A Quick Guide to Buying Land

Written by Susan Kelleher on May 20, 2025

Do you crave the seclusion of country acres, a piece of land on which to park your tiny home or a buildable lot in the middle of the city? Buying land can offer a more affordable path to homeownership than buying an existing home if done with proper planning.

However, the process of buying land is different and often more difficult than buying an existing home. Knowing how to buy land can help you determine whether it could be the right path for you. Here are questions to consider before making any decisions, and a seven-step guide to the entire purchase.

How will the zoning rules affect your long-term plans for the property?

Zoning information is critical in determining whether you’ll be allowed to build what you want on the property. Every piece of land is zoned or classified for a specific use: residential, agricultural or commercial. Local counties or cities establish the zones and the rules about what they will allow in those zones. Many cities and counties make these rules and zoning maps available online for public access.

Beyond your specific piece of land, or "parcel", you’ll also want to consider the immediate area and any plans that could affect the value of the property or your ability to enjoy it. You can find that information in the county or city’s “general use” plan.” This spells out plans for the area over the next 5, 10 or 15 years.

For example, suppose you want to build a home on a quiet parcel in a rural area. The planning document can tell you whether there are future plans in that area for a landfill, power plant, commercial zone or new road nearby that could influence whether you want to live there.

Staff at the government agencies responsible for zoning are well-versed in the details of the plans and can answer any questions you have. No one expects you to be an expert, so reach out to them if you need help deciphering the plans.

Are there deed restrictions on how you can use the land?

A deed is the legal document that transfers ownership of a property. It includes a description of the property, along with any restrictions on what you can build or how you use the land. Deed restrictions are found most often in communities governed by a homeowners’ association (HOA). You’ll need to follow the restrictions in addition to whatever zoning rules apply.

Some common deed restrictions imposed by HOAs include:

- limits on vehicles and where they’re parked

- fences

- types of pets

- types of home-based businesses

- the amount of time you’re allowed to live in an RV during the year

If you are planning to purchase land in an area governed by an HOA, ask the association for a copy of its Covenants, Conditions and Restrictions (CC&Rs), which spell out the restrictions. Read it carefully. If you have any questions about the CC&Rs or if there is no HOA to obtain them from, consult a real estate lawyer for more information. A real estate lawyer can assist in obtaining this information through a title search.

Can you build on the land?

It may seem like an obvious question, but there are numerous additional factors that can foil your plans for building on a piece of land. Contact your county or city planning department to gather information about the parcel you’re considering. Questions to consider include:

Is the land prone to hazards or in a flood zone?

Could landslides be a concern? If the area has a flood designation, this could require flood insurance, which can cost hundreds of dollars a year.

What is the land’s topography?

Flat parcels are the cheapest to build on. If you have to move a lot of dirt and trees to create a building pad, it’s going to cost more to build. You'll also want to consider whether the land contains wetlands or other environmentally sensitive areas.

How close to the property line can you build?

Local governments impose building restrictions called setbacks on property that will affect where you can build on the land. A setback creates a buffer zone; it establishes a minimum distance between the home you want to build and a curb, property line or other structure. Setbacks, which contribute to safety, aesthetics and privacy, differ depending on locale. Take the property setbacks into account when determining whether there is a large enough building space for your home in the area you want to build.

Is the soil suitable for building?

A simple soil test or geotechnical investigation can determine how much weight the soil can handle. This is critical information that will tell you whether the ground is strong enough to support a foundation. It can be required before you can get a permit to build on the land.

If you’re planning to farm the land or suspect there’s some contamination, a soil test can provide that information, too. And if you’re in a rural area with no sewer connections, a percolation or perc test can tell you whether the soil has suitable drainage for a septic system.

Consider adding contingencies when buying land

If you’re going to make an offer, you should consider adding contingencies that will give you time to investigate whether you’ll be able to use the land the way you intend. Among the more common contingencies:

- zoning

- septic system viability

- a survey showing easements and property lines

- environmental tests if warranted

Having contingencies can allow you to walk away without losing your earnest money if the limitations on the land conflict with your plans.

Are you buying land with easy access?

How will you get to the property? If it’s on a main public road, you’ll likely have no problem.

Often, especially in rural areas, the only access to a piece of land is over someone else’s property. Without what is known as an “easement,” your property is considered landlocked.

Ensure that a right-of-way easement — essentially a right of passage — is granted, in writing, before you agree to buy the land. Otherwise, you won’t be able to access it by land, which could diminish its use and value.

A potentially fast way to find easement information is to check the plat map for the property. A copy of the plat map, which also shows the property boundaries and measurements, can be found at the county or city clerk or recorder’s office. However, plat maps and recorded easements can be confusing and complicated to understand, so speaking to an attorney or other professional in this area is highly recommended.

