The End of the Housing Market Deep Freeze: Why the Spring Home Buying Season Is Working Its Way Back Toward a New Normal

- Home purchase demand has partially rebounded since November lows

- New listings have only modestly recovered; and not enough to push inventory up

- Aspiring buyers are likely to face intensifying competition over the next few months, just like in a normal spring

Housing market observers could be forgiven for expecting a weak spring home buying season this year. The market cooled dramatically in the second half of 2022, after buyers ran into an affordability ceiling amid rising mortgage rates and two straight years of red-hot competition. Sales activity plunged, as existing home sales reached their lowest pace since 2010 in December, and home values slumped for the first time in almost that long.

But market conditions were quietly beginning to lay the groundwork for a New Year’s turnaround. After buyers began pulling back throughout the 2nd quarter, prospective sellers also stepped back from the bargaining table. The total flow of homes newly listed for sale in the second half of the year fell 20% from the year prior, from 2.4 million new listings to 1.9 million. The supply slowdown buffered the market from snowballing price declines, and prevented the runaway buildup of inventory back toward pre-pandemic levels. In fact, after rising from record lows last February, the weekly tally of active for-sale listings stopped growing in August, and ever since November has been tracking the same trajectory it followed in the winter of ‘20-’21. It is worth recalling that inventory levels that winter were the lowest on record, and when strong buyer demand materialized that spring, a red-hot buying season ensued. The current low-inventory environment is more attributable to anemic supply, but it will still contribute to shifting some negotiating power into sellers’ favor.

Buyers are coming back, after leaving in droves

o if reluctant sellers helped keep inventory from accumulating last year, what have buyers been up to lately? From July through October, they were clearly pausing their home search – our estimates suggest a 30% decline in the number of active home buyers. And winter is always the seasonal low point for home purchase activity, so teasing out a trend requires comparing to other years at the exact same time. Checking in on our most real-time measure of purchase activity, a weekly count of newly pending sales, we saw a turning point as early as mid-November. At its nadir, this metric was 41.1% below the same week one year prior. By the week ending February 4th, that year-over-year decline had shrunk to just -16.1%. [1]

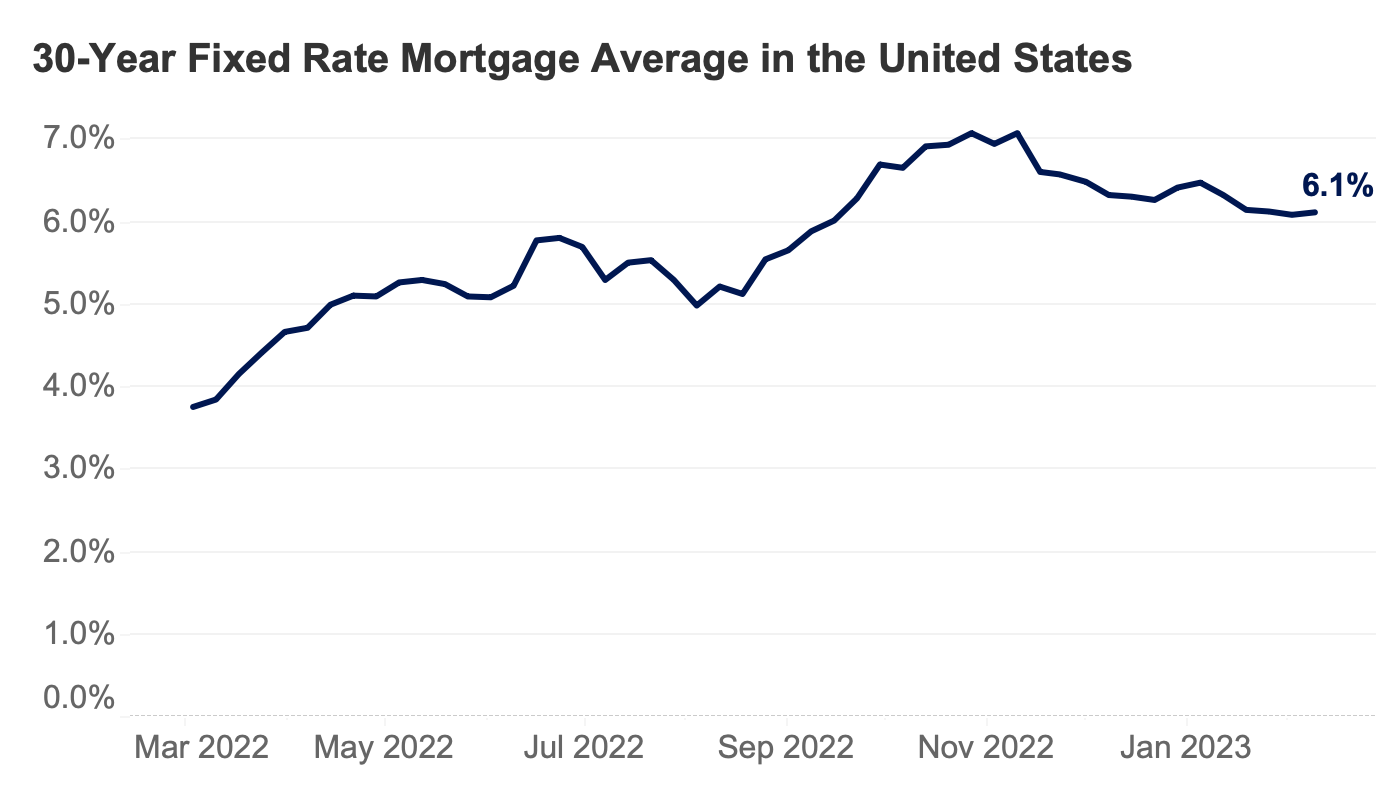

It’s not totally clear why buyers are coming back, but the timing of their return strongly suggests the influence of mortgage rates, which fell almost a full point from their peak of 7.08% on November 10, to 6.09% for a typical 30-year fixed-rate mortgage as of February 2nd. It’s still a far cry from the 3% range available to buyers in 2021, but that progress made a real difference in borrowing costs. Someone buying the typical-valued home at Halloween, with a 30-year loan at then-prevailing interest rates, would have required a mortgage payment of $1,764. That was 10% more than the $1,595 monthly cost on January 31, just 3 months later. Unfortunately for buyers, rates have quickly ticked back up over the last two weeks.

Spring 2023 will not be a repeat of spring in 2021 or 2022

While inventory is as low to start the year as 2021, and buyer demand (proxied by newly pending sales) is digging out from its November lows, we are still a far cry from the explosive conditions of early 2021 and 2022, when buyer demand was cresting at new heights, fueled by near-record-low mortgage rates, triggering bidding wars on most listings. Rather, this might be the market’s first steps toward a “new normal”– a world where inventory remains rather scarce by pre-pandemic standards, but buyers are not exactly swarming the doorway of every open house like in 2021 and early 2022. There is some faint evidence that sellers are coming back to the table – the flow of new listings was only down 16.7% year-over-year in January, after a 27.8% annual decline in December. But it will take more than that to truly bring balance back to the market, and more revived supply should help meet the returning demand, and head off the risk of renewed overheating.

In the meantime, what will this new normal look like for housing? Well-priced, well-marketed homes will get attractive offers their first weekend on the market; but many listings will take longer, and often require price cuts, to sell. [2] Buyers will mostly be motivated by the life transitions that have always triggered home purchases – new jobs, marriages, births – and less by FOMO, or the deal of a lifetime on mortgage rates. Home prices will neither be skyrocketing nor plunging, but hopefully moving on a slow, boring trajectory like they historically have, and a little higher in spring than in winter. Mortgage rates will no longer be setting new record lows, or rising at a near-record pace, but rather just somewhat high, and moving gradually downward. In fact, all the above conditions are already happening so far this year.

A trajectory is not a crystal ball

The housing market has moved along the above trajectory for the last couple of months, but that’s no guarantee it continues on this path. Inflation’s cooldown may stall out, leaving it stubbornly stuck above the Fed’s 2% target. The labor market might swing either way out of its recent Goldilocks track– tightening in concert with renewed inflation, or slumping toward recession. But from November through early February, the economic data has mostly been consistent with the much hoped-for soft landing: decelerating inflation without the pain of a recession.

Mortgage rates will affect both demand and supply significantly. If rates move lower, toward 6% or below, they will bring more buyers into the fold and also make it more palatable for homeowners to sell, increasing supply. If rates hover in the upper 6% range or above, buyers may once again put their house hunt on hold.

Within the housing market, the turnaround since November has coincided with the seasonally weakest 3 months of the year, so extrapolating is bound to be dicey. Will the unexpected demand by January’s very low standards translate proportionately to a strong spring shopping season? Only time will tell.

[1] Other widely-watched measures of real-time buyer demand, like the Mortgage Bankers Association’s purchase applications index, have not rebounded to the same extent. Their latest index data showed purchase applications still down 39% in the week ending January 27, from the same week last year.

[2] The median time on market was 31 days this January – right between the 42 days logged in January 2020, and the lightning-fast 17 days clocked in January 2021.