Graduating into a recession hurts (for about six years)

- Graduating into a recession has an immediate and lasting effect on young adults’ homeownership rate.

- Five years after completing their degree, young adults who graduate into a recession still have a lower homeownership rate than peers graduating into normal economic times. But at six years this gap disappears.

- As the sixth anniversary of the end of the most recent recession approaches, it is likely that a growing number of young adults who graduated college in 2008 and 2009 into the worst economic crisis in a generation will be looking to buy homes.

In markets, as in life, good timing can make a world of difference. For the unlucky generation of young adults who graduated college in 2008 and 2009, bad timing has left indelible scars – scars that remain visible today as this group begins to enter their prime home-buying years.

Research shows that graduating into a recession has a lasting adverse effect on young adults’ employment and earning, a phenomenon known as labor market “scarring.”[1] Homeownership is closely tied to the labor market, particularly among young adults, and some preliminary evidence suggests that a similar “scarring” effect occurs with respect to the homeownership rate among young adults who graduate into a weak economy.

Two years after graduation, the homeownership rate among young adults who graduate college into a recession is about 22 percent below their peers who graduated during better economic times. The good news is, this gap gradually narrows and essentially disappears about six years after graduation.

Analysis

Using data from the U.S. Census Bureau’s March Current Population Survey (CPS), Zillow analyzed the homeownership rate for successive groups of college graduates each year after graduation from 1976 through 2013.[2]

The homeownership rate tends to increase fairly rapidly during the first few years after college, as young adults find stable employment, begin to earn regular incomes and gradually settle down.[3] For most, growth in the homeownership rate begins to slow about 10 years after graduation and essentially levels off about 15 years after graduation.

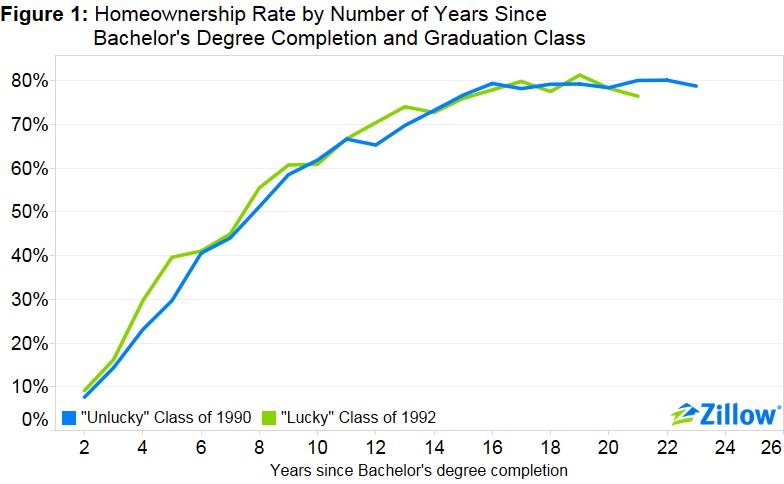

Consider the different experiences of the “unlucky” undergraduate class of 1990, and the “lucky” class of 1992. Between July 1990 and March 1991, the United States entered a relatively brief and mild recession characterized by weak employment recovery. In the years after graduation, the homeownership rate among members of the class of 1992 was higher and initially increased more quickly compared to homeownership among their classmates that graduated two years earlier (Figure 1). It took about six years after graduation before the homeownership rates converged and began to move roughly in tandem.

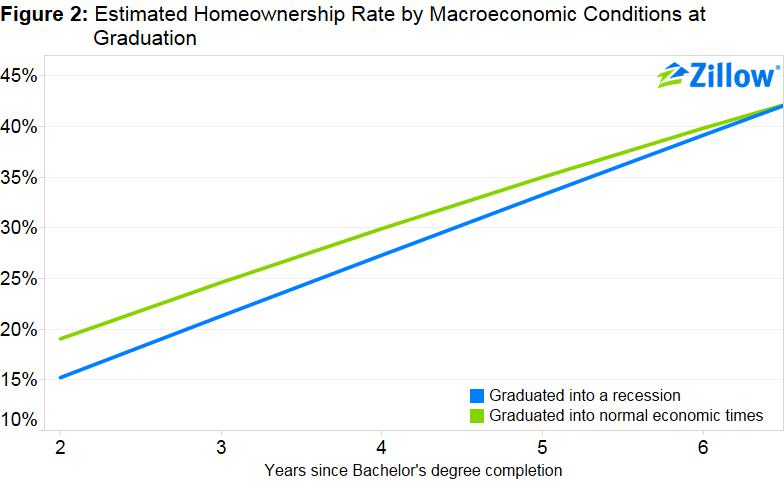

The results suggest that two years after graduation, the homeownership rate among young adults graduating into a recession is about 22 percent below their peers who graduated during better economic times (Figure 2). This gap gradually narrows, however, and essentially disappears about six years after college graduation.

