What Is a Manufactured House?

For one, it’s one of the most affordable home types in America. But buying one comes with special considerations.

Written by Susan Kelleher on May 25, 2022

First-time homebuyers could increase their chances of landing a home by broadening their search to include all home types, including one of the most affordable home types in America: a manufactured home. Manufactured houses have evolved from their early days as “mobile homes” into permanent structures that you can customize for any taste for a fraction of what it would cost to buy a typical single-family home. But what exactly is a manufactured house, and what are the pros and cons for first-time home buyers considering buying one?

What is a manufactured house?

A manufactured home is a completely factory-built house that is constructed according to national standards set by the federal government. The home sits atop a chassis or frame that allows for delivery by truck to a home site. Homes that meet the federal standard come with a certification label.

Before the federal standards were adopted, manufactured homes were called mobile homes because they were made to be moved from place to place. Today, homeowners place a manufactured home on a permanent foundation.

The mode of delivery largely dictates the rectangular shape of a manufactured home. They’re long and thin so they can fit on a truck bed for transport. They come in two primary configurations: single-wide, which is one rectangular unit, and double-wide, which consists of two units that are joined together after they’re delivered.

How large are manufactured homes and what materials are they made of?

Manufactured houses can be spacious and come in a variety of floor plans. Single-wide homes are usually 14-18 feet wide and 50-80 feet long. A double-wide home can be twice that size since it consists of two single-wide sections that are transported separately and joined together at the home site. It’s common for a double-wide to have three bedrooms and two baths.

In 2020, the typical size of a manufactured home was 1,134 square feet for a single-wide home, and 1,677 for a double-wide home, according to the U.S. Census Bureau.

Manufactured homes consist of the same materials as homes constructed at a building site. They can be customized in a variety of styles and finishes.

How much does a manufactured home cost?

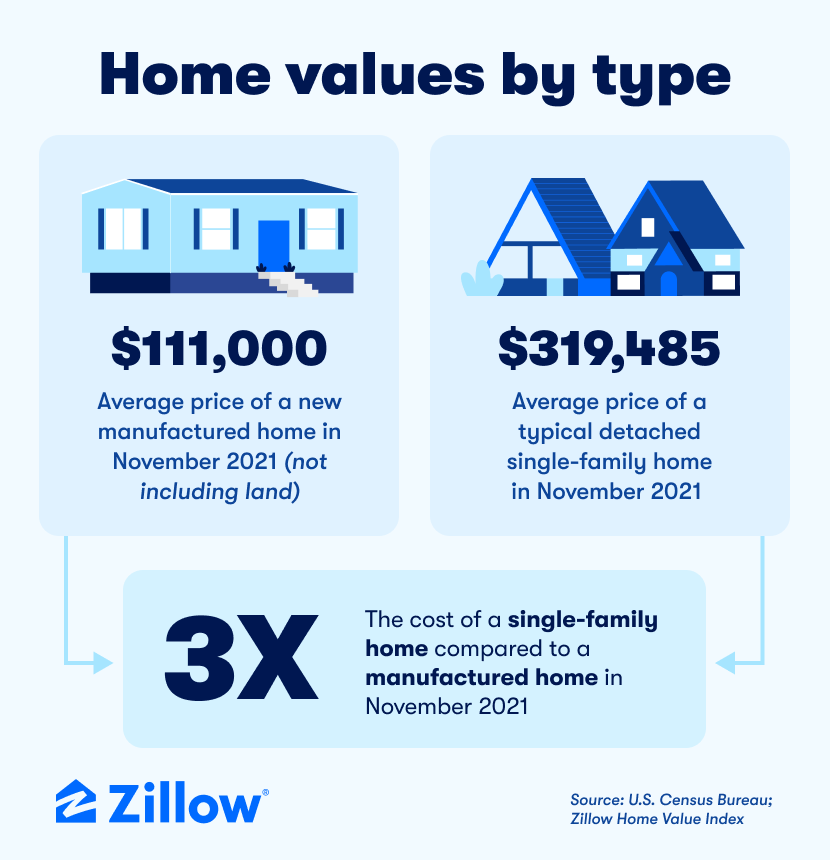

The average price of a new manufactured home in the U.S. was $111,000 in November 2021, according to the census bureau. Single-wides came in at an average price of $76,400 while the average price of a double-wide was $139,900. The typical detached single-family home was worth $319,485 during that same period, according to Zillow’s Home Value Index.

In a recent Zillow survey, the typical mobile or manufactured home buyer said they paid $45,000 for their home between 2019 and 2021. That price, as reported by buyers in the survey, is five times cheaper than the $225,000 buyers said they paid for a traditional single-family detached home over the same period.*

What’s the difference between a manufactured home and a modular home?

The biggest difference is the standards builders follow.

Manufactured homes are built to standards established by the United States Department of Housing and Urban Development. Modular homes are built to the same state, local or regional building codes that apply to site-built homes, and require a building permit.

