What Is APR?

The Annual Percentage Rate, or APR, reflects the true cost of the loan. Find out why it's important and see why having a higher APR might be better for you.

Written by Tali Bendzak on May 13, 2022

APR stands for annual percentage rate, and it’s the price you pay for borrowing a sum of money from a bank or lender. The percentage represents the yearly cost of the loan. You’ll see the term APR whenever you apply for a credit card, mortgage, car loan, student loan or any other type of loan.

When you see a great APR advertised, it’s usually the lowest rate available. Your actual annual percentage rate may vary based on your credit score, repayment history, the level of risk to the lender and other factors. Knowing the APR up front can help you make a more informed decision when comparing credit options to see who is offering the best interest rate and lowest fees.

How does APR work?

When you borrow money from a bank or lender, you have to pay interest and other fees on the money you borrow. Your APR is the total of those costs expressed as a percentage of your loan or credit card balance for the year. You’ll pay the APR in addition to the balance until you’ve fully paid off the debt. On a credit card, APR is usually the same as the interest rate. On a mortgage or other type of loan, APR is the interest rate plus any upfront or annual fees and costs associated with the loan. Credit card APRs are almost always higher than other types of loans, but you can avoid costly interest charges if you pay off your balance in full each month by the due date.

What does APR include?

On a mortgage, your APR includes the interest rate plus any upfront costs the lender charges for processing, approving and providing the loan, in addition to annual costs like mortgage insurance. Not all lenders charge the same fees, so be sure to ask your lender for an itemized list of fees up front.

Some of the most common fees in the APR include:

- Loan origination charges, which can include pre-qualification, underwriting fees, administrative fees and processing fees

- Mortgage insurance, depending on the size of your down payment

- Discount points (an optional fee paid at closing to lower your interest rate)

Some lenders may require you to make monthly payments to an escrow account to cover your property tax and homeowners insurance premiums. These costs don’t impact the rate you receive and are not calculated into your APR.

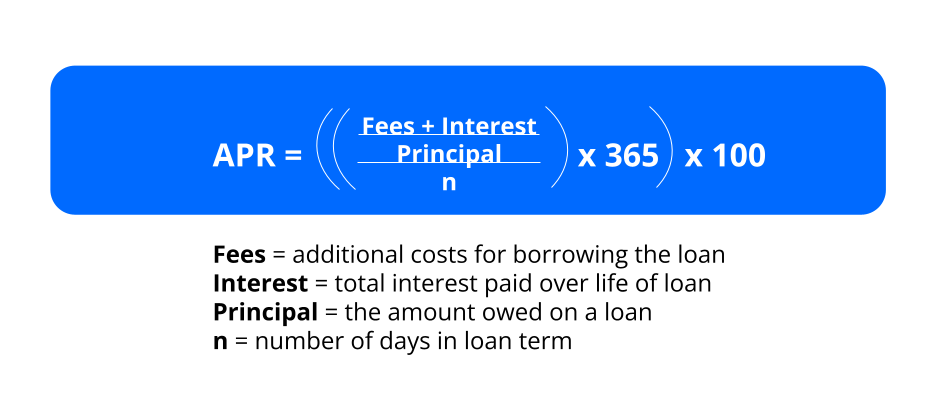

How is APR calculated?

All lenders must disclose how they calculate your APR, thanks to the Truth in Lending Act (TILA), making APR a good way to compare borrowing costs. Banks and lenders use an APR formula that looks like the one below to calculate the amount of interest owed on your outstanding balance:

Lenders will do the math for you, but if you’d like to estimate APR on your own, follow these steps:

Step 1: Add your interest rate and upfront fees

Step 2: Divide the amount you owe (principal)

Step 3: Divide the total number of days you have to repay the principal

Step 4: Multiply by 365 (number of days in a year)

Step 5: Multiply by 100 to convert to a percentage

How to calculate monthly periodic rate

Large loans like mortgages use a monthly periodic rate, which simply tells you the interest rate you’ll be charged each month over your loan term. On a loan, you can divide the APR by 12 (the number of months in the year) to calculate your monthly periodic rate. Then, multiply your current loan balance by the monthly periodic rate to calculate your monthly interest payment. You can also use an amortization calculator to estimate your monthly interest and principal payments for your entire loan duration.

Here’s an example: Let’s say your mortgage APR is 4.5% and your remaining principal balance is $200,000. Divide your APR by 12 to get your monthly periodic rate — 0.375%. Then, multiply the monthly periodic rate by $200,000 to see how much interest you’ll pay this month: $750.

How to calculate daily periodic rate

Credit cards usually use a daily periodic rate to calculate how much you’ll owe in interest each month. To calculate your daily APR, divide the APR by 365 (the number of days in a year) to convert your annual rate into a daily periodic rate. Then, multiply your current balance by the daily periodic rate and the number of days in your billing cycle to determine your monthly interest charge.

Here’s an example: Let’s say your credit card has an APR of 12% and last month you charged $1,000. Divide your APR by 365 to get the daily periodic rate — .0328%. Then, multiply this amount by your current balance and the number of days in your billing cycle, let’s say 30, to see how much you’ll pay in interest on your $1,000 balance — $9.86.

Where can you find your APR?

Banks and lenders are required to display APR information prominently. You can find your APR on your loan estimate, lender disclosures, closing paperwork or credit card statement. On your credit card statement, it’s usually at the bottom and is often labeled “interest charge calculation” or something similar.

APR vs interest rate

The interest rate is a percentage you will pay to borrow money. It doesn’t reflect any fees or other charges associated with taking out the loan. For credit cards, interest rates and APRs are the same.

