How to Prepare to Buy a House

From reviewing your finances to making your wish list, here’s how to get your home-buying journey off to a strong start.

Written by May Ortega on March 11, 2026

Reviewed by Alycia Lucio, Edited by Jessica Rapp

We’ve all been there: scrolling through beautiful home listings late at night, daydreaming about a kitchen island or a backyard for the dog, and thinking, “I’ll own a home someday.” It’s easy to feel like being able to buy a home is always just out of reach.

But your “someday” can start today. Preparing to buy a home isn’t just about the day you get the keys; it’s about the small, confident steps you take right now, like organizing your credit and your budget early on.

If you’re preparing to buy a home and don't know where to start, this guide is broken out into individual, approachable tasks that you can take on one at a time.

Here is your roadmap to getting home:

1. Review your credit score

Your credit score is like your financial handshake; it tells lenders who you are. It’s the biggest factor in the interest rate you’ll get, which directly affects how much your monthly payment will be.

You can obtain your credit report for free. Give it a look. If the number isn't quite where you want it to be, don’t worry. Now is the perfect time to improve your credit. Focus on making on-time payments for credit cards and loans, and avoid any shiny new high-balance loans while you’re in your prepping-to-buy zone.

Here are some of the things that factor into your credit score:

- Payment history

- Total debt

- Length of credit history

- New credit

- Type of credit

Pro tip: If you're currently renting, you’re already making monthly payments, so why not get the (literal) credit for it? CreditClimb from Zillow reports your on-time rent payments to help you build or strengthen your credit history with Zillow's partner Esusu. There’s no hard credit pull to get started, or any hidden fees. Plus, late or missed payments are never reported. It’s all the upside with none of the worry.

2. Figure out your budget

Instead of guessing what you can afford, let’s get specific. Zillow Home Loans’ BuyAbilitySM tool gives you a personalized monthly payment estimate based on the important stuff: current interest rates, your credit profile, and your down payment plans. Once you know your number, you’ll see a “Within BuyAbility” tag on Zillow listings so you can fall in love with homes that actually fit your life.

Estimate your BuyAbility.

3. Prepare your finances

Lenders love to see stability, like consistent income and a low debt-to-income (DTI) ratio. To tidy up your finances, follow these steps:

- Keep things steady: Try to avoid switching jobs or moving to a commission-only role right before applying for a home loan.

- Watch your credit use: Keep those credit card balances low.

- Create a “hidden” fund: Start saving for more than just the home’s down payment. Closing costs are usually 2% to 5% of the price (and celebratory pizza also needs a budget)! There are ways you can shrink your closing costs, like negotiating with the seller and applying for first-time buyer assistance programs.

Pro tip: Use Zillow’s Closing Costs calculator to see what those fees might look like for you.

4. Gather information and advice

It’s perfectly fine to dream a little when thinking of what you want for your house. High ceilings, hardwood floors, a slide going from one floor to the other (it is dreaming, after all). But you’ll also want to figure out your non-negotiables, like a home office or proximity to coffee shops. It’s never too early to build your "must-have" list. Check out these questions for some inspiration.

If you aren't sure where to start your research, you can turn to Zillow’s NotebookLM. This is a personalized AI home-buying research assistant just for you, where you can get expert-backed answers on everything from finding the right agent to saving money. It’s a simple, conversational way to create a clear plan.

5. Choose a real estate agent

Your real estate agent is your home-buying pro and your primary advocate. You can connect with a local expert directly on Zillow. Don't be afraid to ask a lot of questions to help decide if an agent is a good fit.

A good agent should:

- Keep you informed about homes for sale in neighborhoods where you might want to live.

- Assist you with making an offer for a home you like.

- Help you with any issues that may come up during your transaction.

Pro tip: It’s up to you which you choose first: your real estate agent or your loan officer. Just know it’s a good idea to shop around for both.

6. Choose a mortgage loan officer

You don’t need to have a dozen documents and a pen in hand to talk to a loan officer. Think of this as an initial "get to know you" chat to help you choose the right lender. They can explain the technicals around getting your home purchase funded — without you needing to commit to a credit check just yet.

A loan officer can:

- Educate you about the loan application and approval process.

- Explain the down payment requirements for different loan programs.

- Update you on interest rate trends and how your payment may be affected.

- Help you figure out how much you can spend on buying a home.

- Give estimates of your closing costs.

Pro tip: Before starting a mortgage application, view current mortgage rates from Zillow Home Loans* to compare our rates against other lenders. At Zillow Home Loans, we’re transparent about our interest rates and APRs to help you find a home that fits your wants without going over budget.

7. Review your finances with your loan officer

Once you’ve picked a loan officer, have them do a deep dive into your finances. It’s better to find out you’re in great standing (or need a tiny bit more prep) now rather than when you’re mid-offer.

8. Get pre-qualified for a loan

A mortgage pre-qualification is basically your rough draft for a loan. Pre-qualification is a quick estimate of how much the bank will lend you, based on what you tell them about your income and debt. It’s a great way to see what price range you’re actually in. Note that this is not an official pre-approved mortgage.

What does pre-qualification entail? In most states, pre-qualification is based on your own submission of your income and assets, your estimated down payment, desired loan amount, and possibly a credit check, depending on the lender. It’s easy to check if you pre-qualify through Zillow Home Loans, where you can get your answer in five minutes.