Manufactured home builders construct them entirely at a factory before they transport them to a site and place them on a foundation.

Meanwhile, builders construct about 70% of modular homes in a factory. Then, they transport the various components or modules in pieces and assemble them like building blocks at the site. Modular homes also tend to be larger than manufactured homes. Additionally, they have varied profiles and shapes and often include garages, second stories and covered porches.

How can I buy a manufactured home?

Your real estate agent can help you find manufactured homes that are listed for sale on Zillow — both those being sold in rental communities and those that come with land. Remember that only manufactured homes built after 1976 meet federal standards for safety and durability.

You can shop for new manufactured houses and pre-owned models at retailers or dealerships. You can tour models on a lot much like you were shopping for a car, and explore options for customizing and financing. Sellers also list manufactured homes for resale — and sometimes give them away — on online community forums.

Manufacturers’ websites can give you a good idea of the styles and availability in your state. See a model you like? The manufacturer can help you locate a retailer who can arrange for delivery and set up.

If you’re planning to bring a manufactured home to land that you plan to buy, it’s highly recommended that you find the land first. Owning the land can help you get the most favorable loan terms. It can also provide greater stability over your monthly housing costs.

Local zoning regulations will determine how you can develop the land and whether it’s large enough to accommodate your house. Your real estate agent can help ensure you’re paying a reasonable price for land that can be developed in the way you envision.

What are my options for financing if I buy a manufactured home?

You can finance the purchase of a manufactured home with a traditional mortgage, including a federally backed loan, but only if you own the land where the home will be placed and only if the home comes with a red metal certification label. Without land, lenders consider the home personal property, similar to a car. Lenders typically charge a higher interest rate for a personal or “chattel loan” if you qualify for one.

Buying a home to put on rental land, such as a manufactured home community or park, can provide you with a comfortable home and relative stability in your housing costs, but you will not be protected by foreclosure laws that safeguard homeowners who own their land.

According to the federal Consumer Financial Protection Bureau, more than 60% of manufactured housing borrowers own the land where their home is located.

Without land, lenders consider the home personal property, similar to a car. Lenders typically charge a higher interest rate for a personal or “chattel loan” if you qualify for one.

Sources of financing include the manufacturer, credit unions or specialty lenders. Lenders who specialize in manufactured home financing each have their own rules and standards. The federal Department of Housing and Urban Development maintains a list of lenders who offer federally insured loans for manufactured homes.

Take time to shop for the best interest rate and terms. Don’t sign anything unless you understand exactly what you’re signing up for. A HUD-approved counseling agency can provide guidance, as can your agent.

Can I get help from a down payment assistance program?

Maybe. The federal Department of Housing and Urban Development has a list of states that provide down payment assistance. Check to see whether your state helps buyers of manufactured homes and/or the land it will ultimately occupy.

Pros and cons of manufactured homes

Pros

Cost. The typical manufactured home is far less expensive than traditional single-family homes that are built on-site.

Ability to customize. A large variety of styles and finishes are available for customizing your home.

More control over your environment. If you own or are buying the land on which the home will sit, you can position the home and plan the site in a way that suits you.

Lower down payment costs. Because manufactured homes cost less, your down payment is likely to be smaller than if you were buying a traditional single-family home.

Build equity sooner. If you own the land on which your home sits, the lower price point can allow you to get into a home and start building equity sooner. Zillow research shows that from March 2021 to March 2022, the typical listing price on a manufactured home rose 33%.

Cons

Reputation with consumers. Despite improvements in design, safety and durability, manufactured homes still carry some of the baggage associated with their mobile home predecessors.

Learning curve. The best financing is available to buyers who are putting a home on land they own. That requires knowledge of financing, land purchase/development and the home itself. If you’re buying for the first time, it can be a lot to manage.

Uncertainty. If you’re buying a manufactured home situated in a community of manufactured homes park, you’ll be paying rent to the owner. Corporate ownership of mobile home parks has increased across the country in recent years, which has driven up rents. An unexpected park closure could force you to move your home or sell it.

Loan repayment may be shorter. Loans to purchase a manufactured home can come with shorter repayment terms.

Location. Most of the nation’s manufactured homes are in the South. They’re also an attractive option for people in rural and remote areas where building is difficult. If you want to live in a city, you’ll be paying a premium to buy a lot. You could also face difficulty finding rental land in urban areas.

It’s recommended you seek out a knowledgeable agent to help you decide whether a manufactured home is right for you.

More resources

Now that you know what a manufactured house is, here are definitions for 20 other types of homes.

Learn more about additional alternatives to conventional home ownership.

* The median price reported by buyers differs from the Zillow Home Value Index (ZHVI). The ZHVI includes only those homes for sale on the open market. It does not include off-market sales, such as sales between family or friends.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedA great agent makes all the difference

A local agent has the inside scoop on your market and can guide you through the buying process from start to finish.

Learn moreRelated Articles

Download the Zillow App

Don’t miss out on the right home for you — browse up-to-date listings, refine your search and more.

Download the free app