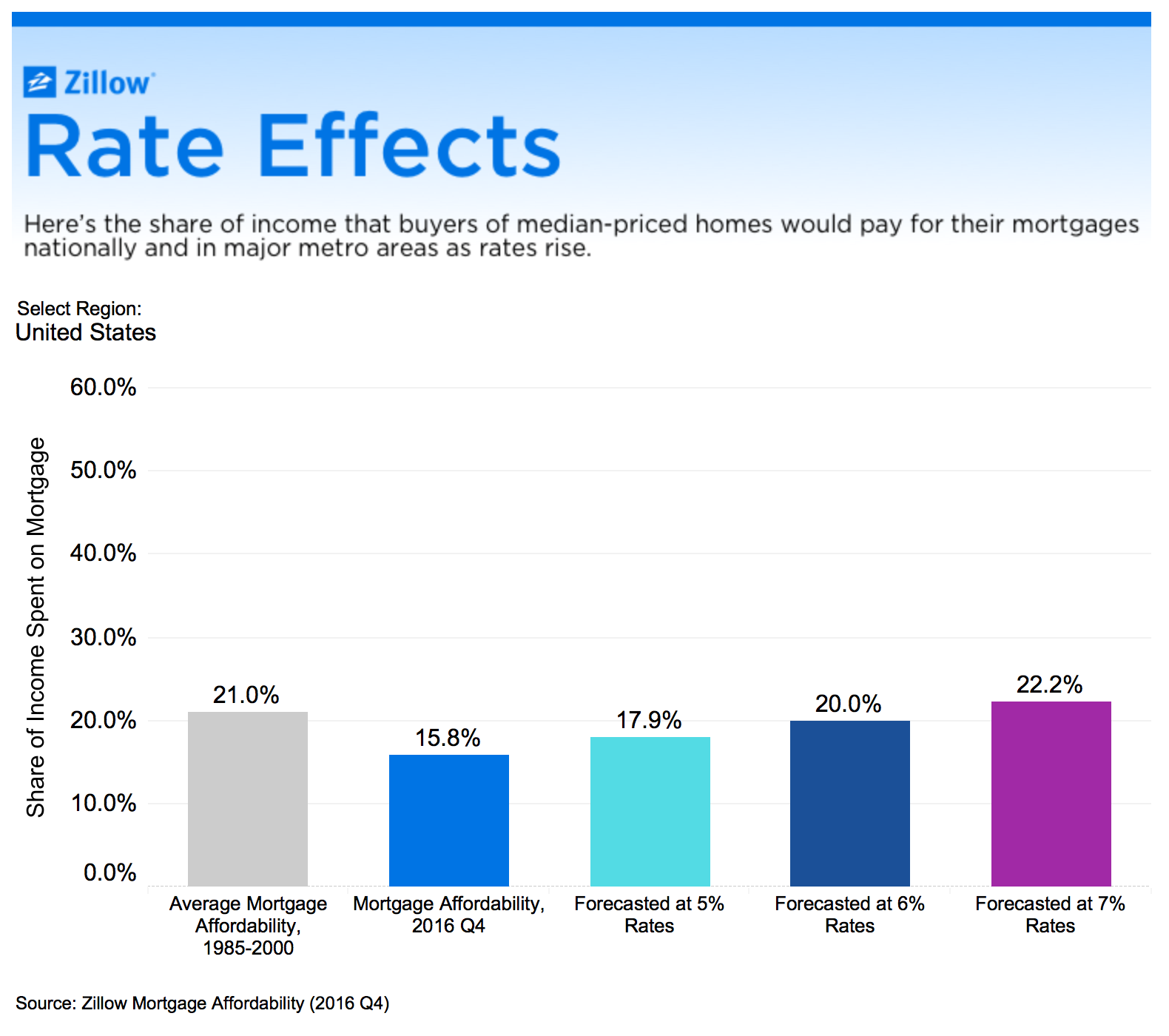

From 1985 through 2000, people with median incomes buying median-priced U.S. homes spent 21 percent of their incomes on the mortgages. That share has dropped. In the fourth quarter 2016, the typical buyer purchasing the typical home spent 15.8 percent of his income on the mortgage. That’s at interest rates around 4 percent — very low compared to historic norms.

If rates rise to 5 percent (which some estimates suggest could happen within the next year) and homes continue to gain value as expected, the share of income spent on a typical U.S. mortgage will jump to 17.9 percent. At 6 percent interest, the share becomes 20 percent. And at 7 percent interest, it becomes 22.2 percent.

In some local markets, the squeeze will be more acute. In Seattle, for example, if rates rise to 7 percent, the share of income that buyers of a median home would spend escalates from 24.7 percent to 35.2 percent.

See how rising rates could affect mortgage affordability in your metro area:

Rising mortgage interest rates pose affordability problems for all home buyers, but current homeowners looking to buy a new home are in a uniquely challenging situation: At higher rates, monthly payments on even a similarly-valued home will go up, to say nothing of a more expensive home.

This means homeowners who have a mortgage locked in at today’s very low rates may be reluctant or unable to give up that less-expensive mortgage and take on a new one at a higher rate when it comes time to buy a new home. This phenomenon is known as “mortgage rate lock-in” and could lead to diminished demand from home buyers and/or reduced inventory of homes for sale as would-be buyers instead choose to stay put in their current homes.

For several decades, as rates have fallen consistently, this hasn’t been a problem. In 2017 and beyond, it could become one.

Related: