Inventory Finally Rebounds as Appreciation, Rent Growth Break Records (May 2021 Market Report)

**The inventory crunch showed early signs of easing in May, with for-sale inventory up 3.9% over April.

**Home appreciation broke new records and typical time on market fell to just six days.

**U.S. rent growth kicked into high gear, recording the largest monthly increase since 2015.

………………..

May brought a long-awaited bump in inventory nationwide, though it did little to immediately cool record-high home value appreciation, according to the May 2021 Zillow Market Report. Homes typically stayed on the market just six days before selling last month, and rents are rising quickly across the U.S.

Total U.S. for-sale inventory rose 3.9% in May from April, the first monthly uptick since July 2020 and only the fifth such gain recorded over the past 24 months. Inventory was up in May from April in 43 of the nation’s 50 largest markets (for which we have data). Still, inventory nationwide is down 31.2% from a year ago, the fourth straight month of 30%+ year-over-year national inventory declines. Inventory was up from a year ago in just three of the nation’s largest markets — San Jose (30.3%), San Francisco (25.6%) and Milwaukee (2.6%). Inventory in a fourth large market, Seattle, was only 0.4% below May 2020 levels.

But while the seasonal boost in inventory is a welcome sign that the ongoing inventory crunch may finally be starting to ease, it will take a while for the gains to immediately make an impact on a red-hot housing market in which demand for homes far exceeds the available supply of them. The typical U.S. home grew in value by 13.2% year-over-year in May, and was up 1.7% from April, to $287,148 — both record highs in Zillow data that dates to 1996. Annual growth was 10% or more in 46 of the nation’s 50 largest metros (again, for which we have data), led by Austin (30.5%), Phoenix (23.5%) and Salt Lake City (20.6%). Similarly, month-over-month growth accelerated in May from April in 47 of the 50 largest U.S. markets.

The combination of tight supply and high demand is doing more than just pushing home values up at a record pace — it is also helping push the amount of time homes spend on the market before selling to record lows. The typical time for a newly listed home to go under contract dropped to just six days nationwide in May, one day shorter than in April. At just three days, typical time on market is shortest in the hot Midwest metros of Cincinnati, Kansas City and Columbus.

After a year in which rent growth substantially slowed or even fell in much of the country, the nation’s rental market is also quickly bouncing back. Typical rents rose 2.3% in May from April to $1,747/month, the largest monthly appreciation since 2015, and were up 5.4% from a year ago. Rent appreciation is especially strong in the Inland West. Of the 100 largest U.S. metros, the top eight for annual rent growth are Boise, Phoenix, Spokane, Las Vegas, Riverside, Stockton, Fresno and Albuquerque — all with increases higher than 15%. The list of large markets where rent remains lower than a year ago includes the expensive coastal metros of San Francisco, San Jose, New York, Boston and Washington, D.C.

Looking Ahead

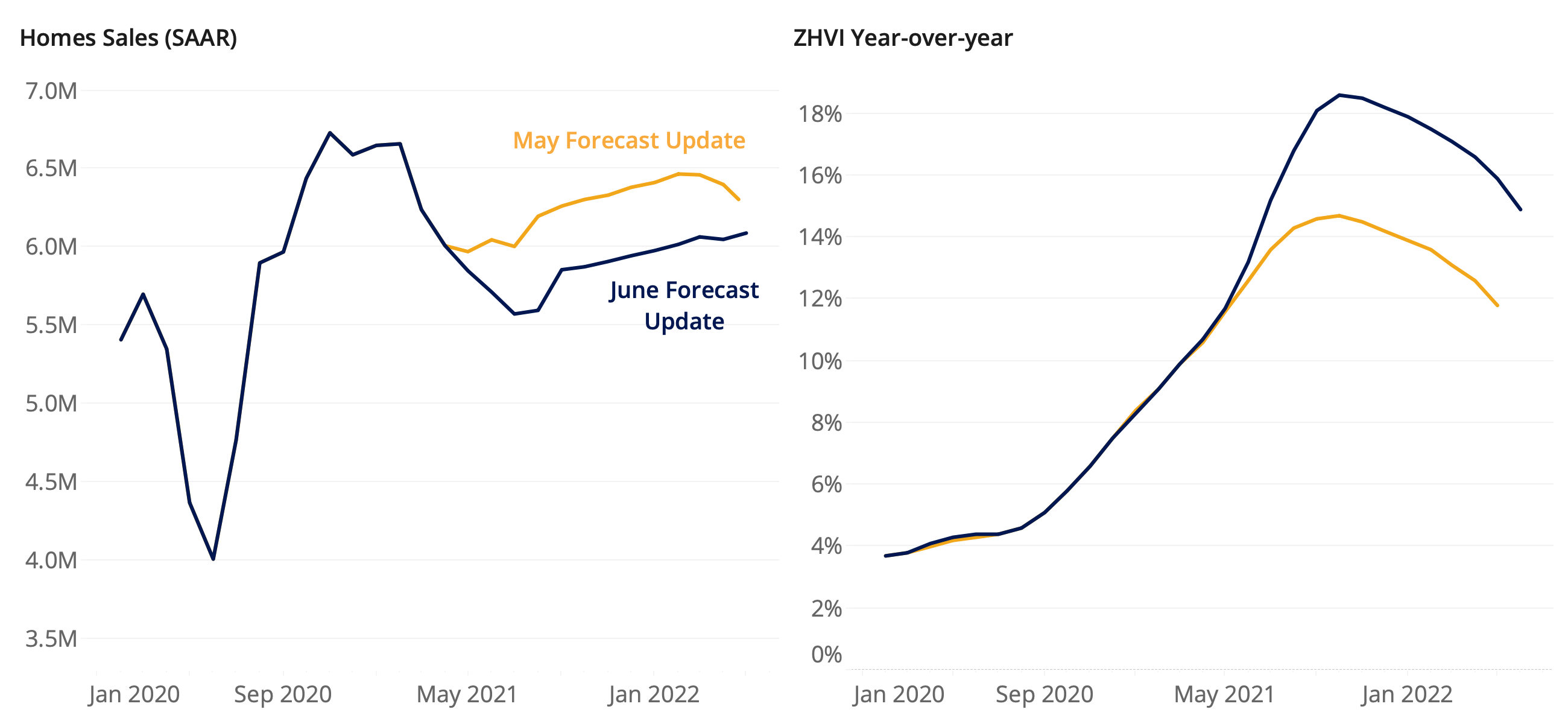

The rapid home price appreciation that has marked the past year in housing is not expected to let up any time soon, though affordability concerns and continued low inventory are putting somewhat of a damper on the outlook for sales, according to the latest Zillow home value and sales forecasts.

Zillow economists expect home values to increase 6.1% over the next quarter (May-August), by 17.9% through the end of this year (December 2020-December 2021) and by 14.9% through the twelve months ending in May 2022. The latest forecast is an upward revision from last month, when we predicted 11.4% year-over-year growth in April 2022. This month’s forecast was boosted, in part, by record short-term appreciation of the past few months, which shows virtually no signs of slowing as sky-high demand runs headlong into inadequate supply.

On the sales side, our forecast has been revised down somewhat, though we still expect that the number of existing homes sold in 2021 will ultimately exceed the number sold in 2020. The latest Zillow sales forecast calls for 1.64 million existing home sales in Q2 and a total of 5.91 million sales in 2021, up 4.8% from the 5.64 million total sales recorded in 2020 — which was itself the strongest year for existing home sales since 2006. Still, the full-year forecast is noticeably down from our prior forecast, which called for more than 6.2 million existing home sales this year. Pending sales figures and mortgage applications that have both fallen recently contributed to the lower outlook.

Ultimately, while demand for homes remains strong, limited supply is constraining sales activity — especially at lower price points, contributing to some affordability concerns. Even so, enduring demographic tailwinds, persistently low mortgage interest rates and an improving economy should continue to buoy demand, and recent signs of improved home seller sentiment suggest that some inventory relief could be on the way.