The Gap in Selling Intentions Between Those With Rates Above and Below 5% Shrank at the End of 2023

-

- The “plans to sell” gap between below and above 5% mortgage rate holding homeowners has shrunk. Earlier research indicated that 5% was a tipping point for intentions to sell.

- While interest rates remained well above 5% since mid-2022, mortgage-rate fluctuations have had little impact on selling intentions of homeowners paying mortgage rates below 5%.

- In contrast, selling intentions of mortgaged homeowners with rates above 5% have been more susceptible to rate fluctuations.

- Despite falling rates at the end of 2023, higher-mortgaged homeowners might still remain financially cautious and hold off on selling and buying due to stagnant home prices and general economic uncertainty

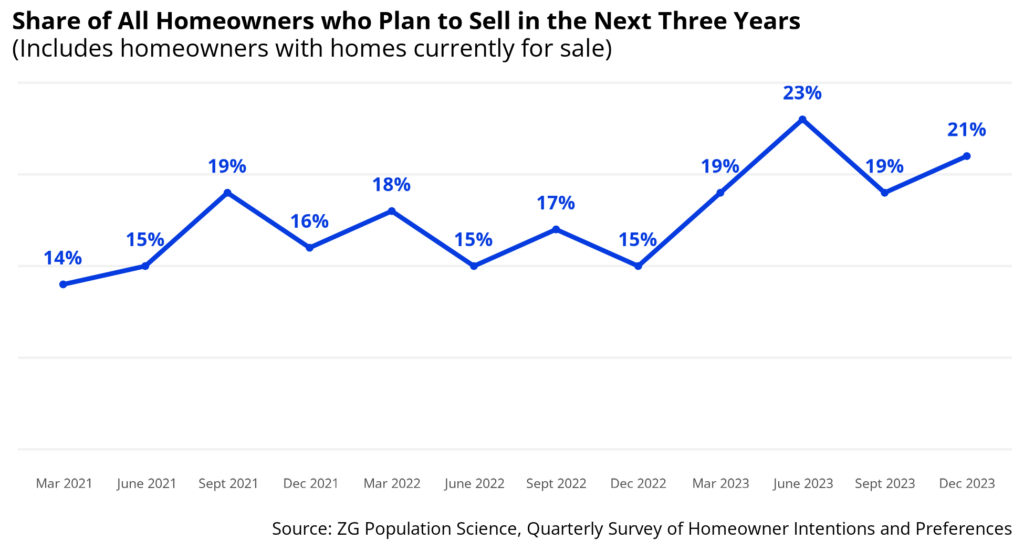

- Still, selling intentions of all homeowners were slightly higher across 2023 compared to past years: 21% of homeowners currently have their home listed for sale or are considering selling their home