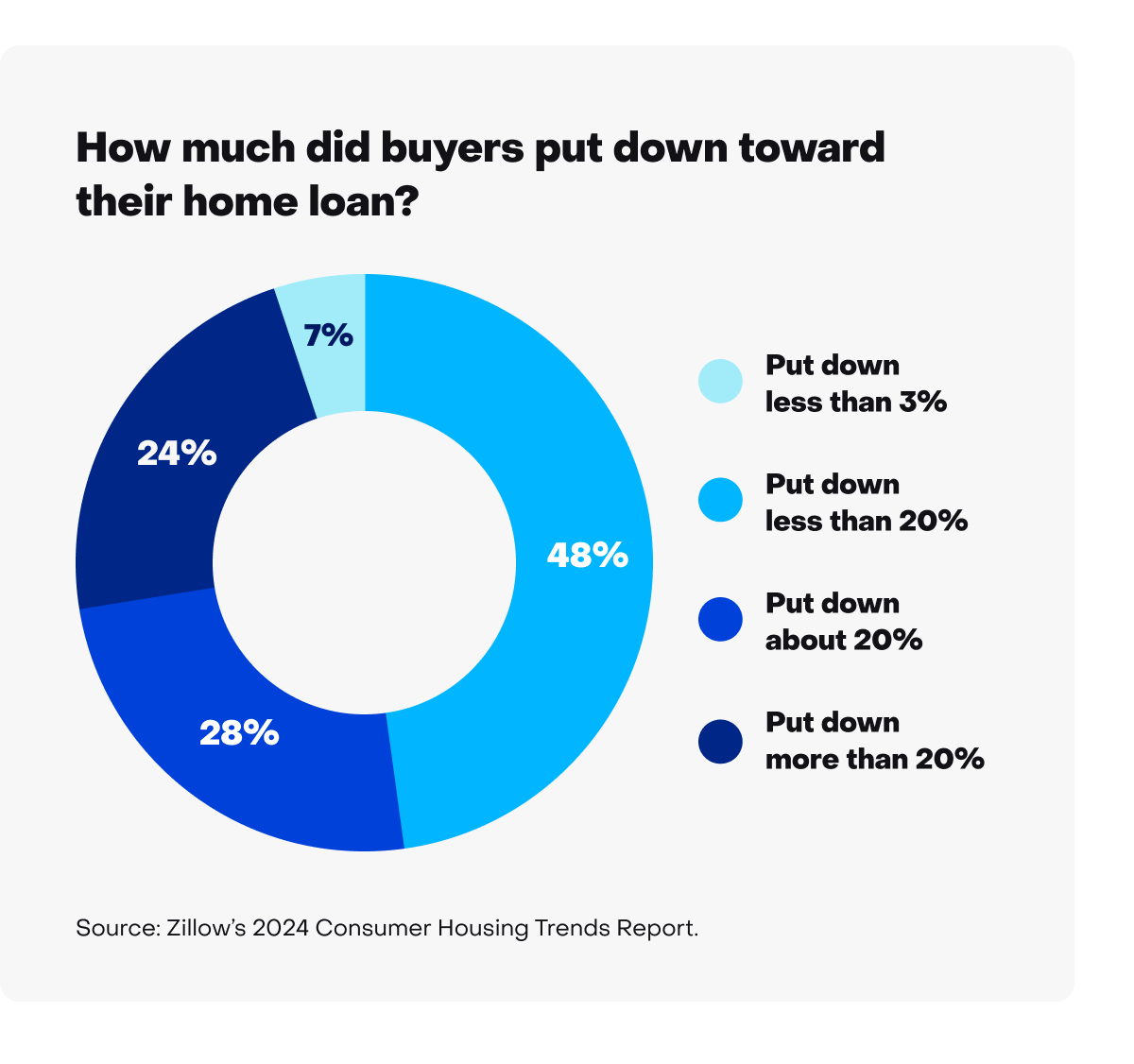

9. Identify funds for your down payment

Needing a 20% down payment on a house is a myth (though doing so can help you avoid paying private mortgage insurance). Lots of first-time home buyers get into homes with as little as 3% down. Whether you save up money, use a financial gift from family, or sell some stock, identify where your down payment money is coming from early. If saving up for a down payment is challenging, check if you qualify for down payment assistance.

10. Get pre-approved for a loan

Pre-approval is the real deal. This is where the lender verifies your income and assets. In today’s market, most agents won't even show you a home without a pre-approval letter — it tells sellers you’re serious about buying.

This is what you’ll need to get pre-approved for a loan:

- Two recent W-2s

- Two recent pay stubs

- Two months’ recent bank statements

- Proof that you have your down payment funds (in some cases)

A loan officer may ask self-employed borrowers to share their income tax returns.

Once you’re approved, the lender will send you a letter as proof.

Pro tip: If you’re planning to buy a home within the next 90 days, you should get pre-approved sooner than later. Most pre-approvals are valid for 90 days. Just know you can renew your pre-approval to restart this clock if needed.

It’s time to make your “someday” start today

Now you’re ready to begin your home-buying journey. Zillow Home Loans offers verified pre-approval. You can start online by answering a few questions about your housing goals and finances. Zillow Home Loans runs a soft credit check (it doesn’t affect your credit score), then guides you through securely uploading your income and asset documents. A loan officer reviews your information, answers any questions you may have, and confirms your borrowing power. Once that step is complete, you’ll receive a verified pre-approval letter that you can use when making offers.

By taking these steps, you’re not just preparing — you’re already on your way home. Someday is much closer than you think.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedA great agent makes all the difference

A local agent has the inside scoop on your market and can guide you through the buying process from start to finish.

Learn moreRelated Articles

Download the Zillow App

Don’t miss out on the right home for you — browse up-to-date listings, refine your search and more.

Download the free app