Mortgage Rates Retreat from 2008 Highs on Tariff, Tillerson News

Weak inflation and ongoing geopolitical uncertainty – headlined by potentially stiff tariffs on aluminum and steel and the ouster of U.S. Secretary of State Rex Tillerson – helped push mortgage interest rates down this week after a roughly week-long rise.

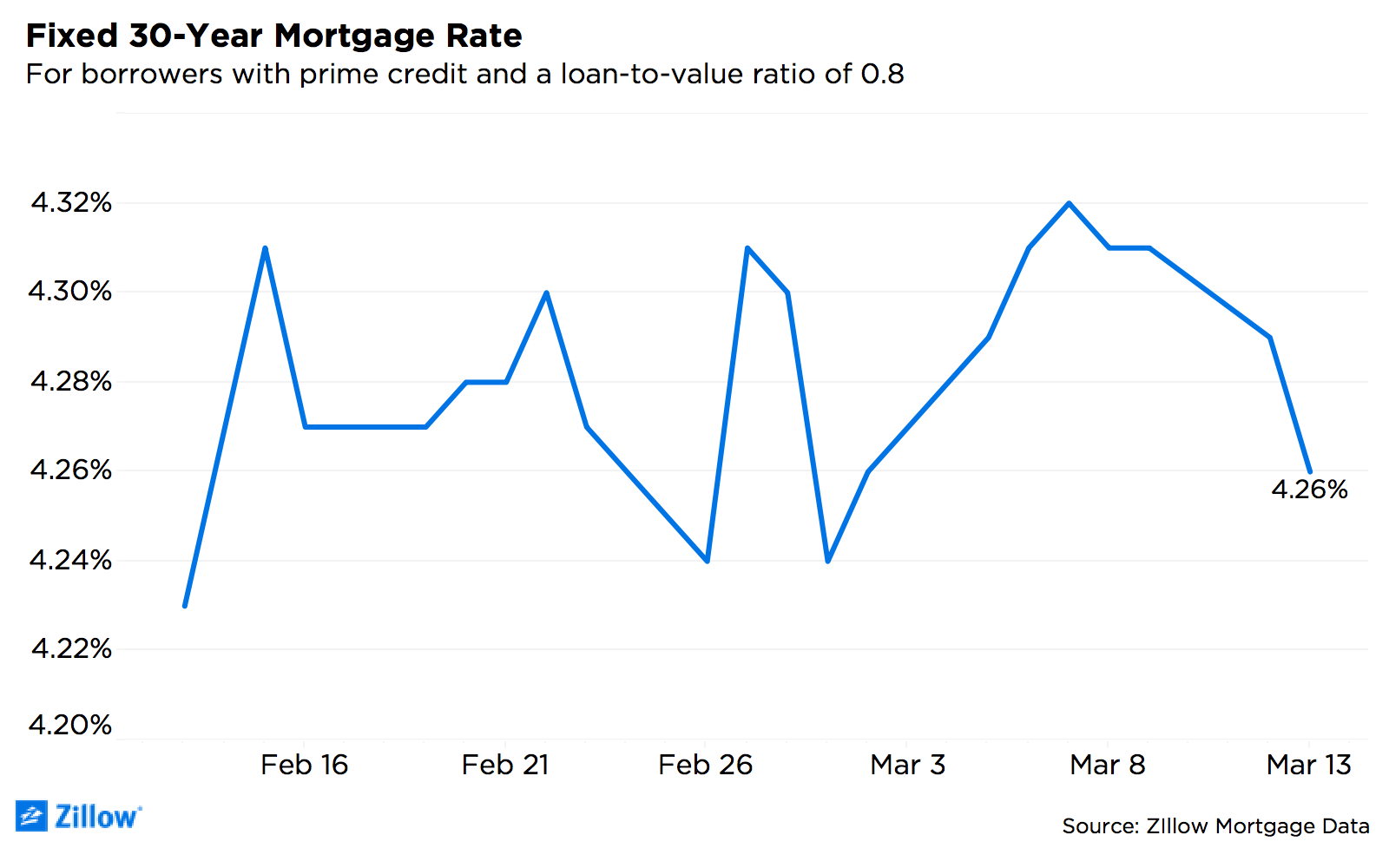

Mortgage rates marched steadily upward through the first part of last week, touching a 2018 high of 4.32 percent, before dipping slightly on Thursday and Friday – even in the face of an exceptionally strong jobs report that may have otherwise been expected to push rates higher. Last week’s dip was likely a reaction to announced plans to enact stiff and widespread tariffs on imported aluminum and steel, which set off market fears that those policies could set off a broader international trade dispute that might disrupt the national economy.

Weak inflation data released early Tuesday softened expectations for the path of interest rates ahead, and pushed rates lower. Additionally, the firing of U.S. Secretary of State Rex Tillerson early this week was yet one more unsettling geopolitical headline, prompting jittery investors to seek safe assets and helping push rates lower still.

Geopolitical uncertainty is becoming somewhat of a fixture at the top of investors’ minds, and is likely to continue to influence investor behavior, and therefore interest rates, for the foreseeable future. Looking more near-term, the Fed is widely expected to raise short-term interest rates at next week’s Federal Open Market Committee (FOMC) meeting, which may push rates somewhat higher – though markets have already priced in this anticipated hike.

Notably, next week is also the first time newly installed Fed Chair Jerome Powell will take questions from the press since taking over from Janet Yellen in mid-February. Markets will watch his comments carefully and rates may rise or fall somewhat in reaction to the first public indications of Powell’s thinking and vision for future policy. The FOMC will also release its next quarterly forecast, which may move rates if economic projections and the expected schedule of future rate hikes deviates widely from past statements.