Homes in These 20 Metros Could be More Affordable by Year’s End

A year of small wins: Zillow economists project income gains will improve housing affordability in more cities.

Written by Grant Brissey on January 21, 2026

Reviewed by Kara Ng, Edited by Jessica Rapp

December 2025 market summary

- Median Home Price: $357,275 (+0.1% from last year, and +0.2% from a month earlier)

- Homes for Sale: 11.5% fewer active listings compared to a month ago

- Time on market for a typical home: 43 days, +10 days from a month earlier

- Average rate on a 30-year fixed (previous 28 days): 6.19% (as of Jan. 14, 2026), down slightly from the previous month

- Market balance: Still a neutral market nationally in December, and essentially flat from November — but a few metros cooled, including Milwaukee, Cleveland, and Detroit.

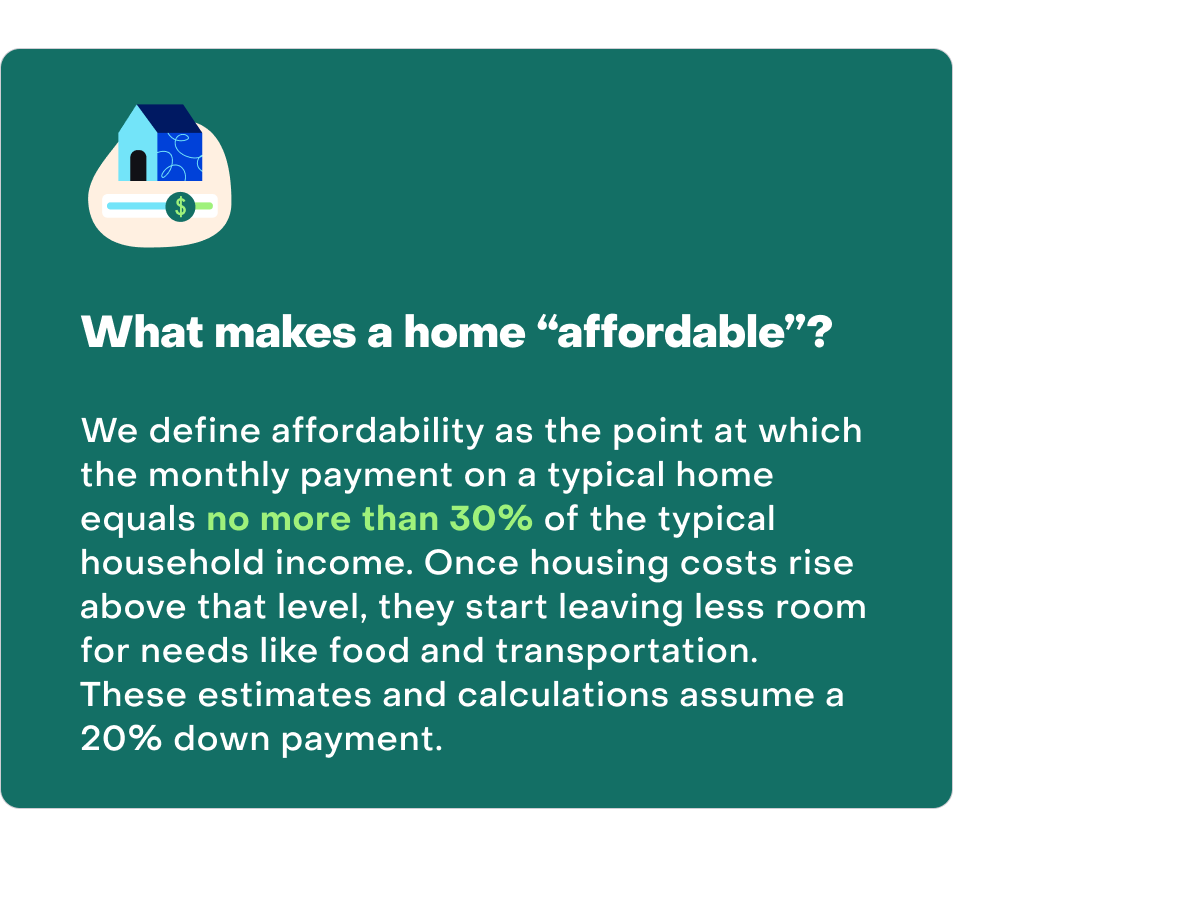

Zillow economists project affordability to improve this year in every major metro except Hartford (Zillow’s hottest housing market for 2026).

Projections see Chicago, Atlanta, and Raleigh crossing into affordable territory by December 2026. If so, they’ll join the growing list of markets where the share of median household income spent on the mortgage for a typical home doesn’t exceed 30%.

“What’s notable for buyers is that these affordability gains aren’t coming from falling prices — they’re coming from wage growth,” says Zillow Senior Economist Kara Ng. “Home values are still forecast to rise in 41 of the 50 largest metros.”

The projections show that buyers may get some relief this year as incomes grow faster than home prices. Still, a smoother path to buying will greatly depend on preparation — improving credit and exploring down payment assistance can make a real difference. Knowing what you can afford, through tools like BuyAbility, can help you move fast.

December: A three-year high in affordability

As 2025 wrapped, buyers saw a quieter market with more choices, fewer bidding wars, and slightly easier monthly payments. It’s a market that’s starting to give buyers room to breathe.

