Rate-Locked Homeowners Nearly Twice as Likely to Not Consider Selling

After hitting record lows at the end of 2020, mortgage rates have dramatically risen over the last couple years, now hovering around 6-7% compared to the sub-3% rates seen in 2020 and 2021. For homeowners with low mortgage rates, these increases imply an additional financial cost to moving to a new home — even one at the same price point. This increased cost of transaction can often keep them “locked-in” to their current home in what is known as a rate lock as homeowners wait for better rates (oftentimes, resulting in a hold up of housing supply). Moving and selling would mean prepayment of the current mortgage and remortgaging a new home at significantly higher rates, resulting in stronger incentives to hold off on selling their home.

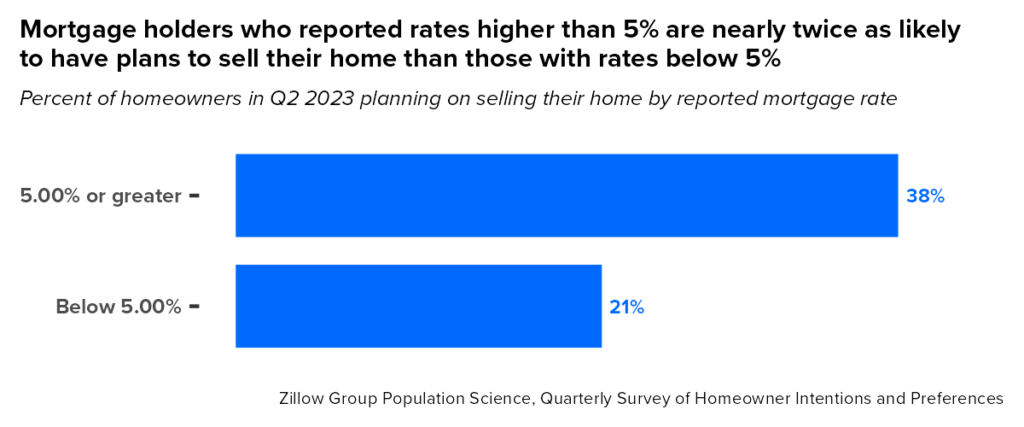

Homeowners who report mortgage rates below 5% are nearly twice as likely to want to hang onto their current home.

Mortgage holders who, as of June 2023, said they had rates higher than 5% are nearly twice as likely to have plans to sell their home in the next three years than those with lower rates. These homeowners face no or relatively little financial disincentive to trading their current mortgage for a new one. In fact, of homeowners who reported plans to sell, 47% of homeowners paying a mortgage above 5% already have their house listed “for sale” compared to 20% of those with rates below. On the flip side, homeowners already paying a lower interest rate may be reluctant to move and refinance at a higher rate.

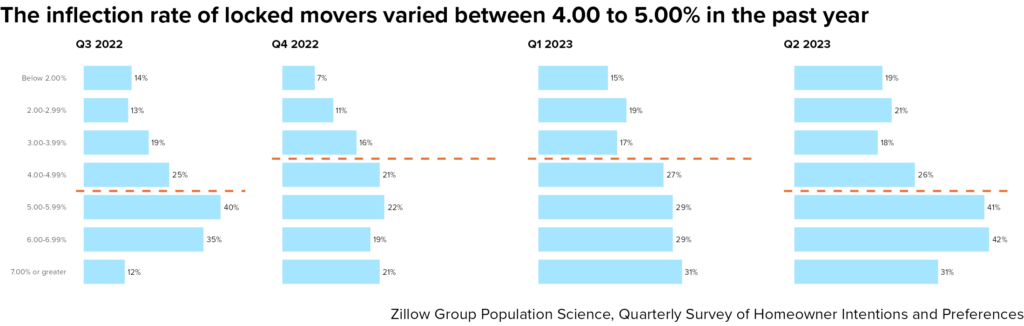

The split between those reporting a 4.00-4.99% and 5.00-5.99% rate reveals the greatest divide in homeowner intent to move: 41% of homeowners at 5.00-5.99% consider selling, while only 26% of those at 4.00-4.99% say the same. That said, while the most striking divergence for locked movers in June 2023 was at a 5.00% mortgage rate, it has varied between 4.00 to 5.00% in the past four quarters (i.e., 5.00% for September 2022, 4.00% for December 2022, and 4.00% for March 2023). This oscillation could indicate that the true inflection point – the rate at which homeowners are less likely to move – is generally between 4.00 and 5.00%.