If there is no existing road to the property, you’ll need to factor the cost of building one into the purchase price.

Are there utilities on the property or will you have to install them?

In larger planned developments, the builder generally brings utilities, such as water, sewer, natural gas and electricity, to the lots.

In rural areas, however, buyers may need to go to greater lengths to connect to utilities. That could involve drilling a well, installing a septic system or digging trenches to connect with electricity or water. All are likely to be costly projects. Off-grid technologies can open up possibilities for power, water and waste disposal, but the cost and viability of those options should be considered.

Does your parcel have internet access?

Internet access also could be a major issue for people who need high speeds — or reliable access — for work-from-home situations. There are increasing numbers of work-around solutions, including accessing the internet via cellular service providers. However, home connection to an established provider tends to offer the most reliable service.

Get bids or estimates on any work that needs to be performed before you sign a purchase agreement, or have your real estate agent make your agreement contingent upon your acceptance of the bids or other due diligence investigation.

How will you purchase the land?

Not all lenders handle vacant land loans, so it may be a bit of a challenge to finance your purchase. The owners of raw land — which is land without any utilities, sewers, or streets — may offer seller financing when they’re selling it. If not, try local banks or credit unions.

People can buy raw land with no intention of building on it. Raw land lenders set their own qualifications and LTV guidelines that establish the level of risk they’re willing to assume on a particular loan. Higher risk loans tend to come with higher interest rates.

But if you're buying land with the intention to build on it, there are a few things to keep in mind.

Buying land to build a home

If you intend to buy land and then build a home on it or buy a modular/manufactured home, it’s best to determine if you can qualify for a construction-to-permanent loan first. Once the home is near completion, you can start searching for a traditional mortgage to refinance your construction loan.

If you’re seeking financing in this way, consider the costs involved in developing the land when applying for a loan. The costs can include tree removal, grading, drainage and creating an access road, as well as bringing utilities to the site and building a structure. Get bids or estimates for all the work required before seeking financing so you’ll know how much you need and what type of financing to apply for.

Buying land with utilities

If you‘re buying a piece of land that already has utilities on it, and plan to live on it in an RV or tiny home, the financing is likely to be straightforward. But if you’re planning to build, you may be required to have building plans in hand in order to apply for a construction-to-permanent (CP) or combined construction loan to finance the purchase of the land and the building of your home.

Buying land with cash

If you’re paying cash for the land, it may be possible to obtain a construction loan later to build on the land using your equity in the land as a down payment.

As you can see, buying land has a lot of similarities to the process of buying an existing home, but requires an extra level of diligence to make sure you're buying the right land for your goals. It is really important to find a lender or advisor you trust and who can help guide you through all of the intricacies of the financing process for vacant land, especially if multiple loan products are necessary to achieve your goals.

How to buy land

If you’re just exploring ways to buy land and aren’t ready to engage a professional, start by crowdsourcing some information. Seek out online forums for people who have already gone through the process, or talk to a local builder to see what might be involved. And spend some time searching for what’s available in your desired area.

