Renters: Results from the Zillow Consumer Housing Trends Report 2022

Executive Summary

More than two years into a global pandemic, the housing market continues to witness unprecedented shifts: recent weeks and months have seen skyrocketing interest rates, a softening buyers’ market, and climbing rents. While many of these changes are reshaping the homebuying process and renters’ plans and preferences, many renters’ behaviors, intentions, and preferences have remained relatively stable over the last year. Amid the flurry of external change, much of the rental market remains following the pandemic-catalyzed new ‘normal.’

The 2022 Consumer Housing Trends Report (CHTR) provides a snapshot of what housing consumers are thinking and doing in early-to-mid 2022. In this report, we take a deeper look at renters For the first time in recent years, CHTR includes both renters who have moved in the last year (the historical focus of the report), as well as tenured renters who have lived in their homes longer. In other CHTR 2022 reports, we examine homeowners, buyers, and sellers more closely. Information about who renters are in 2022 equips business teams with information they need to make informed decisions in this transformed housing market landscape.

Who are renters?

The typical US renter is 39 years old. Compared with the adult population as a whole, renters generally tend to be younger, less likely to identify as white, more likely to have never been married, and, and more likely to identify as LGBTQ+. These trends are especially true for recent renters. Demographic change tends to play out over a long time: Most of these characteristics have not changed substantially, if at all, over the last few years.

As we will detail throughout the report, there are several notable differences by renter tenure. For example, for renters who moved in the last year (recent renters), the median age is 31 years old. Renters who have lived in their current home for at least a year are typically older: their median age is 42 years old.

What do their homes look like?

Most renters (55%) live in an apartment building. The typical rental home has 2 bedrooms and 1.5 bathrooms, and is 1000 – 1999 square feet (500-999 for recent renters).[1] About two-thirds of recent renters (68%) moved from a previous rental.

How much do recent renters pay upfront?

The typical (median) recent renter submitted 2 applications. For those that paid an application fee (68%), the typical amount was between $40 and $59. Most recent renters (87%) also reported paying a security deposit — typically $500 to $999 among renters that paid one. Application fees and security deposits follow many similar trends: renters in urban and suburban areas, renters of color, younger renters, and renters in regions with the most expensive rental markets are all more likely to pay an application fee and/or a security deposit, and those upfront costs tend to be higher.

What characteristics do they consider important in a rental?

From a series of home characteristics, renters are most likely to say that a home that’s within their initial budget is very or extremely important (80%), followed by having their preferred number of bedrooms (68%). Despite continued easing of COVID-19-pandemic restrictions, recent renters remained similarly unlikely to consider shared amenities like gyms, rooftop decks and pet areas as highly important.

Who is planning to move (again)?

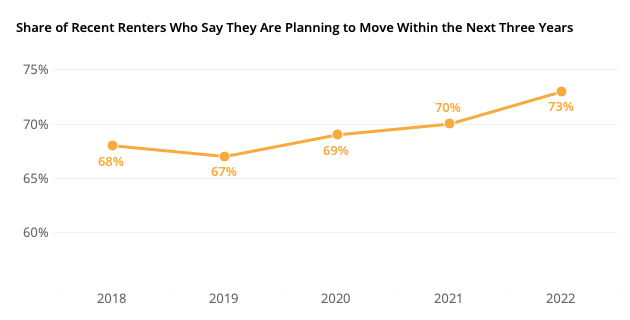

About two-thirds of renters (64%) say they are considering moving within the next three years. For recent renters, the share is even larger: 73% say they plan to move again in the next three years. Despite the unprecedented events of the last two years, this number has remained relatively flat from 2018 (68%), 2019 (67%), 2020 (69%), and 2021 (70%). Among renters considering moving, about half (49%) say they plan to continue renting while 45% say they plan to buy their next home. The remainder (6%) say they plan to have another living situation.

Survey Methodology

Research Approach

In order to gain a comprehensive understanding of U.S. renters, Zillow Group Population Science conducted three nationally representative surveys – each sampling with at least 3,000 renter-respondents. In total, the three surveys contain information from 8,300 unique renters – more than 2,500 recent renters and 5,700 tenured renters. Participants were allowed to take more than one survey. The study was fielded between March and June 2022.

Wherever possible, survey questions from previous years were asked in the same manner this year to allow for the measurement of year-to-year trends in key areas of business interest.

For the purpose of this study, “renters” refers to household decision makers 18 years of age or older who rent their primary residence. “Recent renters” refer to those that moved in the past year, and “tenured renters” refer to those that did not move in the past year.

Sampling & Weighting

Results from this survey are nationally representative of renters. To achieve representativeness, ZG Population Science used a two-prong approach. First, the initial recruitment to the sample was balanced to all renters from the U.S. Census Bureau, 2019 American Community Survey (ACS) on the basis of age, relationship status, income, ethnicity/race, education, region and sex. The survey targeted subgroups based on all key household demographic characteristics. Second, statistical raking was used to create calibration weights to ensure that the distribution of survey respondents matched the U.S. population with respect to a number of key demographic characteristics. Weighting benchmarks used the 2019 ACS for race and income and the 2021 Current Population Survey Annual Social and Economic Supplement (CPS ASEC) for geographic division/region, education, age and sex.

Quality Control

To reduce response bias, survey respondents did not know that Zillow Group was conducting the survey. Several additional quality control measures were also taken to ensure data accuracy:

- We identified and terminated any professional respondents, robots or those taking the survey on multiple devices.

