Risk On, Risk Off: Large/Small Lenders Prioritize Different Borrower Profiles

In the wake of the Financial Crisis, there has been substantial speculation that lenders have become increasingly cautious in their mortgage lending – particularly large national lenders subject to additional regulatory scrutiny in the wake of the Dodd-Frank Wall Street Reform and Consumer Protection Law.

Some observers say large lenders are now more reluctant to quote riskier borrowers, leading to a divergence between the mortgage market for the safest borrowers, dominated by larger lenders, and the mortgage market for risky borrowers, dominated by smaller lenders.

There is, admittedly, no firm distinction between lenders potentially characterized as “small” as opposed to “large.” One option is to classify lenders based on the number of states where they are licensed to operate. Using this criteria and a fairly strict threshold, we classify “small” lenders as those licensed in up to two states. “Large” lenders, for our purposes, are licensed in 49 or more states.

Using this size classification between lenders and Zillow’s unique database of mortgage loan requests from borrowers and responses from lenders, we are able test these anecdotal assertions about recent trends in mortgage lending.[1] We compare small and large lender engagement of borrowers along two dimensions:

- The share of lenders who decline to provide quotes to certain types of borrowers

- The interest rate/annual percentage rate offered to certain types of borrowers

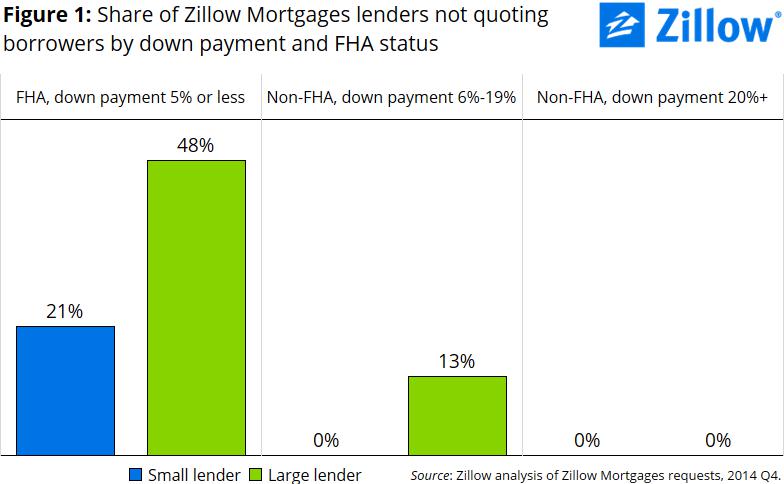

Down Payment

Since FHA loans with higher down payments are rare (and in many cases, do not make sense for all but those borrowers with the worst credit scores), we compare these borrowers to borrowers seeking non-FHA-insured loans with higher down payments. Within our sample of lenders on Zillow, all small lenders quote non-FHA loans with a down payment between 6 percent and 19 percent, and all small lenders also quote borrowers seeking non-FHA loans with a down payment of 20 percent or higher (figure 1). Among large lenders, 13 percent do not quote non-FHA loans with a down payment between 6 percent and 19 percent, while all large lenders quote non-FHA loans with a down payment of 20 percent or more.

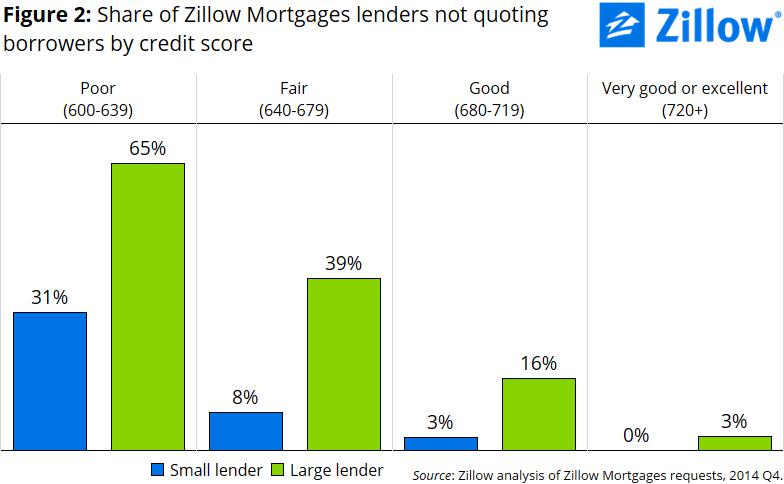

Credit Score

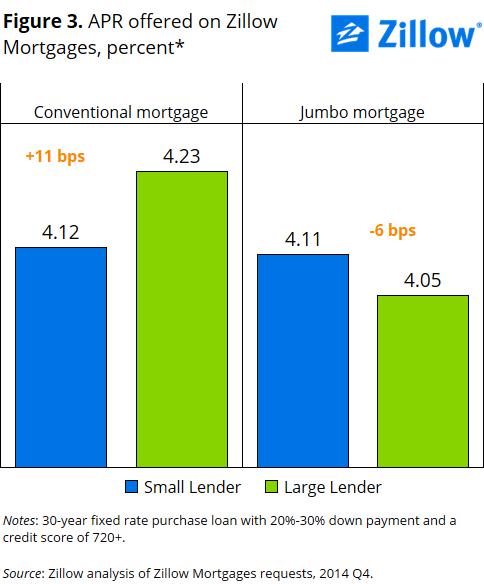

Jumbo Loans

When we compare the annual percentage rate (APR) offered to borrowers seeking 30-year, fixed-rate purchase loans with a 20 percent to 30 percent down payment and an excellent credit score (720 or higher), large lenders tended to offer high rates for non-jumbo loans – by more than 10 basis points – but slightly lower rates for jumbo loans – by about 6 basis points (figure 3).

Conclusion

The results presented above confirm many observers’ anecdotes – large lenders appear less likely to actively pursue riskier borrowers when measured by down payment and credit score, but appear very eager to attract high-quality jumbo borrowers. In some respects, this may be one of the great ironies of contemporary financial markets: The lenders most capable of bearing risk (in terms of diversification and analytic capacity) seem to be avoiding it, while the lenders who may be least capable of bearing risk seem to be most actively pursuing it.

Methodological Note

The data presented above are for 2014-Q4 and include purchase loans only. By our size classification described above, our data contain 71 small lenders and 31 large lenders.

[1] Zillow encourages all participating lenders to quote a wide range of borrowers, but each lender is able to prioritize their exposure to certain borrower segments.