What Is a Home Appraisal?

Written by Alycia Lucio on December 6, 2022

A home appraisal is an estimate of a property’s value by a licensed appraiser. Whether you’re buying, selling or refinancing a home, an appraisal is typically an important part of the process because the results can affect your ability to receive a mortgage and finalize the home sale. Most lenders require a home appraisal to ensure you aren't borrowing more money than the property is worth. You’ll want the appraisal to come back either at the loan amount or higher in order to qualify for a mortgage. When buying a home, the appraisal will also let you know that you’re making a good investment.

Talk to a mortgage expert to learn more about getting pre-approved for a loan and any home appraisal requirements.

How does a home appraisal work?

In most instances a lender will request a home appraisal, and then a licensed appraiser will be assigned by an Appraisal Management Company (AMC). The AMC will ensure that the assigned appraiser can perform an independent and neutral assessment of a property’s value, without pressure from the lender, buyer, seller or other interested party. Once the appraiser is assigned, they will schedule a time to appraise the home, usually within 48 hours.

When appraising the home, the appraiser will complete a visual inspection of the home’s interior and exterior by walking the property and grounds. They’ll also drive around the neighborhood, research recently sold comparable homes nearby and analyze public record data. Then, they’ll compile a report on the home’s appraised value and share it with you and the lender. When buying a home, you’re not obligated to share the home appraisal report with the seller, but you are responsible for paying the appraisal fee.

Home appraisal process

Here is a step-by-step view of the home appraisal process:

- The lender orders an appraisal.

- The appraiser performs a property walkthrough and research.

- The appraiser shares a detailed report of the property’s valuation, based on their findings.

- A copy of the report is shared with you and the lender for review.

- You pay for the appraisal.

Home appraisal vs home inspection

While a home appraisal and home inspection are both important pre-closing steps, a home appraisal isn't the same as a home inspection. An appraisal is an evaluation of the home’s condition to determine its fair market value. A home inspection is an in-depth test of the home's major systems to make sure the property’s structure, electrical components and plumbing are functioning as they should.

An appraiser will visually inspect the property and grounds, and then research similar homes in the area to compare them. An inspector will physically check the interior and exterior of the home and flag any structural, construction or mechanical concerns to you.

What do appraisers look for in the home?

The appraiser will look at the property, grounds and condition of the home. They’ll note any visible flaws — like a roof issue or a cracked foundation. Then, they’ll compare the type of home, its size and condition to recently sold homes in the same area.

Appraisers aim to find at least three similar homes sold within the last 90 days, but in some circumstances multiple comparables aren’t available. Lenders must be flexible with the number of comps or amount of similarities. By putting the appraised property side-by-side with homes that have similar features, the appraiser can properly evaluate a home’s value, taking into consideration any home improvements that would make the home worth more or less.

Here is general list of what affects a home appraisal:

- Square footage of the home

- Number of bedrooms and bathrooms

- Age and condition of the home (newer homes are usually worth more)

- Construction materials used (energy efficient materials add value)

- Lot size and zoning restrictions

- Improvements made to permanent home fixtures (think roof, flooring, windows)

- Damage that may decrease a home’s value

- Additional amenities and special features

- Comps of recently sold homes in the area

- Location of the home and nearby amenities

- Current state of the local housing market

How do you read a home appraisal report?

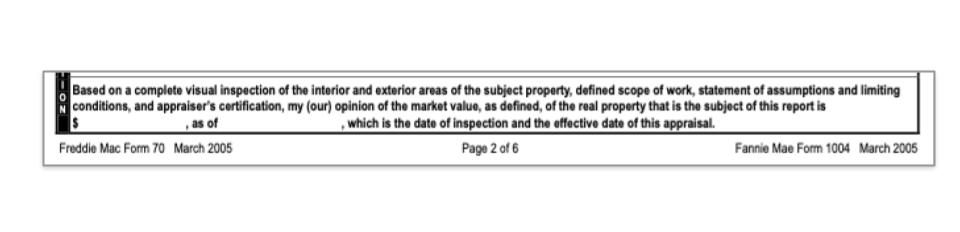

Most appraisers use a standardized report format known as a Uniform Residential Appraisal Report. This seven-page long report details the actions the appraiser took to complete the valuation and review the market conditions where the home is located.

When reviewing a home appraisal report, start on the first page by confirming the address and property details are correct. Then, at the bottom of page 2, you’ll see a box that shows the final appraised value.

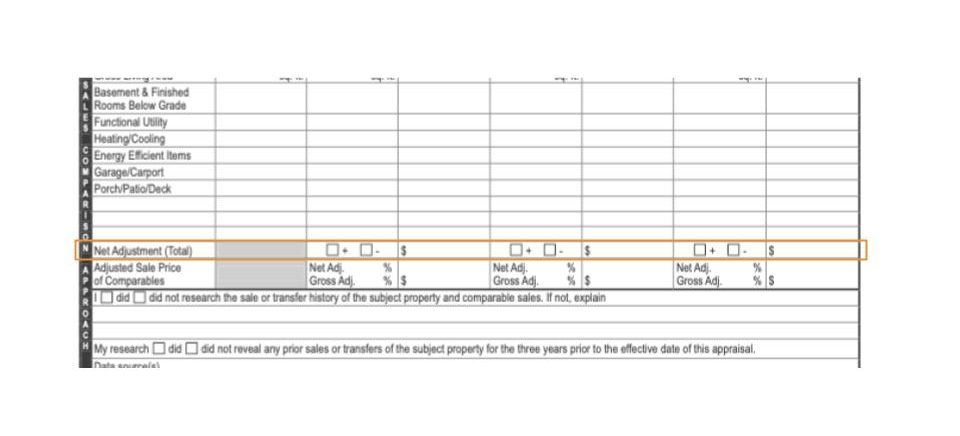

Continue through the report to see how the appraiser got to that final appraisal value. You’ll see columns with comparable sales and a line that says “net adjustment total.” This figure is how much the appraiser has adjusted the home’s value based on the comps. They may have also included photos.