- Completion times were recorded to ensure that surveys submitted by the fastest respondents, who may have rushed through the survey, did not provide poor quality data. If necessary, these respondents were removed from the sample.

- In-survey quality control checks identified illogical or unrealistic responses.

Additional Data Sources

Unless otherwise specified, estimates in this report come from the Consumer Housing Trends Report (CHTR) 2022, and year-over-year comparisons also use data from CHTR 2018, CHTR 2019 CHTR 2020, and CHTR 2021. To provide a fuller picture of the state of home rentals and renters’ characteristics, preferences and behaviors, we also analyzed data from other sources:

- U.S. Census Bureau, 2019 American Community Survey – Despite the release of ACS 2020 data, changes in sampling methodology during the pandemic resulted in certain unrealistic estimates for renters. To better capture renter heterogeneity, Zillow Population Science used ACS 2019 as the most recently available reliable dataset from the U.S. Census Bureau’s survey of the U.S. population. The ACS is the nation’s largest survey and is based on a probability sample; as such, it is considered one of the leading sources of information on U.S. population and housing.

- U.S. Census Bureau, 2021 Current Population Survey Annual Social and Economic Supplement – The CPS ASEC offers the most recent demographic estimates on renters.

- Zillow.com website metrics – To provide additional context for survey results, ZG Population Science also examined internal Zillow data on rental listing information, rental applications, and page view / app use metrics.

- Zillow Group Population Science Fall 2020 Survey of Renters – Because many young renters moved out of the rental market at the start of the COVID-19 pandemic, this survey supplemented previous ZG Population Science research on both shifting and stable sentiment among renters while capturing an age demographic that was atypically absent from the rental market earlier that year. Topics included renter preference on location, virtual home searching tools, and reasons for moving.

The Typical Renter & Rental

In this section, we provide a high-level overview of key renter info and what their homes look like. According to Census Bureau 2021 Current Population Survey Annual Social and Economic Supplement, 30% of adults in the country are renters (regardless of whether they moved in the past year). About a fifth (17%) of these renters moved in the past year.

Age

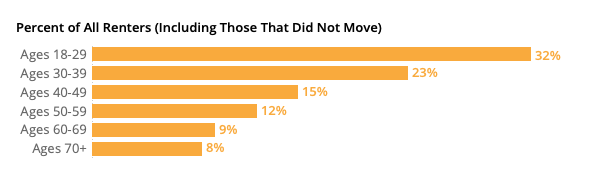

The median age of U.S. renters is 39 years old and about two-thirds (65%) of renters are under the age of 40; only 8% of renters are in their seventies or older, and 9% are in their sixties. In other words, the age distribution of renters trends younger than the overall U.S. population. While past research has referred to renters that moved in the past year, renters as a whole, including tenured renters who did not move, skew older. The median age for a tenured renter (who did not move in the past year) is 39 — almost a decade older than the typical renter that moved (30).

| Age Group |

Percent of Recent Renters |

Percent of All Renters (including those that did not move) | Percent of Household Decision Makers [2] |

Percent of US Adults |

| Ages 18-29 |

41% |

32% | 12% |

20% |

| Ages 30-39 |

24% |

23% | 18% |

17% |

| Ages 40-49 |

13% |

15% | 17% |

16% |

| Ages 50-59 |

10% |

12% | 18% |

16% |

| Ages 60-69 |

7% |

9% | 17% |

15% |

| Ages 70+ |

4% |

8% | 17% |

15% |

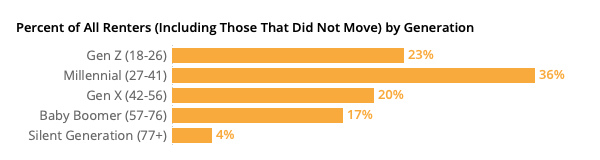

Consistent with age, the largest generational group of renters is between 27 and 41 years old in 2021 — the group colloquially known as “Millennials.” About 42% of renters are Millennials.

| Generation [3] |

Percent of Recent Renters |

Percent of All Renters (including those that did not move) | Percent of Household Decision Makers |

Percent of US Adults |

| Gen Z (18-26) |

30% |

23% | 7% |

14% |

| Millennial (27-41) |

39% |

36% | 27% |

26% |

|

Gen X (42-56) |

17% | 20% | 26% |

23% |

| Baby Boomer (57-76) |

12% |

17% | 32% |

28% |

| Silent Generation (77+) |

4% |

4% | 8% |

7% |

Source: Census Bureau, 2021 Current Population Survey Annual Social and Economic Supplement

Race & Ethnicity

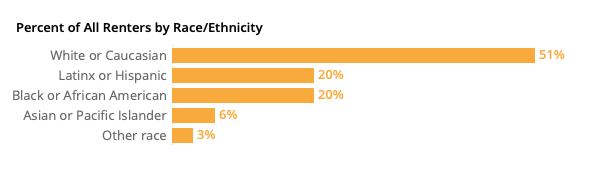

Just over half of renters are non-Hispanic white or Caucasian (56%), smaller than the overall share of the U.S. adult population that is white (63%). At the same time, 12% of U.S. adults identify as non-Hispanic Black or African American, while 20% of renters are Black.