The typical mortgage payment fell 5.2% year over year, pushing affordability to a three-year high. Thanks in part to lowering interest rates, sales in December bumped up 1.9% from a year ago, but are still down over the month because of the slower holiday season.

In many markets, these trajectories should continue in 2026.

“This is what a small-wins year looks like for housing,” says Ng. “The slow and sustainable path — incomes rising, price growth staying in check and rates drifting lower — would allow buyers to regain footing while homeowners continue to build wealth.”

A brief history of affordability

2020-22: Despite low mortgage rates, prices soared in 2021 and affordability declined sharply by 2022, when mortgage rates doubled.

2023: Affordability reached all-time lows in October, when a typical mortgage required 38.5% of median household income. Homes in just seven of the nation’s 50 largest metros qualified as affordable at that time.

2024-25: Mortgage rates hovered around 6%–7% and prices stayed high. Affordability inched up as incomes rose, but owning a home still stretched budgets or remained out of reach for many.

2026: Nationally, a mortgage payment now takes 32.6% of median household income; the best affordability nationwide since August 2022. It’s on track to improve to 31.8% by the end of the year.

What to know if you’re planning to shop or list soon

In most markets, Buyers more likely to see negotiations — and in some cases concessions — than bidding wars, especially in markets where listings are lingering.

The biggest buyer advantage right now is choice. More homes are on the market than last year — up 8.9% from last December — even though December brought the usual seasonal slowdown.

“If you don’t like being forced into quick decisions, now can be a great time,” says Ng. “That said, real estate is still hyper-local. Well-priced, highly desirable homes can move quickly.”

Look into down payment assistance

Before you start touring homes, make sure your finances are sorted. The more prepared you are, the more options and confidence you’ll have. Consider checking into down payment assistance programs that can help ease upfront costs. The closer you can get to a full 20% down payment, the lower your monthly payment will be. If the down payment is the challenge, many lenders will accept as little as 3% down, depending on details like credit.

“Preparation doesn’t just make the process smoother — it can change the outcome,” said Ng. “Knowing your numbers ahead of time helps buyers compete without overreaching.”

Watch mortgage rates closely

Even small rate changes can quickly affect what you can afford. Zillow Home Loans’ BuyAbility tool tracks current rates so your search results stay aligned with the monthly payment you’re comfortable with.

Find homes in your budget with BuyAbility℠

Loading

LoadingRegional highlights

Some Midwest and Northeast markets are still seeing stronger price growth, while parts of the Sun Belt, Florida, Texas, and the West Coast are softer than a year ago. Here’s what to know about the markets poised to become affordable by the end of this year.

Chicago

Chicago is one of the few big metros with fewer homes for sale than last year, down about 6%. Still, the market has cooled from seller-friendly conditions into a more neutral balance, giving buyers and sellers roughly equal footing. The typical home is worth $333,786, up 3.8% from a year ago. Homes typically go from listed to pending in about 29 days.

Homes in Chicago

Atlanta

Buyers in Atlanta have more options than they did last year, with inventory up 11% year over year. That added choice has nudged the market closer to the buyer side of neutral. The typical home value is $374,117, down 2.8% from last year, and homes take about 63 days to go under contract — a slower, seasonally normal December pace.

Homes in Atlanta

Raleigh

Raleigh continues to stand out for how much its inventory has grown. Homes for sale are up 41% from last year, the largest jump among the nation’s 50 biggest metros. That surge has helped shift Raleigh from a seller’s market into a neutral one, giving buyers more room to shop and negotiate. The typical home is valued at $429,457, down 2.6% from a year ago, and homes go pending in about 53 days.

Homes in Raleigh

Zillow's affordable market forecast

| Metro area | Monthly mortgage cost (20% down) | Current share of income spent on mortgage (affordability) | Expected affordability by end of 2026 |

| Pittsburgh, PA | $1,519 | 22.30% | 21.40% |

| Birmingham, AL | $1,599 | 24.20% | 23.30% |

| St. Louis, MO | $1,841 | 25.90% | 25.20% |

| Detroit, MI | $1,739 | 26.10% | 25.50% |

| Oklahoma City, OK | $1,725 | 26.90% | 26.30% |

| Buffalo, NY | $1,675 | 26.60% | 26.30% |

| Louisville, KY | $1,759 | 27.20% | 26.40% |

| Indianapolis, IN | $1,874 | 27.00% | 26.60% |

| Memphis, TN | $1,647 | 27.70% | 26.90% |

| San Antonio, TX | $1,983 | 28.90% | 27.70% |

| Cleveland, OH | $1,723 | 28.10% | 27.70% |

| Cincinnati, OH | $2,034 | 28.60% | 28.10% |

| Baltimore, MD | $2,522 | 29.30% | 28.20% |

| Minneapolis, MN | $2,562 | 30.00% | 28.70% |

| Houston, TX | $2,119 | 29.80% | 28.80% |

| Kansas City, MO | $2,161 | 29.40% | 28.90% |

| Columbus, OH | $2,188 | 30.00% | 29.50% |

| Raleigh, NC | $2,719 | 30.40% | 29.60% |

| Chicago, IL | $2,404 | 30.40% | 29.70% |

| Atlanta, GA | $2,473 | 30.60% | 29.90% |

A local agent can help you stay competitive on a budget.

They’ll help you get an edge without stretching your finances.

Talk with a local agentRelated Articles

A local agent can help you stay competitive on a budget.

They’ll help you get an edge without stretching your finances.

Talk with a local agent