For other loans, like mortgages, your APR is a calculation that includes both your interest rate and any fees you pay up front. APRs are provided by lenders so you can more easily do an “apples to apples” comparison of multiple banks and lenders, since fees can vary considerably. Learn more about mortgage APR vs interest rates.

APR vs APY

As you’re shopping for a loan, you may see the term APY, in addition to APR (lenders are required to show both). APY stands for annual percentage yield. Like APR, APY is a helpful calculation for determining how much you’ll pay for the money you borrow because in addition to factoring in fees, APY also includes compounding interest. Compounding interest is interest on a loan that accrues on both the initial principal and over time.

As you explore the APR and APY of your loan, you’ll also see the term “nominal interest rate.” Your nominal interest rate is your base interest rate, without taking into account fees or inflation.

Variable vs fixed APR

A variable APR means that the rate you’ll pay can change over time, as market conditions change. Variable rates are influenced by the prime rate, which is the industry benchmark rate at any given time. A fixed APR means that you’ll pay the same interest rate throughout the life of the loan, regardless of market fluctuations. Credit cards have variable APRs, while vehicle loans and personal loans often have fixed rates. Mortgages are available with either fixed or variable rates, but no matter which you choose, the higher your credit score, the lower the rate you’ll usually get.

Types of APR

Credit cards can have multiple types of APRs, such as an introductory rate and a cash advance rate. These additional APRs can impact your total interest owed. When you carry a balance on your credit card from purchases, cash advances or balance transfers, the APR is used to calculate how much you’ll pay in interest on your next statement. Here is a quick overview of some of the language credit card companies are using:

Purchase APR: This is the interest rate that will be applied to purchases you make with your credit card.

Cash advance APR: Many credit cards give you the option of getting a cash advance against your credit limit, and often this service has a different, often higher, APR.

Penalty APR: If you violate the terms of your credit card by, for example, making a late payment, you may be subject to a high penalty APR.

Introductory APR: Credit card companies often offer low-interest or zero interest APRs for a set number of months after opening your account, as an incentive to new customers.

Promotional APR: To encourage you to use your card, credit card companies sometimes offer promotional APRs for a specific period of time or a specific credit use, like balance transfers.

Does APR affect your monthly payment?

Yes, your APR affects your monthly payment. With loans like a mortgage, you’ll pay a monthly interest payment in addition to your principal for the duration of your loan term. The higher your APR, the more you’ll pay in interest each month and the longer it will take for you to start making a significant dent in your principal balance.

Depending on the type of loan you choose, a fixed or variable APR can also impact how much interest you’ll pay each month over the life of the loan. At first, you’ll pay more toward the interest every month, since your interest is a percentage of the principal balance owed. As you move through your monthly payments, you’ll pay less and less in interest each month and more in principal, lowering your overall loan balance. To get an estimate of your monthly mortgage payments over time, use our amortization calculator.

Why is APR important?

Before the enactment of the Truth in Lending Act, including more recent amendments to it like the TRID Disclosures, consumers found it difficult to effectively compare loans because each lender presented information differently. Today, all lenders must use the same terminology and display rates the same way — with an APR that takes into account all up-front fees. Even with APR information available, it’s still important to ask every lender for an itemized list of fees they charge.

What is a good APR?

A good APR is a low one, since you want to pay as little as possible in interest over the life of the loan. As mentioned above, the rates advertised by a lender are typically the lowest available rates, which means you’ll need to meet specific conditions and have a solid credit score to qualify.

On a loan

Mortgage rates fluctuate over time, so it’s best to keep a pulse on current rates. Keep in mind that a low interest rate doesn’t always guarantee a lower APR — it all comes down to the fees your lender is charging and anything else that is financed into your loan, like your closing costs.

Even if two lenders advertise the same interest rate, the APR might end up higher for one than the other. Say you’re looking for a mortgage and two lenders advertise a 4.5% interest rate, but the APR of the first lender is 4.85% and the second lender is 5.1%. The APR for the second lender is higher because they charge higher fees and closing costs to obtain the loan.

On a credit card

Anytime you can get a credit card APR for lower than current average interest rates, you’re in a good position. According to the Federal Reserve, the average interest rate for credit cards has hovered around 14% to 15% since 2018. Remember, if you pay off your balance in full each month, the APR won’t really matter. If you do plan on paying off your balance monthly, you may want to consider choosing a card with a higher APR but better benefits. If you plan on carrying a balance, a lower APR is more important. Some cards even offer 0% APR for a certain time period after opening the account, but keep in mind the introductory APR will typically be replaced with a much higher APR after that period expires.

How can I get a lower APR?

Your credit score and credit history play an important role in the APR you’ll be able to get. Whether you’re taking out a mortgage or simply opening a new credit card, you can boost your credit profile by making your payments on time and avoiding maxing out credit cards. It’s considered best practice to avoid using more than 30% of your available credit at any given time. Also, be sure to monitor your credit for fraud or mistakes, which can negatively affect your score.

For more mortgage related tips, visit our Mortgage Learning Center.

How much home can you afford?

At Zillow Home Loans, we can pre-qualify you in as little as 5 minutes, with no impact to your credit score.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Get pre-qualifiedHow much home can you afford?

See what's in reach with low down payment options, no hidden fees and step-by-step guidance from us at

Zillow Home Loans.

Zillow Home Loans, NMLS # 10287. Equal Housing Lender

Calculate your BuyAbility℠

Loading

LoadingRelated Articles

Get a mortgage with Zillow Home Loans

Go from dreaming to owning with low down payment options, competitive rates and no hidden fees. A dedicated loan officer will guide you until you have your keys in hand.

Zillow Home Loans, NMLS #10287. Equal Housing Lender.