Conclusion

Movements in the homeownership rate are complicated and the model presented above is just one lens to examine its dynamics. As discussed in previous research, the homeownership rate among young adults has drifted downward over time because of shifting marriage and labor force participation trends. Graduating into a recession might prompt young adults to delay getting a job in favor of staying in school, depressing their homeownership rate in the near term but potentially increasing it in the long term. Or, more may be forced to rent longer as lower wages and higher student debt make saving for a down payment on a home more difficult. And after witnessing the effects of the foreclosure crisis, some may decide the costs of homeownership may outweigh the benefits. Our model does not account for these possibilities.

But our admittedly simplistic findings suggest that young adults graduating college into a recession continue to experience adverse effects even after the economy recovers. While they eventually do catch up with their peers who graduate into more normal economic times, it typically takes six to seven years. As the sixth anniversary of the end of the most recent recession approaches (June 2015 will mark six years since the end of the recession that ran from December 2007 to June 2009) it is likely that a growing number of young adults who graduated into the worst economic crisis in a generation will increasingly be looking to buy homes.

Methodology

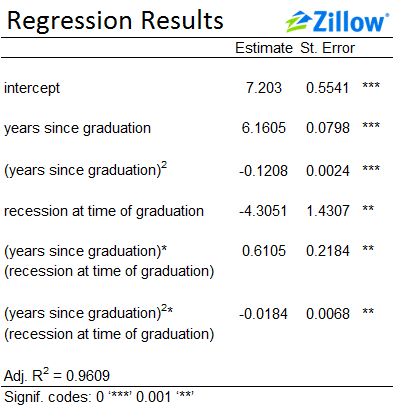

We model the homeownership rate as a function of a linear and a quadratic time trend which allows the homeownership rate to increase as time since college graduation increases, but at a decelerating rate. To capture the effects of graduating into a recession, we interact each of these time trends with an indicator variable that takes the value of one (1) if a recession was ongoing during the second or third quarter of the year of graduation. Official recession dates are from the National Bureau of Economic Research’s Business Cycle Dating Committee.

Homeowners exclude individuals who reside with a parent, relative, or housemate who owns the residence. The Current Population Survey (CPS) does not directly ask respondents their year of college graduation so we must assume that young adults complete their Bachelor’s degrees at age 23 and calculate the year of college graduation and number of years since college graduation using the survey year and age variables. Since the March CPS is conducted between mid-February and mid-April of the survey year, and most college graduations occur in May and June, we begin measuring homeownership rates two years after college graduation.

The regression results (see table below) have the expected signs and are strongly significant.

[1] See for example Philip Oreopoulos, Till von Wachter, and Andrew Heisz, The Short- and Long-Term Career Effects of Graduating into a Recession: Hysteresis and Heterogeneity in the Market for College Graduates, Institute for the Study of Labor (IZA) Discussion Paper No. 3578, June 2008 and Hani Mansour, The Career Effects of Graduating from College in a Bad Economy: The Role of Workers’ Ability, University of Colorado Denver, November 2009.

[2] Zillow analysis of data from the U.S. Census Bureau’s March Current Population Survey (CPS) made available by Miriam King, Steven Ruggles, J. Trent Alexander, Sarah Flood, Katie Genadek, Matthew B. Schroeder, Brandon Trampe, and Rebecca Vick, Integrated Public Use Microdata Series, Current Population Survey: Version 3.0 [Machine-readable database], Minneapolis: University of Minnesota, 2014.

[3] Homeowners exclude individuals who reside with a parent, relative, or housemate who owns the residence. The Current Population Survey (CPS) does not directly ask respondents their year of college graduation so we must assume that young adults complete their Bachelor’s degrees at age 23 and calculate the year of college graduation and number of years since college graduation using the survey year and age variables. Since the March CPS is conducted between mid-February and mid-April of the survey year, and most college graduations occur in May and June, we begin measuring homeownership rates two years after college graduation.