| Race/Ethnicity | Percent of Recent Renters | Percent of All Renters | Percent of Household Decision Makers | Percent of US Adults |

| White or Caucasian |

56% |

51% | 66% |

63% |

| Black or African American |

17% |

20% | 12% |

12% |

| Latinx or Hispanic |

17% |

20% | 13% |

16% |

| Asian or Pacific Islander |

7% |

6% | 5% |

6% |

| Other race |

4% |

3% | 2% |

3% |

Source: Census Bureau, 2019 American Community Survey

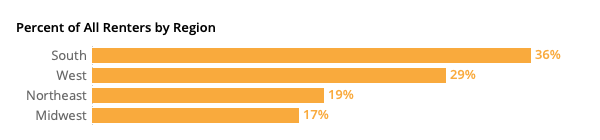

Region

The largest share of renters live in the South (39%), followed by the West (25%) and Midwest (21%). The smallest share lives in the Northeast (15%).

| Region |

Percent of Recent Renters |

Percent of All Renters | Percent of Household Decision Makers |

Share of US Adults |

| South |

39% |

36% | 38% |

38% |

| West |

25% |

29% | 23% |

24% |

| Midwest |

21% |

17% | 21% |

21% |

| Northeast |

15% |

19% | 17% | 17% |

Source: Census Bureau, 2021 Current Population Survey Annual Social and Economic Supplement

| Region |

Percent of Adults that Rent |

Percent of Household Decision Makers that Rent |

Percent of Renters that Recently Moved |

| South |

28% |

28% |

20% |

| West |

36% |

36% |

13% |

| Midwest |

25% |

25% |

21% |

| Northeast |

32% |

33% |

16% |

Source: Census Bureau, 2021 Current Population Survey Annual Social and Economic Supplement

Gender Identity & Sexual Orientation

About one in ten (11%) recent renters identified as LGBTQ+ in 2019, the first year CHTR asked about sexual orientation and gender identity, then 16% in 2020. The share that identified as LGBTQ+ peaked in 2021 at 22%. In 2022, 18% of recent renters identified as LGBTQ+.[4] Recent renters are more likely to identify as LGBTQ+ (18%) than tenured renters (12%) or renters as a whole (13%). Younger renters are more likely to self-identify as LGBTQ+: The median age of an LGBTQ+ renter is 29 – versus 41 for cisgender heterosexual renters. Renters trending younger than the US adult population as a whole may help explain why renters are also more likely to identify as LGBTQ+.

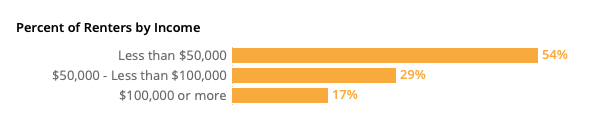

Income

Renters tend to have lower incomes than the U.S. population overall. The annual median household income among renters is approximately $42,500, compared to the overall national median of $67,500. [5]

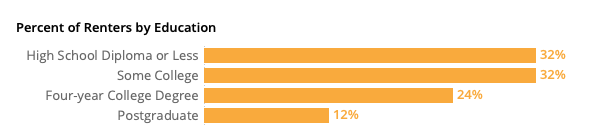

Education

Renters tend to have a similar level of education to the overall population of U.S. household decision makers: 36% of renters have at least a four-year degree, similar to 34% of overall U.S. household decision makers.

| Education |

Percent of Renters |

Percent of Household Decision Makers |

| High School Diploma or Less |

32% |

36% |

| Some College |

32% |

30% |

| Four-year College Degree |

24% |

21% |

| Postgraduate |

12% |

13% |

Relationship Status

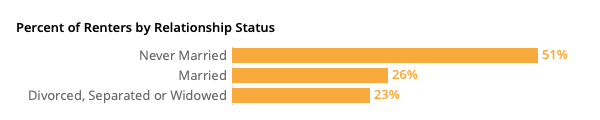

Skewing younger than the U.S. population as a whole, renters are less likely to be married, divorced, separated or widowed. A majority (51%) are single and never married. These differences in relationship status may provide a partial explanation for the lower household income of renters compared with the overall population.

Household Composition [6]

- 29% of renters have children under age 18 in their homes

- 2% of renters have their parents or parents-in-law in their homes

- 38% have at least one dog

- 29% have at least one cat

- 13% have another kind of pet

Urbanicity

Almost half of renters describe the area that they live in as suburban (45%); 41% say they live in an urban area, and the remaining 14% say they live in a rural area.

Home Type, Beds, Baths, and Size

Apartments of various sizes are what most renters call home: 53% of renters report living in an apartment building. About one in five renters (17%) say they rent in a smaller-size apartment building (fewer than 10 units). The same share (17%) said they live in a medium-size building (10-49 units), and 19% said they live in a larger multifamily building (50 units or more). About 21% live in a single-family detached house.

| Home Type | Share of Renters |

| Apartment in a smaller size building (fewer than 10 units) | 17% |

| Apartment in a medium size building (10-49 units) | 17% |

| Apartment in a larger size building (50 units or more) | 19% |

| Condominium / co-op | 4% |

| Single-family detached house | 21% |

| Townhouse / rowhouse | 8% |

| Duplex / triplex | 5% |

| Room in shared housing | 3% |

| Income restricted rental home / community | 2% |

| Other | 4% |

The typical (median) renter lives in a 2-bed, 2-bath, apartment between 500 and 999 square feet.

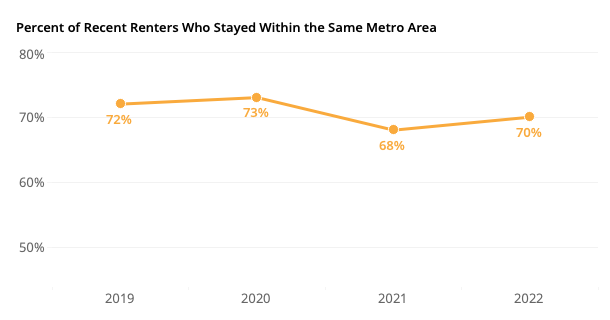

Most Recent Movers Changed Neighborhoods, but Stayed Local

When asked how far they moved, the largest share of recent renters said they stayed in the same city, but changed neighborhoods (40%). About one in ten (11%) reported staying in the same neighborhood. The smallest share (3%) moved from abroad.

| Distance Moved | 2019 | 2020 | 2021 | 2022 |

| Same neighborhood | 16% | 14% | 11% | 11% |

| Same city, different neighborhood | 38% | 40% | 39% | 40% |

| Same metro, different city | 19% | 19% | 19% | 19% |

| Same state, different metro | 13% | 12% | 16% | 15% |

| Same country, different state | 13% | 13% | 13% | 13% |

| Moved from abroad | 2% | 2% | 2% | 3% |

That is, about 70% of recent renters stayed within the same metro area. Over time, this number has largely stayed stable (72% in 2019, 73% in 2020, 68% in 2021).

Upfront Costs

Applications & Application Fees

Paying a rental application fee was the norm across generations. However, younger renters were more likely to submit at least one application than their older counterparts. While most Gen Z (83%), Millennial (74%) and Gen X (79%) renters paid at least one application fee, less than half (42%) of Boomer & Silent Generation renters paid one.

The 2021 Consumer Housing Trends Report hypothesized that older renters were more likely to have personal connections to their landlords – helping to explain the lower likelihood of paying an application fee. We added questions to this year’s survey to examine this possibility. Findings from this new content (in 2022) paint a more complex portrait: Across age groups, renters reported knowing their landlord or property manager personally at similar rates.

| Age Group | Share that Paid An Application Fee | Share that Paid An Application Fee of At Least $40 |

| Ages 18-29 | 70% | 28% |

| Ages 30-39 | 64% | 26% |

| Ages 40-49 | 59% | 23% |

| Ages 50-59 | 50% | 19% |

| Ages 60+ | 41% | 18% |

| Generation | Share that Paid an Application Fee | Share that Paid An Application Fee of At Least $40 |

| Gen Z (Ages 18-27) | 71% | 29% |

| Millennial (Ages 27-41) | 65% | 26% |

| Gen X (Ages 42-56) | 56% | 21% |

| Baby Boomers & Silent Generation (Ages 57+) | 42% | 18% |

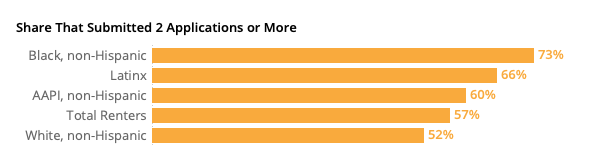

Across racial groups, paying an application fee is more common than not, but renters of color are more likely to report paying one: Larger shares of Black (69%), Latinx (65%), and Asian American/Pacific Islander (60%) renters reported paying an application fee than white renters (53%). Black and Latinx renters were also almost twice as likely to report submitting 5 applications or more (38% of Black and Latinx renters report submitting 5 or more, compared to 21% of white renters). Renters of color report paying a higher median application fee than white renters: The typical white renter reported paying $35 in application fees on their rental, while the typical Black, Latinx, and Asian renters all reported spending $50 on application fees. [7]

| Race/Ethnicity |

Share that Paid an Application Fee |

Share that Paid At Least $40 |

Share that Paid At Least $100 |

Share that Submitted 2 Applications or more |

| Total Renters |

59% |

23% |

9% |

57% |

| White, non-Hispanic |

53% |

20% |

8% |

52% |

| Black, non-Hispanic |

69% |

25% |

10% |

73% |

| Latinx |

65% |

31% |

12% |

66% |

| AAPI, non-Hispanic |

60% |

28% |

9% |

60% |

LGBTQ+ renters were more likely to report paying an application fee: 66% of LGBTQ+ renters said they paid one – higher than 57% of cisgender heterosexual renters. LGBTQ+ renters are also more likely to submit a greater number of applications: 68% submit two or more – compared to 57% for cisgender heterosexual renters. And 19% submit 5 or more – just above 15% for cisgender heterosexual renters.

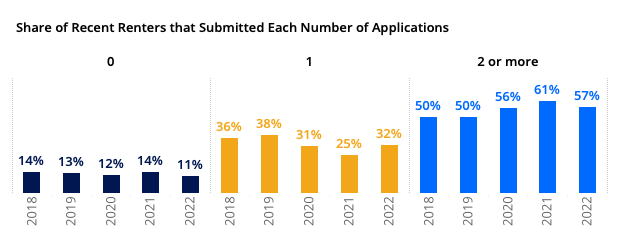

| Share of Renters that Submitted Each Number of Applications |

Total Renters |

LGBTQ+ |

Cisgender Heterosexual |

| 0 |

12% |

9% |

12% |

| 1 |

29% |

22% |

30% |

| 2 or more |

59% |

68% |

57% |

| 5 or more |

16% |

19% |

15% |

LGBTQ+ renters are about 28% more likely to report recently moving than cisgender heterosexual renters. This higher move likelihood means that LGBTQ+ renters disproportionately feel the effect of upfront costs of moving, and may experience them more often.

Renters in large multifamily buildings (those with 50 units or more) were most likely to report submitting at least one application: 96% do, compared with 81% of those in single-family detached houses and 89% of those renting other home types.

| Type of Home Rented | Share that Submitted At Least 1 Application | Share that Paid an Application Fee | Median Application Fee | Median Application Fee Among Renters Who Paid One |

| Total Renters | 88% | 59% | $20 – $39 | $40 – $59 |

| Multifamily (50+ units) | 96% | 72% | $40 – $59 | $40 – $59 |

| Single-family detached | 81% | 47% | $0 | $40 – $59 |

| Other | 89% | 62% | $20 – $39 | $40 – $59 |

Security Deposits

For renters that pay one, the typical security deposit reported in 2022 was $500 – $999.

The oldest generations of renters are the most likely to avoid paying a deposit at all: 81% report paying a security deposit — lower than 87% of Gen Z, 86% of Millennial, and 85% of Gen X renters.

| Generation | Share that Paid a Security Deposit |

| Total Renters | 85% |

| Gen Z (Ages 18-27) | 87% |

| Millennial (Ages 27-41) | 86% |

| Gen X (Ages 42-56) | 85% |

| Baby Boomers & Silent Generation (Ages 57+) | 79% |

| Age Group |

Share that Paid a Security Deposit |

| Total Renters |

85% |

| Ages 18-29 |

87% |

| Ages 30-39 |

86% |

| Ages 40-49 |

88% |

| Ages 50-59 |

82% |

| Ages 60+ |

80% |

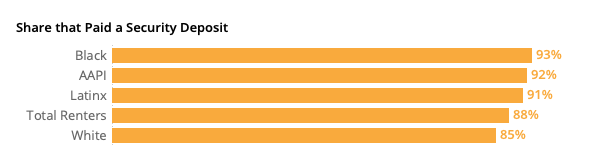

Renters of color are more likely to report paying a security deposit: 86% do, compared to 84% of white renters. Latinx and Asian American/Pacific Islander renters are more likely to pay a more expensive deposit: 39% of Latinx and 43% of AAPI renters paid at least $500 for their deposit, and 22% of Latinx and 30% of AAPI renters paid at least $1,000.

| Race/ Ethnicity |

Share that Paid a Security Deposit |

Deposit of At Least $500 |

Deposit of At Least $1,000 |

| Total Renters |

88% |

33% |

18% |

| White |

85% |

32% |

17% |

| Black |

93% |

28% |

13% |

| Latinx |

91% |

39% |

22% |

| AAPI |

92% |

43% |

30% |

Regardless of the type of home rented, paying a deposit is the norm: 85% of renters reported paying one. Renters in single-family detached houses, though, can be slightly more likely to dodge paying a deposit: 21% of single-family renters reported paying no security deposit – higher than 11% of multifamily renters and 13% of renters in other home types. When they don’t avoid paying one, single-family deposit amounts are typically higher: The typical security deposit among single-family renters that pay one was $1,000 – $1,499 – higher than the median of $500 – $999 for renters in multifamily and other types of buildings. A lower likelihood of paying an application fee (which often includes a credit check) combined with the fact that single-family renters are more likely to rent from a private owner (who may be less able to offset risk from a single tenant than a professional management company) likely contribute to this difference.

| Type of Home Rented |

Share that Paid a Security Deposit |

Median Security Deposit | Median Security Deposit Among Renters Who Paid One | Share that Paid At Least $500 |

Share that Paid At Least $1,000 |

| Total Renters |

85% |

$500 – $999 | $500 – $999 | 33% |

18% |

| Multifamily (50+ units) |

89% |

$250 – $499 | $500 – $999 | 26% |

15% |

| Single-family detached |

79% |

$500 – $999 | $1,000 – $1,499 | 41% |

24% |

| Other |

87% |

$500 – $999 | $500 – $999 | 31% |

17% |

| Type of Home Rented |

Share that rent from a private owner (rather than a professional management company) |

Share that knew their landlord/property manager personally |

| Total Renters |

51% |

20% |

| Multifamily (50+ units) |

15% |

11% |

| Single-family detached |

77% |

27% |

| Other |

46% |

19% |

Resources Renters Use When Shopping & Searching

More Recent Renters Searching on Mobile Devices

The share of recent renters that say they searched on a mobile website held onto its increase from 2021: (74% in 2022 and 2021, up from 65% in 2020) and/or on a mobile app (60% in 2022 and 2021, up from 51% in 2020).

| Online resources used when searching |

2019 |

2020 | 2021 |

2022 |

| Website on a laptop / desktop computer |

70% |

72% |

73% |

67% |

| Mobile website on a smartphone / tablet |

64% |

65% |

74% |

74% |

| App on a smartphone / tablet |

46% |

51% |

60% |

60% |

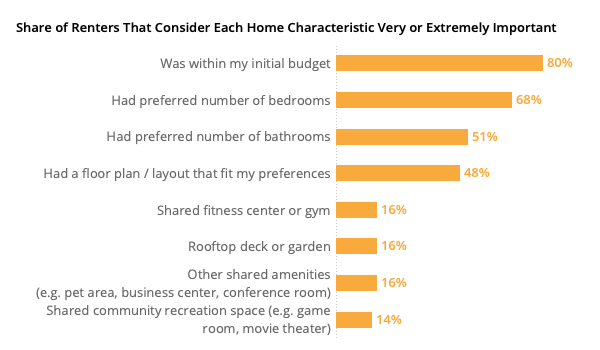

Home Characteristics that Renters Consider Highly Important

Importance of Staying on Budget Persists

When asked what home characteristics they are most likely to consider very or extremely important, renters have consistently said that staying within their initial budget is highly important. The largest majority (80%) said so, higher than any other home characteristic.