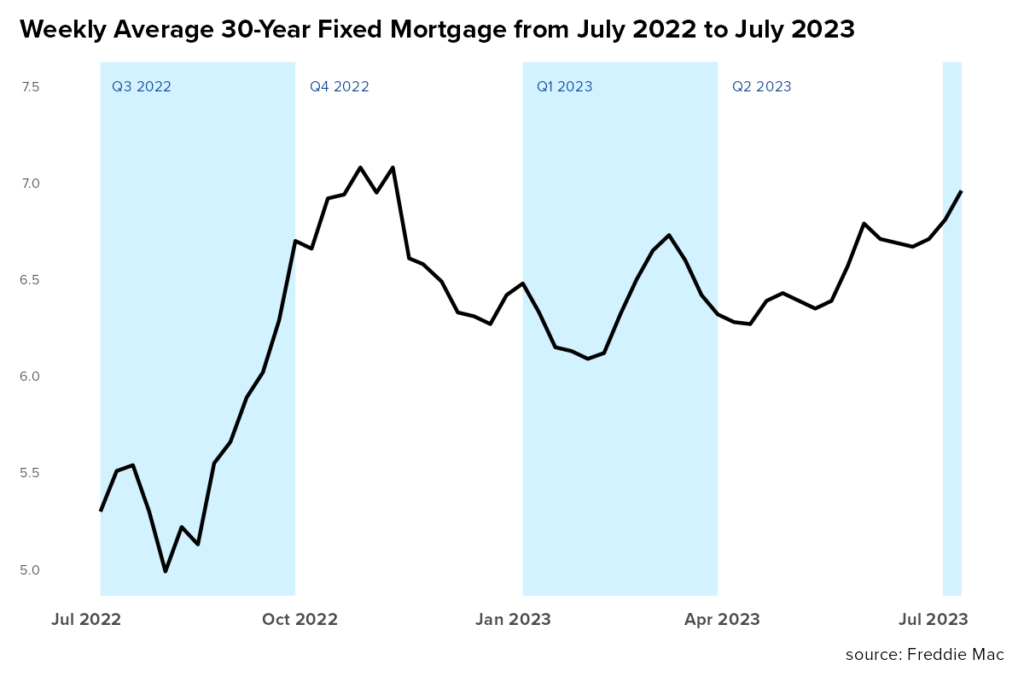

However, there is suggestive evidence that homeowners may be considering trends in the market rate when making their decision whether to sell and move. When tracked against Freddie Mac’s weekly average 30-year fixed mortgage, there is preliminary evidence that the purchase rate at which homeowners are less likely to move is higher (i.e. 5.00%) when mortgage rates are increasing, as seen in September 2022 and September 2023, and lower (i.e. 4.00%) when mortgage rates are generally decreasing or plateaued. The Zillow Group Population Science team will continue to track this inflection point in upcoming surveys to determine whether the pattern continues to hold.

Most of today’s mortgage holders would need to remortgage their new home at a higher rate than their current one.

According to our survey, around 90% of mortgage holders reported having a rate less than 6.00%, about 80% of mortgage holders reported having a rate less than 5.00%, and almost a third reported a rate less than 3.00%.

What does this mean? As mortgage rates hover just shy of 7.00% in the past month, most of today’s mortgage holders would be forced to finance any new home at a higher rate than their current one, an incentive to hold on to their home rather than move soon. A recent study by two finance professors, Julia Fonseca and Lu Liu, found that mortgage lock can happen even without increasing market rates. In general, moving is costly. Even if the market rate is equal to or even slightly below the mortgage rate at purchase, homeowners have to weigh whether the benefit of financing a new home at a similar or lower rate is worth the other costs of moving.

Of course, a homeowner’s decision to sell and move is influenced by more than just mortgage rates. We found that less than half (42%) of all homeowners considering selling said that recent changes in mortgage rates were a reason they decided to move. However, when disaggregated between those with rates above 5.00% and those below, unsurprisingly, homeowners with higher mortgages were more likely to report rates as one of their reasons to sell. 65% of higher-rate homeowners reported rates as an influencing factor compared to 35% of lower-rate homeowners. Rather than solely looking at interest rates, homeowners might take into account their monthly payment amount and non-financial incentives that might be worth the cost, e.g. family-motivated reasons, new jobs or school.

Still, interest rates are impacting moving rates. In the study mentioned above, Fonseca and Liu also found that a one percentage point increase in the difference between a homeowner’s mortgage rate and the current market rate reduces moving rates by 9%. In today’s market where interest rates continue to rise, the difference between existing homeowners’ rates and the market rate continues to grow, resulting in more “locked-in” households.

Locked mortgages impact housing supply.

Even though this locked mortgage effect may not be a direct experience for first-time homebuyers, current homeowners’ reluctance to sell does have a direct impact on the housing supply. When homeowners with low mortgage rates are hesitant to sell their homes, it results in a shortage of housing options, resale supply, homeowner mobility, and places upward pressure on housing prices.

Methodology

These analyses use data from the ZG Population Science Quarterly Survey of Homeowner Intentions and Preferences using a repeated cross-sectional design. Homeowners 18 years of age and older who did not move within the last 12 months were eligible for participation. Data are weighted to ensure representativeness of this homeowner population. The Q2 2023 survey was fielded during the first two weeks of June 2023 and included 1,815 homeowner respondents.