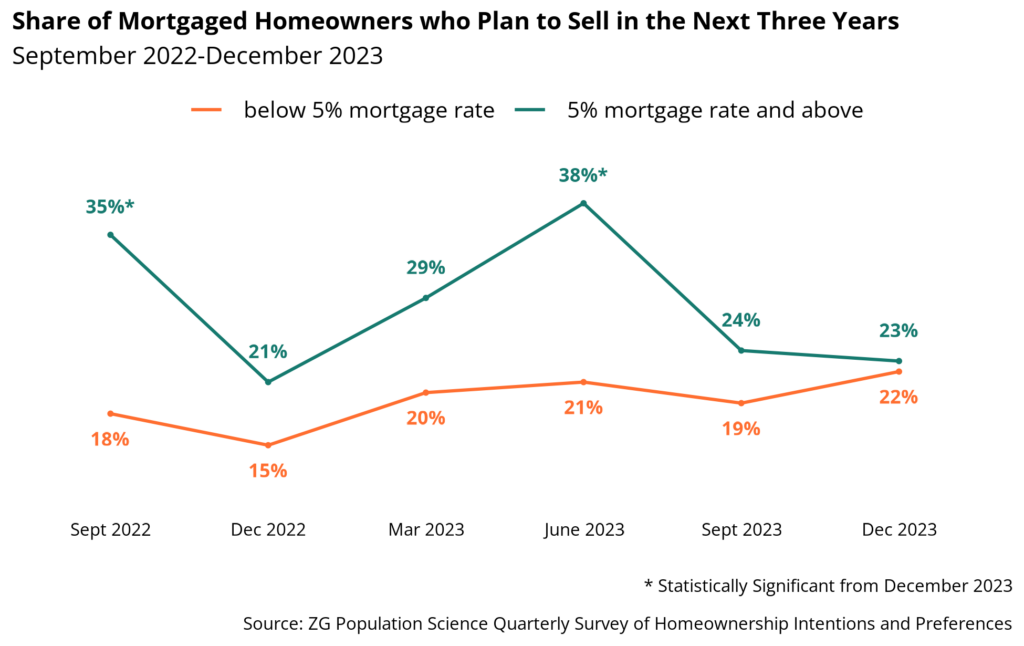

In June 2023, we saw that a 5% mortgage rate was the “tipping point” for homeowners to consider selling. Homeowners who reported above a 5.00% mortgage rate were almost twice as likely to consider selling than homeowners below.

Why were we seeing this gap? Increased mortgage rates since 2021 have implied additional financial costs to moving to a new home. A house of the same value now requires a substantially higher monthly mortgage payment than it did a couple of years ago. And most (54%) seller-buyers tend to buy a more expensive home than the one they sold. This increased cost of transaction has effectively kept homeowners with lower rates “locked-in” to their current home while they wait for lower rates.

Does the gap between homeowners with mortgages below and above 5% still hold true?

In contrast to 6 months ago, a recent survey from Zillow Group Population Science now shows that the “plans to sell” gap between mortgaged homeowners below and above 5% has shrunk.

In September 2023, the gap shrunk to a 5 percentage-point difference between higher- and lower- rated homeowners. By December 2023, the gap was no longer statistically different (22% for homeowners with rates below 5% and 23% for homeowners with rates above 5%).

While market rates remain well above 5%, they have had little motivating impact on the selling plans for mortgaged homeowners holding rates below 5%

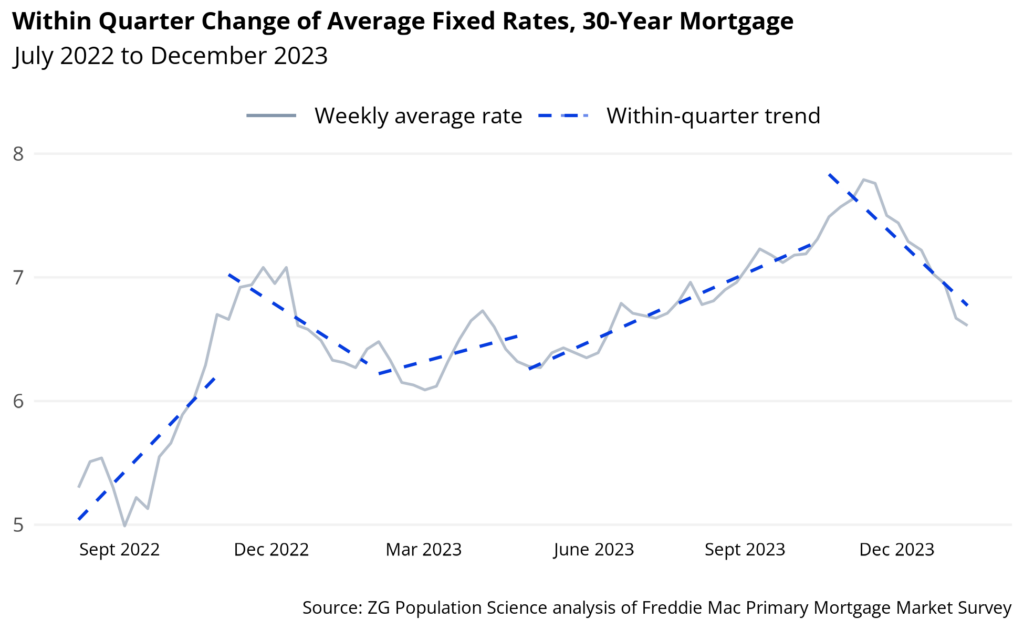

For almost 12 years after the 2008 recession, the average fixed rate (AFR) for 30-year mortgages, according to Freddie Mac, remained below 5%. However, by mid-2022, that flipped: the average weekly rate since then has increased well above the 5% mark, nearing almost 8% in October 2023 before a more recent decrease in the last three months.