Preferred number of bedrooms was the runner-up, at a distant 68%. Despite the rise of remote work with the COVID-19 pandemic, the importance of renters’ preferred number of bedrooms has held steady over the last few years.

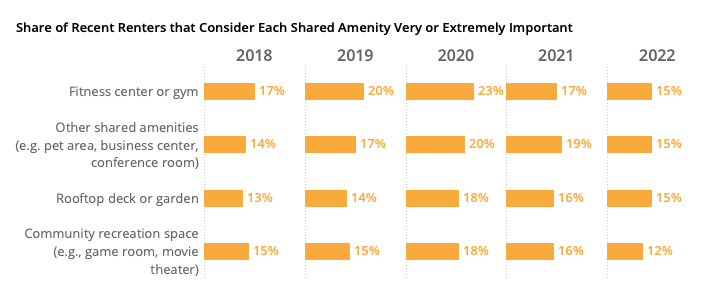

No “Post-Pandemic” Rebound for Importance of Common Amenities

Between 2018 and 2020, the share of recent renters that considered various shared community amenities like gyms, decks, gardens, and game rooms highly important inched upward. In 2021’s survey, however, this trend appears to have ground to a halt or even reversed. And in 2022, despite many of these amenities reopening, recent renters were similarly or less likely to consider each highly important.

The likelihood that recent renters consider each common amenity highly important dropped in 2022 from peaks in 2020: a shared fitness center or gym dropped from 23% in 2020 to 15% in 2022; a community recreation space dropped from 18% to 12%; rooftop deck or garden fell from 18% to 15%, and other shared amenities fell from 20% to 15%.

Pandemic Coincided with an Increase in the Share of Renters Considering Buying

Most Considered Buying During their Rental Search

A majority of recent renters said in 2022 that they considered buying when they were looking for a home to rent: 66% said they at least thought about it, up from 56% in 2021, 55% in 2020, 49% in 2019, and 46% in 2018.

Millennial renters were the most likely to say they considered buying: 70% said so, significantly higher than the oldest generations of renters — closer to half of Baby Boomer and Silent Generation renters (47%) said they at least thought about buying.

| Considered Buying |

Total Renters |

Gen Z (Ages 18-27) |

Millennial (Ages 28-42) |

Generation X (Ages 43-57) |

Boomers + Silent Gen |

| Never considered buying |

37% |

34% | 30% | 41% |

53% |

| Seriously considered buying instead |

23% |

23% | 27% | 24% |

10% |

| Thought about buying, more serious about renting |

41% |

43% | 43% | 36% |

36% |

| NET: Considered buying |

63% |

66% | 70% | 59% |

47% |

Almost Three Quarters of Recent Renters Consider Moving Again Within the Next 3 Years

Similar both before and after the pandemic, recent renters consistently consider moving: 73% say they are considering it within the next 3 years. About a quarter (23%) say they are currently considering moving, and almost one in three (31%) say they’re considering moving in the next year. Another fifth (19%) say they’re considering it within the next two to three years. About one in ten (12%) say they might consider moving, but not within the next 3 years. And the remaining 15% say they have no plans to move.

| Moving Consideration |

2018 |

2019 | 2020 | 2021 |

2022 |

| No plans to move |

20% |

20% | 19% | 17% |

15% |

| Might consider moving, but not within next 3 years |

12% |

14% | 12% | 14% |

12% |

| Considering moving in the next 2-3 years |

22% |

20% | 23% | 24% |

19% |

| Considering moving in the next year |

22% |

23% | 26% | 21% |

31% |

| Currently considering moving |

24% |

24% | 20% | 24% |

19% |

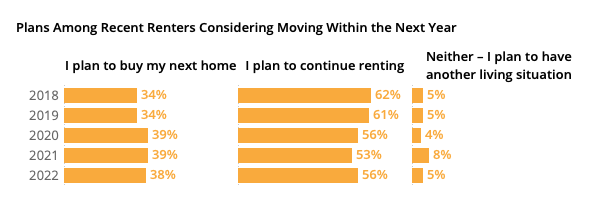

The Share Considering Moving Remained Stable, But Plans to Buy Stayed Up

In 2018 and 2019, 34% of recent renters considering moving within the next year said they planned to buy their next home. In 2020, the share increased slightly to 39%, and in 2021, the same share (39%) said they planned to buy. In 2022, recent renters appeared more likely to report plans to buy their next home: 44% said home buying was their next plan.

Demand for Digital Tools Stable, Up in Some Cases

A Quarter of Recent Renters Took Zero In-Person Tours

The typical recent renter surveyed in 2022 reported taking only one in-person tour. Going on at least two in-person tours is still quite common, however: 40% of recent renters reported taking at least two. 2022 continues the trend from last year: About one in four (23%) recent renters said they forewent in-person tours entirely.

| Share of Recent Renters that Reported Taking |

2018 |

2019 | 2020 | 2021 |

2022 |

| 0 In-Person Tours |

21% |

19% | 18% | 23% |

23% |

| 1-4 In-Person Tours |

62% |

63% | 67% | 68% |

71% |

| 5 or More In-Person Tours |

16% |

17% | 15% | 10% |

6% |

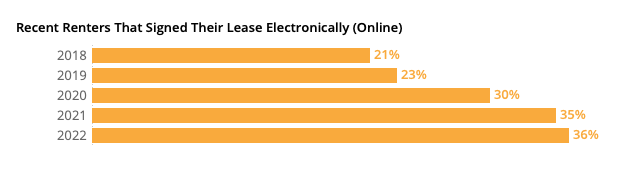

Rise in Electronic Lease Signing Holds

While the share of recent renters that signed their lease electronically stayed largely unchanged between 2018 and 2019 (21% and 23% respectively), 2020 saw a substantial increase to 30%, and the trend continued in the 2021 survey, where 35% of recent renters reported signing their leases electronically. In 2022, 36% of recent renters reported signing electronically – similar to 2021. In-person leases are still the norm for a majority of renters (55%), but have been on a downward trend since last year.

While the share of recent renters that actually signed electronically remained similar to 2021, the share that would ideally prefer to sign electronically increased 8 points to 53%. Despite landlords and property managers stepping up their offering of electronic leasing options, the gap between the share of recent renters that signed online (36%) and would ideally prefer to sign online (53%) widened in 2022.

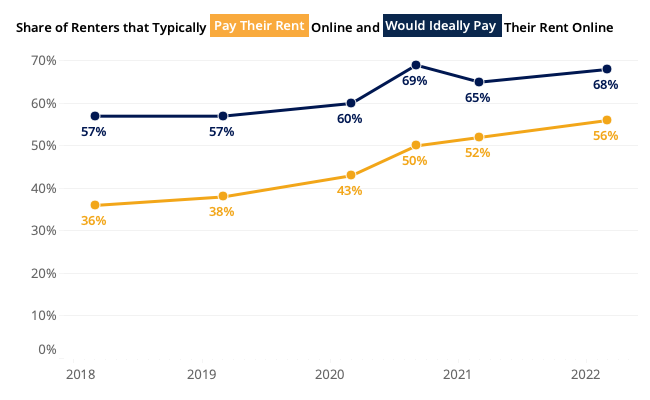

Half of Renters Pay Rent Online – More Would Like To

In fall of 2020, half (50%) of recent renters said they typically pay their rent online. Since then, the share has risen a slight 6 points to 56%. Over the same time, the share of recent renters that said they would ideally prefer to pay their rent online remained similar: 69% in fall 2020 and 68% in spring/summer of 2022.

| Gap Between Share of Renters that Typically and Would Ideally Pay Rent Online | |||||

| Spring 2018 | Spring 2019 | Spring 2020 | Fall 2020 | Spring & Summer 2021 | Spring & Summer 2022 |

| 21% | 20% | 17% | 19% | 13% | 12% |

Half of Renters Get At Least One Perk or Concession

Among recent renters that recalled which concessions they received, 54% said they got at least one – similar to 55% in 2020. The most common perk that renters reported getting was parking — about a quarter (24%) said parking was included in their rental agreement. Frequency of most individual concessions stayed similar to 2021.

| Among recent renters that remember whether they got any concessions |

2020 |

2021 |

2022 |

| First month rent free |

13% |

15% |

12% |

| More than first month rent free |

7% |

5% |

5% |

| Reduced rent |

12% |

13% |

12% |

| Parking |

19% |

25% |

24% |

| Reduced security deposit |

11% |

10% |

8% |

| Free/discounted access to paid property amenities (laundry, internet, etc…) |

10% |

12% |

11% |

| Broker’s fee paid |

5% |

4% |

3% |

| Gift card |

6% |

5% |

5% |

| Something else |

6% |

6% |

4% |

| I didn’t receive any concessions |

45% |

41% |

46% |

| Net: Received Concession |

55% |

59% |

54% |

Concessions Appear to Have Peaked in February

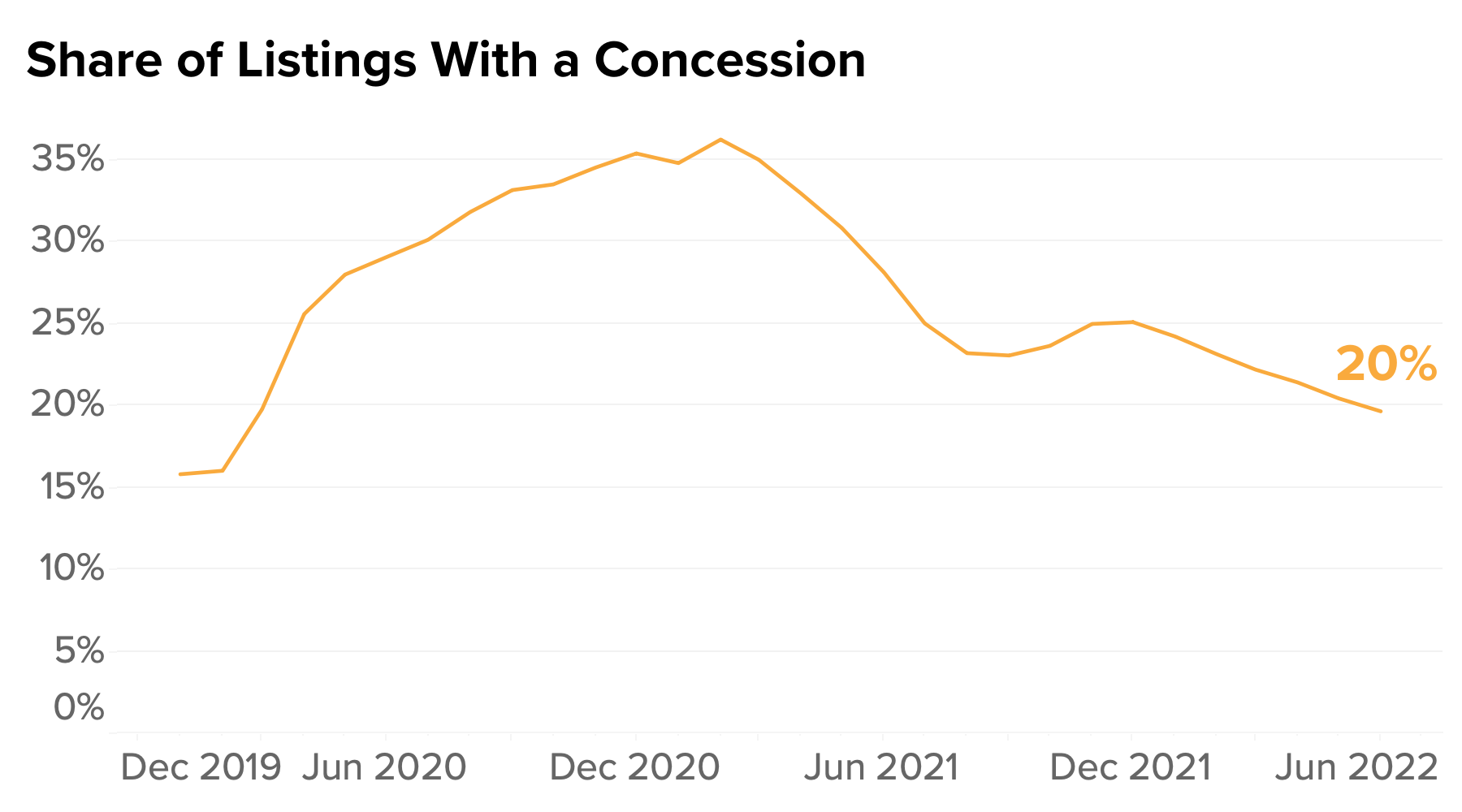

According to an analysis of Zillow rental listings, the share of listings that advertised at least one concession peaked in February 2021 (36% mentioned one). By June 2022, that number had dropped to 20%.

Perks & Concessions More Common for Young and Multifamily Renters

The youngest generation of renters (those age 27 and younger) were the most likely to secure at least one perk or concession in their rental agreement: 67% reported doing so, higher than 51% of those between 28 and 42 years old, and even higher than older generations.

| Among renters that remember whether they got any concessions |

Gen Z (Ages 18-27) |

Millennial (Ages 28-42) | Generation X (Ages 43-57) |

Boomers + Silent Gen (58+) |

| Share that got at least 1 perk/concession |

67% |

51% | 37% |

36% |

Renters in large multifamily buildings were also more likely to report getting a concession: 58% said they did, compared to 36% of renters in single-detached houses. Renters in other home types were the middle ground: 52% reported getting at least one concession.

| Among renters that remember whether they got any concessions | Single-Family Detached House | Multifamily Apartment Building | Other |

| Share that got at least 1 perk/concession |

36% |

58% |

52% |

Renters in each of these groups associated with a higher likelihood of reporting a concession may not actually be more likely to receive each perk, like parking, but rather more likely to consider such a perk as something they cannot take for granted: Renters in single-detached houses, for example, may consider parking as a given, which may explain why 87% didn’t report receiving it as a concession or perk.

12 Months Is the Most Common Lease Duration

A Quarter of Renters are Month-to-Month

About a quarter (24%) of renters say that their lease allows them to leave with no more than a month of notice. For recent renters, the share is smaller: 15% of those that moved in the past year say their lease allows them to leave with no more than a month of notice.

12 Months Is the Norm for 2/3rds of Fixed-Term Renters

Among renters on a fixed-term lease, two-thirds (67%) say they signed on for a 12-month duration. About one in five (19%) say their lease is longer than a year. One in ten (10%) say their lease is 2 years or longer, and one in seven (14%) say their lease is shorter than 12 months.

[1] Renters were asked about their home’s square footage in ranges. According to the 2019 American Housing Survey, the median was 980 square feet.

[2] Zillow Group Population Science calculates estimates for “household decision makers” when utilizing U.S. Census Bureau data by averaging the characteristics of heads of household and their spouses and/or partners within a household. For renter households, this definition also includes roommates/housemates.[3] Zillow Group Population Science defines Gen Z as those born between 1995 and 2003, Millennials between 1980 and 1994, Gen X between 1965 and 1979, Baby Boomers between 1945 and 1964, and Silent Generation in 1944 and earlier.[4] LGBTQ+ renters are those who identified as gay, lesbian, bisexual, transgender, gender non-conforming/non-binary, intersex, or with another sexual orientation (other than straight) or gender identity (e.g. gender fluid, gender queer, gender neutral).

[5] National median income is from U.S. Census Bureau, 2021 Current Population Survey Annual Social and Economic Supplement.

[6] These estimates come from CHTR 2021 and the 2019 American Community Survey.

[7] These higher fees and number of applications that renters of color disproportionately experience may at least be partially attributable to age, income, and geography: The typical renter of color is 2 years younger than the median white renter. White renters are more likely to rent in rural markets and the Midwest, both of which generally skew less expensive, while renters of color are more likely to rent in urban markets. Asian and Latinx renters in particular are more likely to rent in the West, which includes many of the country’s most expensive and competitive rental markets. Exploratory analyses of the data suggest that differences in region, urbanicity, age structure, and income explain about 10-20% of Latinx-white differences. Models, however, are underpowered for a more detailed accounting of sources of racial/ethnic differences.