During The Pandemic, Relatively Fewer Land-Use Restrictions In Some Markets Created Pockets of Housing Affordability

- During the pandemic, new single-family construction surpassed the 1-million-unit threshold for the first time since 2007.

- As mortgage rates doubled, markets with fewer land-use restrictions saw relatively more building activity, and became pockets of housing affordability.

- Conversely, regions with the most restrictive land-use regulations — Los Angeles, San Diego, San Jose, Sacramento, and Riverside — now have the smallest share of affordable listings on Zillow.

The pandemic triggered a one-two punch of fast-rising home prices and a doubling of mortgage rates that severely impacted the affordability of buying a home. Demand that far exceeded supply also left a major shortfall in housing inventory.

But areas where builders have been able and encouraged to keep up with that surge in demand have witnessed better affordability outcomes. The injection of more options in both the rent and for-sale markets have helped cool rampant growth and have supported a recovery in existing inventory.

What happened to the economy?

The pandemic disrupted supply chains while putting millions of people out of work. The sharp economic contraction and deep uncertainty disrupted financial markets.

In response, policymakers implemented aggressive economic measures, including direct income support and unprecedented monetary stimulus. The Federal Reserve purchased Treasury and mortgage-backed securities to lower interest rates and stabilize the economy.

With spending curtailed by stay-at-home policies, households accumulated excess savings. Simultaneously, virus fears, pandemic restrictions, and the rise of remote work increased demand for lower-density areas.

How did that impact housing?

This combination of higher savings, lower mortgage rates, and a growing need for space drove housing demand to new heights. In 2021, home sales reached their highest level since 2006. Mortgage application data revealed a significant shift from high-density to low-density, and from multifamily to single-family neighborhoods.

By July 2021, home values had surged 19% year over year — the fastest 12-month increase on record, according to Zillow data. Austin saw the most explosive growth by far, with annual home value appreciation reaching up to 41% by mid-2021.

Market rents also began rising, foreshadowing future increases in government rent inflation measures. Miami saw rents rise the fastest, notching 30% annual growth in the spring of 2022.

Fueled by record home equity gains and stock market growth, demand soared across various sectors of the economy. But as inflation took hold, interest rates climbed. The 30-year fixed mortgage rate jumped from 2.7% in late 2020 to 7.1% by October 2022.

How the homebuilding industry responded

When demand rises, supply typically follows, though with a lag. In 2021, total housing starts reached 1.6 million units, with single-family starts exceeding 1 million for the first time since 2007, according to the U.S. Census Bureau.

Historically, housing markets with fewer building restrictions have been more responsive to rising demand, and the same pattern emerged during the pandemic.

The metro areas with the highest single-family permitting activity from January 2020 to November 2024 were:

| Metro Area | Single-family permits (Jan 2020—November 2024) | Home value change (Jan 2020—November 2024) |

| Houston, TX | 245,425 | 38% |

| Dallas, TX | 217,456 | 45% |

| Phoenix, AZ | 145,790 | 55% |

| Atlanta, GA | 133,666 | 57% |

| Austin, TX | 97,962 | 41% |

| Charlotte, NC | 92,214 | 60% |

| Orlando, FL | 80,113 | 54% |

| Tampa, FL | 76,729 | 61% |

| Nashville, TN | 73,964 | 50% |

| Jacksonville, FL | 68,308 | 52% |

Many of these areas have seen some of the nation’s largest price corrections from pandemic peaks — high-flying markets that have since come back down to earth include Austin, Phoenix and Dallas.

In contrast, the metros with the least single-family construction included Milwaukee, San Jose, Pittsburgh, New Orleans, San Diego, Birmingham, San Francisco, Memphis, Louisville, and Baltimore.

Despite an increase in construction, the industry was not immune to economic disruptions. Supply chain bottlenecks and labor shortages pushed construction costs higher. By December 2021, material costs had risen 35.1% year over year, while labor shortages drove construction wages up 6% in 2022.

Though 2021 saw the highest number of housing starts, the bulk of single-family completions did not reach the market until 2022 — after mortgage rates had more than doubled. Multifamily completions peaked even later, in 2024.

Affordability Challenges and Market Adjustments

Higher inflation and rising interest rates sent housing affordability to historic lows, prompting builders to adjust. Many new homes that began construction before rates surged were completed just as residential mobility slowed. To attract buyers, builders introduced incentives such as mortgage rate buy-downs.

