Q1 2017 Negative Equity: Slow Progress Beats No Progress

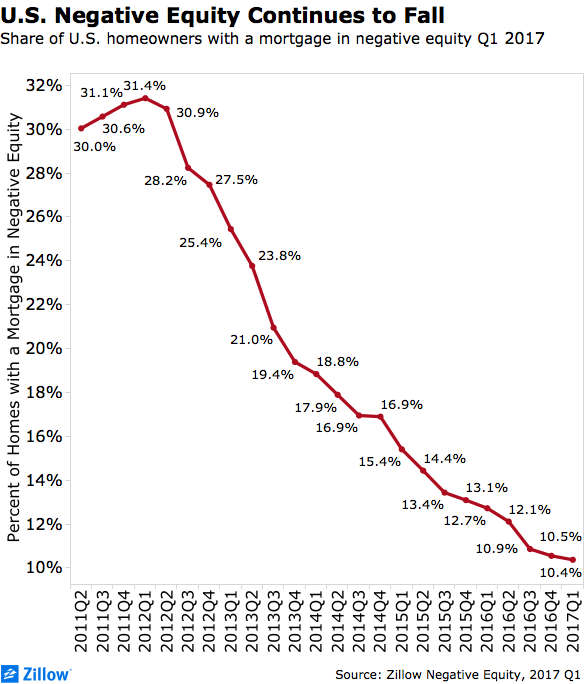

- The U.S. Q1 2017 negative equity rate – the share of all homeowners with a mortgage that are underwater, owing more on their home than it is worth – fell to 10.4 percent.

- Nationwide, slightly more than 5 million homeowners with a mortgage are in negative equity, down from a high of more 15.7 million in early 2012.

- A majority of those homeowners remaining in negative equity are underwater by 20 percent or more.

The U.S. negative equity rate – the share of all homeowners with a mortgage that are underwater, owing more on their home than it is worth – fell to 10.4 percent in the first quarter of 2017, the 20th straight quarterly decline. But the speed at which negative equity is falling has slowed dramatically.

The 0.1 percentage-point quarterly drop between Q4 2016 and Q1 2017 negative equity was the smallest since a barely noticeable drop from Q3 2014 to Q4 2014. The Q1 2016-Q1 2017 annual change of 2.3 percentage points is the smallest on record (data dates to Q2 2011), tied with the annual drop recorded in Q3 2012 and again in Q2 2016. The annual change, spread over four quarters, is smaller than the one-quarter change recorded between both Q2-Q3 2012 and Q2-Q3 2013.

One reason for the slowdown is because the bulk of those homeowners that remain in negative equity are very deep underwater – 56.7 percent of those in negative equity were underwater by more than 20 percent as of the end of Q1. In addition to simply paying off your loan over time, the surest way to get out of negative equity is to wait for a home’s value to appreciate enough to bring it into positive equity. Home values grew at a robust annual pace of more than 7 percent in Q1, well above historically “normal” annual home value growth of 3 percent to 5 percent. Even so, it would take several years of growth at that rate to free a homeowner underwater by 20 percent – to say nothing of the roughly 15.1 percent of underwater homeowners who owe twice or more what their home is worth.

Essentially, those “easy” homeowners in relatively shallow negative equity have likely already or will soon re-surface as home values have grown over the past few years. That leaves just those millions of harder cases remaining that are likely to take much longer to free.

Among the 35 largest metro markets covered by Zillow, the negative equity rate as of the end of Q1 was highest in Chicago (16.4 percent), Virginia Beach (16.1 percent) and Las Vegas (15.9 percent). Negative equity was lowest in San Jose (2.8 percent), San Francisco (3.6 percent) and Portland (4.2 percent). Of the 10 large markets with the lowest rates of negative equity, seven are on the West Coast.

Finally, even if a homeowner isn’t technically underwater but doesn’t have much equity, they can still have a lot of difficulty selling their home and using the proceeds to comfortably afford the costs of buying a new one, including a down payment, taxes and real estate commissions. Including those U.S. homeowners with a mortgage with 20 percent or less equity in their home, almost a quarter (24.3 percent) of homeowners with a mortgage are in so-called “effective” negative equity.

Among the nation’s 35 largest metro markets, the highest effective negative equity rates are in Virginia Beach (41.5 percent), Las Vegas (34.8 percent) and Baltimore (32.7 percent). The lowest rates of effective negative equity among large metros as of the end of 2016 were in San Jose (6.3 percent), San Francisco (8.3 percent) and Portland (10.9 percent).

Related:

- Equity Inequality: The Differing Impact of the Boom and Bust on Millennial, Gen X and Older Homeowners

- Homes in Black Neighborhoods Twice as Likely to be Underwater as Homes in White Neighborhoods

- Blue and Red Home Values