October Market Reports: Home Value Growth Accelerates, While Rent Growth Slows

- Rents appreciated 4.5 percent year-over-year, down from 5.3 percent in September 2015.

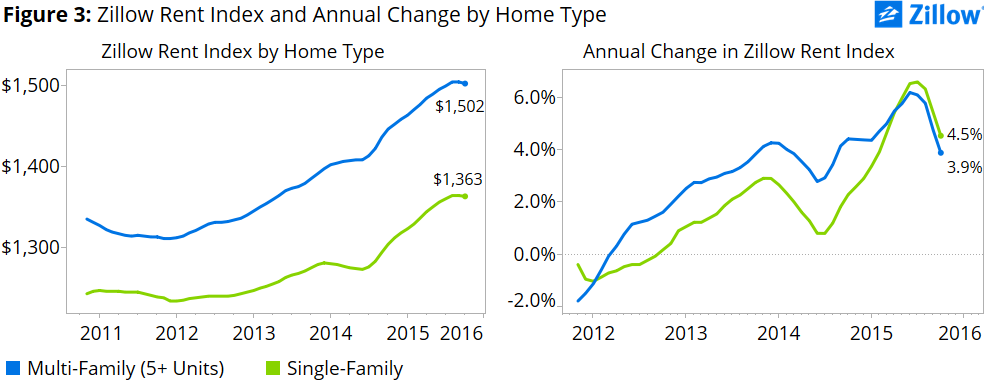

- Rents in large multifamily buildings rose 3.9 percent annually, rents of single-family homes grew 4.5 percent.

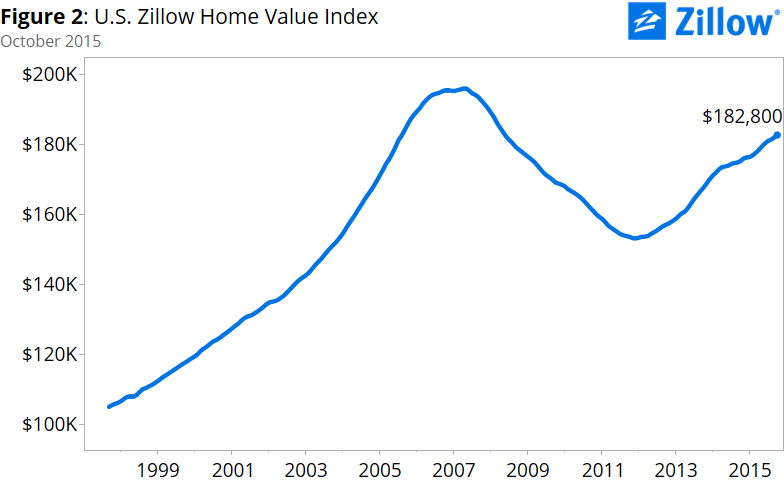

- Home values grew 4.3 percent year over year to a Zillow Home Value Index of $182,800 in October.

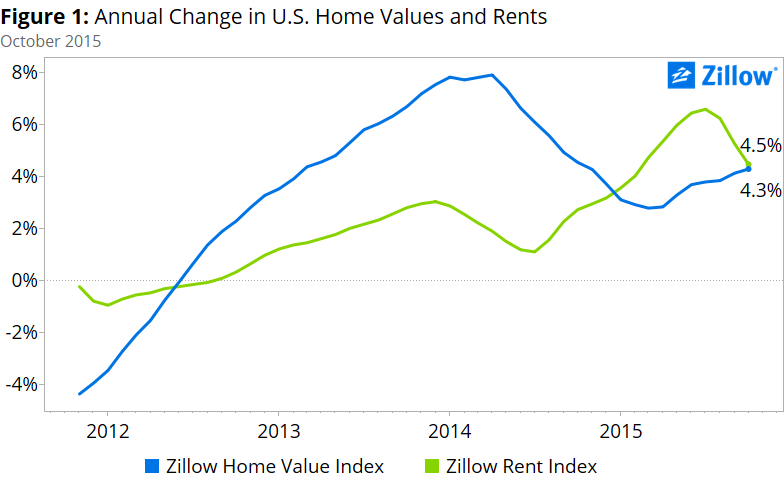

As the U.S. housing market enters the fourth quarter of 2015, the dominant trends from the first quarter have reversed. Annual home value appreciation, previously slowing down, has accelerated; while growth in rents, previously accelerating, has begun to slow down.

In each of the first three months of 2015, annual home value growth was slower than the month prior. U.S. median home values grew 3.1 percent year-over-year in January (down from 3.7 percent in December 2014), 2.9 percent in February and 2.8 percent in March. The annual pace of rental appreciation over the same period was consistently speeding up. Median U.S. rents grew 3.6 percent year-over-year in January (up from 3.2 percent in December 2014), rising to 4 percent in February and 4.7 percent in March.

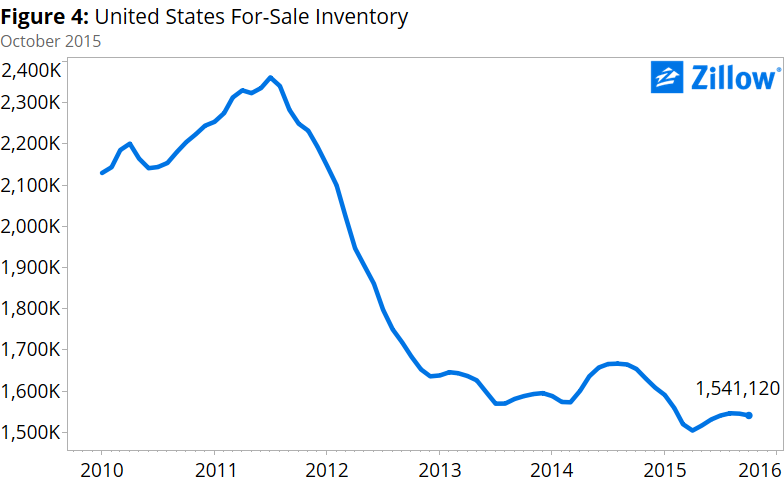

The main reason for the reversal likely hinges on the supply of homes for sale and rent. After years under construction, more rental units are beginning to come online in many cities nationwide, helping to ease rental appreciation in some areas. At the same time, the number of homes available for sale nationwide has fallen in each of the past two months, keeping some upward pressure on home values.

Still, rents continue to grow at a rapid clip, and are growing faster annually than home values overall: 4.5 percent year-over-year growth for rents, compared to 4.3 percent year-over-year growth for home values.

As rents have grown and rental affordability continues to suffer, the stability and relative affordability of homeownership may be pushing some qualified renters to make the jump to homeownership. A widely expected December rate hike from the Federal Reserve could be an additional incentive for buyers to enter the market while mortgage interest rates remain low. Reflecting this, home values are growing at their fastest pace since November 2014.

The Pace of Home Value Appreciation is Picking Up

Among the 35 largest metro areas in the country, 24 experienced annual home value growth that was faster than the nation’s 4.3 percent yearly pace of appreciation. Home values grew by more than 10 percent per year in six of those large metro markets: Denver (16.2 percent), Dallas (15.2 percent), San Jose (13.3 percent), San Francisco (12.2 percent), Portland (11.4 percent) and Miami (10.3 percent). Two large metros, Washington, D.C. (-0.4 percent) and Baltimore (-1.2 percent), experienced annual declines in home values.

Single-Family Rents Rising Faster than Multi-Family Rents

Nationwide, rents of single-family, condo, co-op and apartment homes grew 4.5 percent year-over-year in October, to a U.S. Zillow Rent Index of $1,382, down from 5.3 percent annual appreciation in September. As recently as July, overall rents were growing 6.6 percent year-over-year. Though rents continue to rise fairly quickly, we’re beginning to see signs of a slowdown in the national rental market.

Perhaps owing to their rising popularity as a rental option for young families and those displaced by foreclosure in recent years, rents for single-family homes are growing more quickly than rents for more traditional apartments in larger multifamily buildings. Single-family home rents grew 4.5 percent year-over-year in October, while rents for apartments in multifamily properties grew just 3.9 percent over the same period (figure 3). A limited supply of single-family homes for rent compared to more traditional apartments could also be a factor in their more rapid rental appreciation, especially given weak construction activity for new single-family homes in general.

Fewer Homes For-Sale

Of the nation’s largest 35 metro markets, Atlanta, Austin and Washington, D.C., experienced the biggest increases in inventory over the past year. The Charlotte, San Diego and Seattle metros all experienced decreases in for-sale inventory of 25 percent or more.

Outlook

Over the next year, the pace of home value growth is expected to slow, growing 2.6 percent from October 2015 to October 2016, according to the Zillow Home Value Forecast. Over the past year, home values grew 4.3 percent. Of the largest metro areas covered by Zillow, Las Vegas, Dallas, Seattle and Sacramento, Denver, Riverside and Portland are expected to have home values grow by 5 percent or greater over the next year. No metro areas are expected to have home values fall, although appreciation for Baltimore is expected to be flat.

Rental appreciation has started to slow down in part due to more rental supply. Many of the bigger multifamily rental projects that were begun a couple years ago in cities nationwide are finally starting to open for occupancy, easing pressure on rents somewhat. But make no mistake: Despite this recent slowdown in rental appreciation, the rental affordability crisis we’ve been enduring for the past few years shows no signs of easing, especially as income growth remains weak. It will take a lot more supply, and a lot more renters-turned-homeowners, to fully reverse this trend.