What happens after an appraisal?

After the appraisal report is shared, you’ll have time to review it and make sure it’s free of errors. At the same time, the lender will determine your loan eligibility. If you think your appraisal is lower than it should be, you may be able to ask the lender if they’ll allow you to get a second opinion.

Here’s what comes next based on the results of the appraisal report.

Appraisal matches the offer: This is good news for the buyer and the seller. The lender will usually finalize the loan and you can proceed to closing at the agreed-upon sale price.

Appraisal is greater than the offer: This is even better news for the buyer. It means they’re getting a good deal on the home and should have some instant equity after closing.

Appraisal is lower than the offer: A low appraisal isn’t ideal, but there are a few things you can do. As a buyer, you can either renegotiate the sale price with the seller or make up the difference between the appraised value by increasing your down payment.

Home appraisal tips

I'm buying a home and need an appraisal

When you’re buying a home with a loan, you’ll need to include a financing contingency as part of your purchase offer. During the financing process your lender will require an appraisal of the property. This is a safeguard in case you stop paying your mortgage. The appraisal ensures the lender can sell the property for the amount of money you’re borrowing. As the buyer, you’ll also have peace of mind knowing you aren’t overpaying for the home.

The results of the appraisal can affect a loan approval. If the home appraises for more than the offer amount — great! You may get instant equity after closing. However, if the appraisal comes back low, you may have to make up the difference in cash or renegotiate the price with the seller in order to get your lender to fund your loan.

To prepare for the appraisal process, you might explore property estimates on Zillow, called Zestimates. These are based on our proprietary valuation model and available MLS and public records. The Zestimate is a helpful starting point, but it’s not equivalent to an official home appraisal. This is where your local agent can help explain the difference between the listing price, Zestimate and comparables (comparative market analysis). Each real estate market has its own dynamics that can affect your offer price, such as trends and bidding wars.

Here are a few tips that will set you up for success during the home appraisal process:

- Research recent comparable home sales in the area you’re looking to buy

- Hire a real estate agent who knows the area and understands market trends

- Include a financing contingency on your offer if you are using a loan to purchase, or an appraisal contingency as a cash buyer

- Review the appraisal report thoroughly for any errors you want to dispute

I’m selling my home, and the home is being appraised

Appraisals can be helpful tools for sellers. If you’re not sure how much you should list your house for, an appraisal can help you hone in on an appropriate price. Or perhaps you’re already in the process of selling your home and your buyer has included an appraisal contingency in the purchase contract. Either way, the condition of your home affects its appraised value. Put your best foot forward by following these tips:

- Keep a record of your home improvements and point them out to the appraiser

- Fix anything that’s broken

- Make sure the home and yard are clean

- Declutter the home

I’m refinancing, and the lender has ordered an appraisal

If you’re refinancing your home, your lender will likely want an appraisal for the same reason as when you bought it — to ensure the property is worth the amount you are financing. The only difference is that when you’re refinancing, the home appraisal will determine your loan-to-value (LTV) ratio, which can impact the interest rate that you receive. For example, if your LTV ratio is 75% or lower, meaning your loan balance is no more than 75% of the appraised value of your home, you could get a lower rate because the loan is seen as less risky to the lender.

Before the appraisal is performed, consider doing the following to have your home showing at its best for the potential to get the highest appraisal value possible.

- Ask a friend or family member to examine each room and point out areas that can be improved

- Declutter the home

- Make a list of any home upgrades or improvements you made and share it with the appraiser

FAQs about home appraisals

How much does a home appraisal cost?

The average appraisal costs about $400, but prices can vary based on your location and the size of the home. Appraisals may cost more if the property is somehow unique or on a large plot of land that needs to be surveyed to confirm property lines.

With non-purchase loans like a HELOC, the appraiser may not need to walk through the home and may instead perform a “drive-by appraisal”. This type of appraisal is less expensive and only used in cases where the home’s value is pretty certain.

How long does a home appraisal take?

The home appraisal appointment itself only takes about an hour. Your home appraisal report usually takes about a week to complete. Appraisal times may vary depending on the complexity of the property, the appraiser’s schedule and the type of loan. FHA loan appraisals and VA loan appraisals typically take a bit longer to complete than a conventional loan appraisal, because they require more documentation and often have minimum property requirements that need to be met.

Who pays for a home appraisal?

Even though the lender orders the appraisal, it’s the buyer’s responsibility to pay for it. Typically, you can pay for the appraisal at closing, but you may also have the option to pay at time of service.

What to do if an appraiser makes a mistake?

If you notice an error on your home appraisal report, notify your lender immediately. You may be able to get the mistake corrected or have a second appraisal done. If a second appraisal is needed, keep in mind you will most likely have to pay another appraisal fee.

How do appraisals affect your mortgage?

In order to assess the home’s market value and make sure the borrower isn’t attempting to borrow more money than the house is worth, all lenders order an appraisal during the mortgage process. When buying, a home appraisal can play a role in determining if your lender will approve your loan. When refinancing, a home appraisal will determine your LTV, which can affect the interest rate you receive.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedHow much home can you afford?

See what's in reach with low down payment options, no hidden fees and step-by-step guidance from us at

Zillow Home Loans.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Calculate your BuyAbility℠

Loading

LoadingRelated Articles

Get a mortgage with Zillow Home Loans

Go from dreaming to owning with low down payment options, competitive rates and no hidden fees. A dedicated loan officer will guide you until you have your keys in hand.

Zillow Home Loans, NMLS #10287. Equal Housing Lender.