At the same time, homeowners locked into ultra-low mortgage rates hesitated to sell, reducing the supply of existing homes. New listings from owners hit bottom at 35% below pre-pandemic averages in April of 2023. As homebuyers substituted existing homes with more readily available newly built homes, a more severe decline in homebuilding activity was averted.

To address affordability concerns, builders increasingly pivoted toward higher-density housing, constructing more townhomes and condos instead of detached single-family homes. Building on smaller lots and incorporating attached housing allowed them to keep prices within reach while mitigating rising land and material costs.

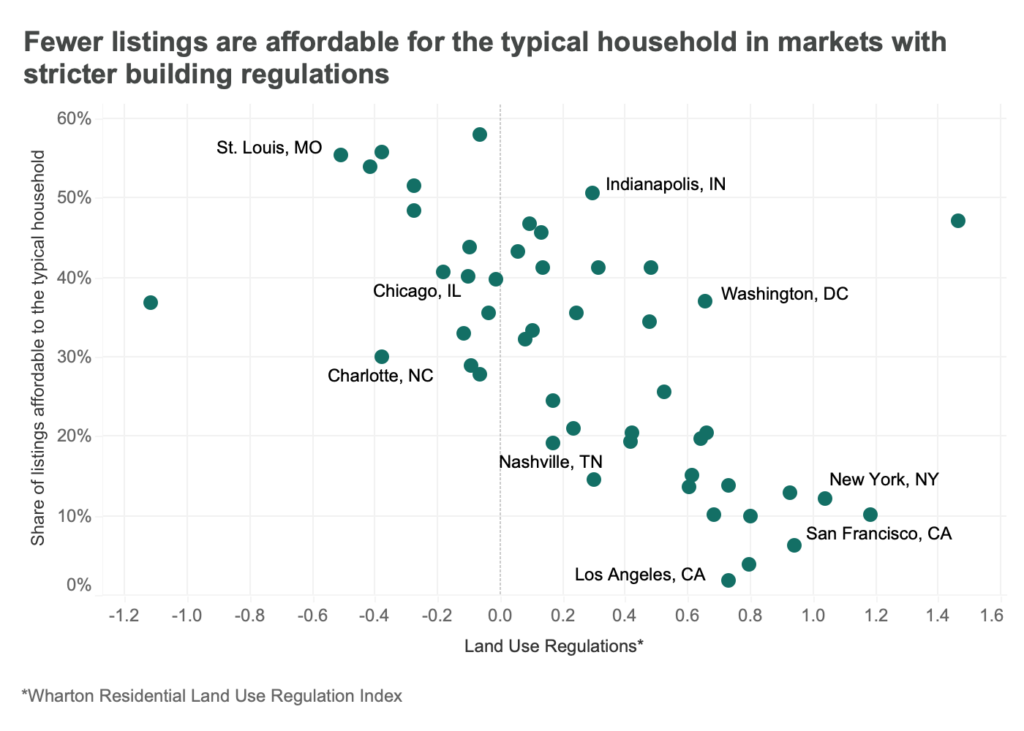

The Impact of Land-Use Regulations on Affordability

It was true before the pandemic, and it’s still true now. Housing remains least affordable in markets with the strictest zoning and planning restrictions. A higher ranking on the Wharton Residential Land Use Regulation Index (meaning more strictly regulated) is negatively correlated with the share of listings on Zillow that are affordable for a household making the median income.

Builders can only build what they are allowed to. How responsive builders are to a price increase depends on the availability of labor and materials, as well as buildable land, which often depends on geographic constraints and regulations such as zoning and planning restrictions that determine what builders can build where.

Addressing the 4.5-million-home deficit in the U.S. requires reforms to allow greater density. Zillow survey data indicates that most residents support such changes in their own neighborhoods to boost supply.

Policymakers should consider:

- Zoning reforms to permit more middle housing, multifamily and high-density housing.

- Reducing parking requirements to lower development costs.

- Streamlining permit approvals to minimize delays.

- Expanding affordable housing trust funds to support new development.

By easing restrictions and increasing supply, cities can create more housing opportunities and improve affordability for millions of Americans. The ‘Build The Middle playbook’ provides a roadmap to remove barriers to more affordable middle housing.