ZG Population Science research suggests that while mortgage rates remain well above 5%, the fluctuations of these rates have had little motivating impact on the selling plans for mortgaged homeowners with rates below 5%. Rather, a steady share (almost one in five) of below 5% mortgaged homeowners continue to have plans to sell regardless of increasing and decreasing rates. Since September 2022, this share has held consistently around 18-20% [1] and increased slightly to 22% in December 2023.

In contrast, selling intentions of mortgaged homeowners with rates above 5% were more susceptible to rate fluctuations.

The selling intentions of homeowners with rates above 5% have experienced notable shifts in reaction to three different factors: direction of the trend, speed of increase or decrease, and level of the average mortgage rate.

A steep increase of average mortgage rates over three months was accompanied by a steep decrease in above 5.00% mortgaged homeowners’ selling intentions. In December 2022, when average mortgage rates experienced the sharpest increase over three months, the proportion of above 5.00% mortgaged homeowners with plans to sell dropped by 40 percent from 35% to 21%. Then, when mortgage interest rates dropped in the beginning of 2023, the share of above 5.00% mortgaged homeowners with intentions to sell rose from 21% to 29% in March 2023.

However, an increase of mortgage rates is not always followed by a decrease in homeowner intentions to sell if the change was gradual. When mortgage rates rose from January to June 2023, more homeowners with mortgage rates above 5% said they intended to sell in the next 3 years. This high peak can likely be attributed to three things: (1) a lagged homeowner reaction to a slower increase of mortgage interest rates, (2) the hovering of rates around mid-6.00%, and/or (3) housing market seasonality, as households are more likely to plan moves during warmer months.

In contrast, September 2023, the lagged reaction of homeowners to mortgage rate increases caught up. The selling intentions of homeowners with rates above 5.00% decreased from 38% to 24%. Both the sustained quarter-over-quarter increase and the level of rates nearing 8.00%, an all time high in 23 years, are big drivers of this decrease in homeselling intentions.

Even though rates fell at the end of 2023, the gap in selling intentions shrunk.

At first glance, the closing of the gap between below and above 5% mortgages homeowners in December 2023 seems counterintuitive. After reaching a peak of 7.79% [2] at the end of October, rates started to fall significantly – in two months the average rate dropped to 6.61%. [3]However, this dramatic drop was not matched by a similar dramatic increase of selling intentions for those with rates above 5%, rather we saw the selling intentions of both groups of mortgaged homeowners converge.

Why was this the case? Though mortgage rates have declined, affordability in the housing market still lags due to stagnant home prices. Additionally, general economic uncertainty and industry layoffs still persisted at the end of 2023, meaning that higher-mortgaged homeowners might still remain financially cautious and hold off on selling and buying. Finally, lagged selling intentions could be due to homeowners’ lack of awareness of rate decreases. We saw record-high rates through October, but the decrease in rates coincided with the holiday seasons in November and December when homeowners are generally less focused on real estate news.

Still, overall selling intentions for all homeowners – both those with mortgages and those who own their home free and clear – were slightly higher in 2023 compared to past years. 21% of homeowners currently have their home listed for sale or are considering selling their home within the next three years. This is slightly up from earlier this year (19% in September 2023) and significantly up from last year (15% in December 2022).

[1] The percentage point differences across quarters from Q3 2022 – Q3 2023 have remained statistically insignificant

[2] Average 30yr FRM for the week of Oct 25 according to Freddie Mac

[3] Average 30yr FRM for the week of Dec 28 according to Freddie Mac

Methodology

This analysis uses data from the ZG Population Science Quarterly Survey of Homeowner Intentions and Preferences (QSHIP) using a repeated cross-sectional design. Homeowners 18 years of age and older who did not move within the last 12 months were eligible for participation.

This survey has been designed to allow us to measure within- and between-year change, and responses about mortgage rates have been collected since the third quarter of 2022. The most recent Q4 2023 survey was completed during December 2023 and included 4,218 homeowner respondents.

To achieve national representativeness, quotas for age, education, sex, region, race, and marital status limited oversampling of any given demographic group. In addition to using quotas for respondent sampling, ZG Population Science weighted the sample to the overall U.S. population using the U.S. Census Bureau 2022 Current Population Survey Annual Social and Economic Supplement (CPS ASEC) using these same characteristics.