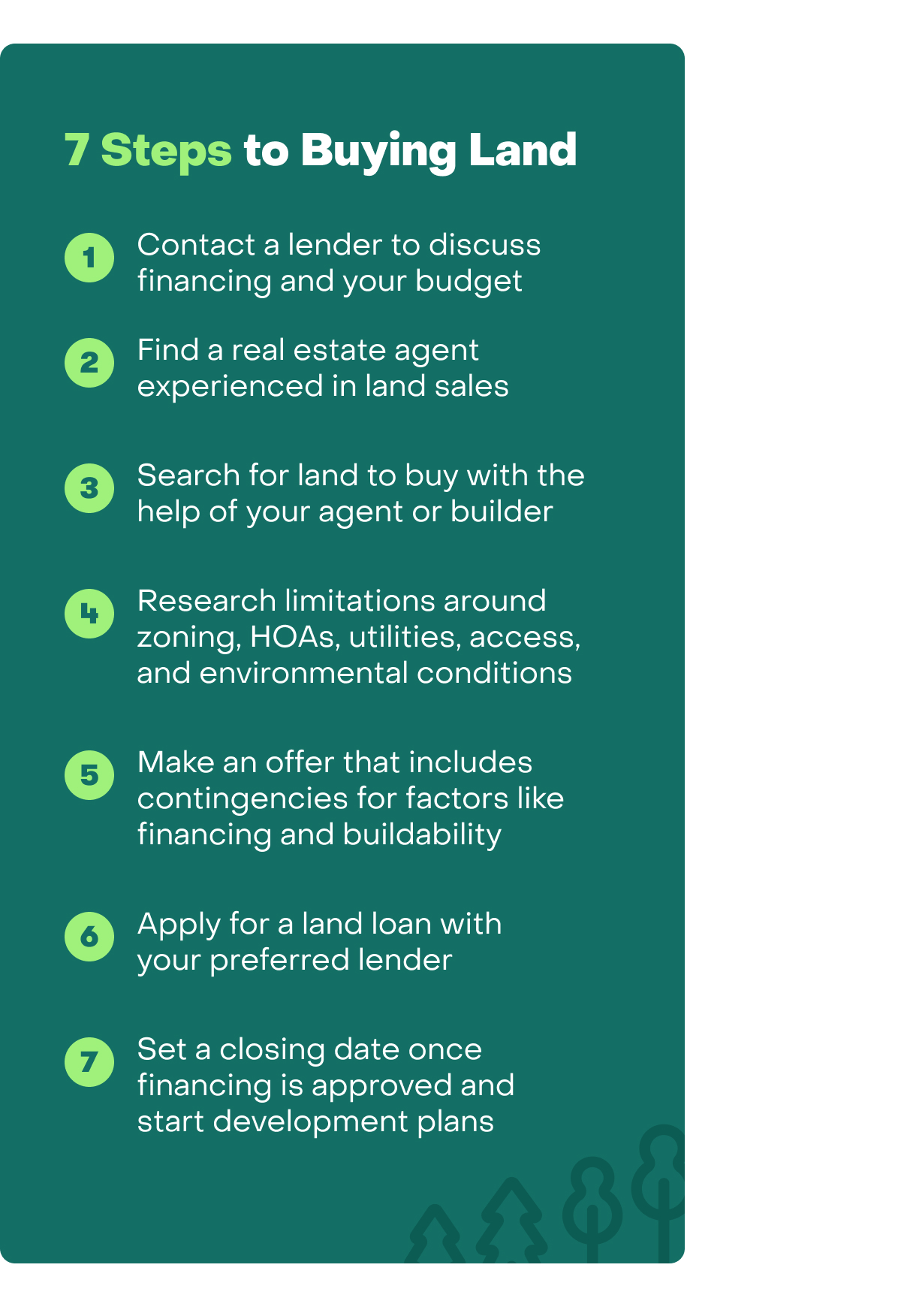

The process of buying land generally mirrors the process of buying a home and is likely to include the following steps:

Contact a lender

If you plan to finance the purchase of land, work with a lender to discuss options. This pre-qualifying discussion will help you understand your budget for land. Your lender will walk you through several, possible financing solutions including a land loan, USDA loan, SBA 504 loan (for business use) or a home equity loan.

Hire a real estate agent experienced in buying land

The process of buying land usually begins with an experienced agent. Look for a professional who is familiar with the area and who has experience in land sales. Some agents who have taken special training in land sales will advertise themselves as an accredited land consultant. You can start by compare agent reviews on Zillow’s Find an Agent tool.

While it’s possible to do the legwork yourself, a local builder also can help you decide whether a plot is suitable for development and help through the process of developing it.

Shop for land

In addition to working with your agent or builder to identify property, expand your search to include local newspapers, online classified advertising, websites that specialize in land and even an in-person search of the area to look for for-sale signs, especially in rural areas.

Research the parcel

Consider whether you’ll be able to build the home you want, and whether you can do so within your budget. Some of things to consider include zoning, setbacks, legal access to the land, the availability of utilities, any HOA restrictions and environmental and soil limitations. Reaching out to professionals like lawyers, inspectors, surveyors, and contractors to help navigate all of this information is highly recommended and can make this process a lot easier.

Submit a land purchase offer

If you have an agent, you’ll work with them to craft an offer. Some of the contingencies to consider: financing, including a property appraisal, title search to ensure there are no liens or other owners, buildability as determined by soil tests, setbacks and zoning. Be sure the offer gives you enough time to investigate the issues so you don’t get locked into a contract on a piece of land that you can’t build on.

Apply for a loan for buying land

If you like the lender you’re working with, formally apply for a loan now that you know the cost of the property. Your lender will verify your income, assets and debts as part of its underwriting or risk assessment process for the loan.

Close on your land purchase

Once your financing has been approved, your lender will set a day for closing, which is when the sale is finalized. You should have homeowners insurance in place, even if it’s just liability insurance.

Once you’ve closed, the land is yours.

Tags

A local agent can help you stay competitive on a budget.

They’ll help you get an edge without stretching your finances.

Talk with a local agentRelated Articles

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualified