8 min read

Zillow Economists Explain: Why Are There Still So Few Homes for Sale?

Skylar Olsen, senior principal economist at Zillow, said early signs indicate a surprising degree of buyer confidence.

Written by Susan Kelleher on July 8, 2020

In March, when COVID-19 began sending economic shock waves across the country, aspiring home buyers sidelined by years of low inventories and out-of-reach prices took to the internet with a common question: “Is now a good time to buy?”

Chances are they were recalling the Great Recession, when criminally lax lending practices fueled by Wall Street speculators created a housing bubble that led to a flood of foreclosed homes hitting the market. That recession lasted from December 2007 to June 2009.

More than five months into COVID-19, it’s clear that the current recession is nothing like the last one. Instead of swelling inventories, there are even fewer homes for sale now than there were at this time last year — 20% fewer — and price declines have barely registered.

So what’s going on? Why, during a time of widespread unemployment and dramatic economic decline, are there still relatively few homes for sale? Why haven’t home prices dropped dramatically? And how can agents help buyers who want or need to buy right now position themselves to act if a suitable home comes on the market?

COVID-19’s impact on housing inventory

Even before the pandemic, there were more people who wanted to buy a home than there were sellers.

Four main things have driven the shortage:

- a record long expansion and low unemployment, pre-COVID-19

- historically low interest rates that give people more buying power

- a sizable new generation of home shoppers entering the market while older generations were choosing to hang onto their homes

- a sharp drop in new home construction over the past decade

The U.S. economy has never had a sudden shock like the one we’re now experiencing, so no one knows how buyers and sellers will continue to respond to it. Economists at Zillow have been tracking key signals to predict what will happen to the supply of homes and the prices they’re selling for.

Based on those early signals, Zillow economists predict that home prices will decline by 1% to 2% from February highs to an expected low point in October. After that, prices are expected to return to pre-coronavirus levels before summer 2021.

Skylar Olsen, senior principal economist at Zillow, said early signs indicate a surprising degree of buyer confidence.

“There are signs buyers are showing up,’’ she said. Mortgage purchase applications and pending home sales initially dropped off in March, but then quickly snapped back; and online searches for homes — likely a combination of recreational browsers and serious buyers — rose 50% above previous levels.

Olsen said prospective buyers, many frustrated by low inventory in previous shopping seasons, seem to think that now might be a good time to get a good deal on a home and lock in a favorable mortgage rate. Meanwhile, homeowners seem to think they might be better off waiting to sell until the economic picture becomes more clear, Olsen said.

“Those two behaviors offset each other,” she said, which results in even fewer homes being listed for sale and helps explain why — even as COVID-19 was hitting the economy — bidding wars for homes were still occurring in some markets.

“Hopefully, sellers are watching buyers return,’’ Olsen said. “That builds the confidence of sellers, both existing homeowners and builders, to start returning more inventory to the market.”

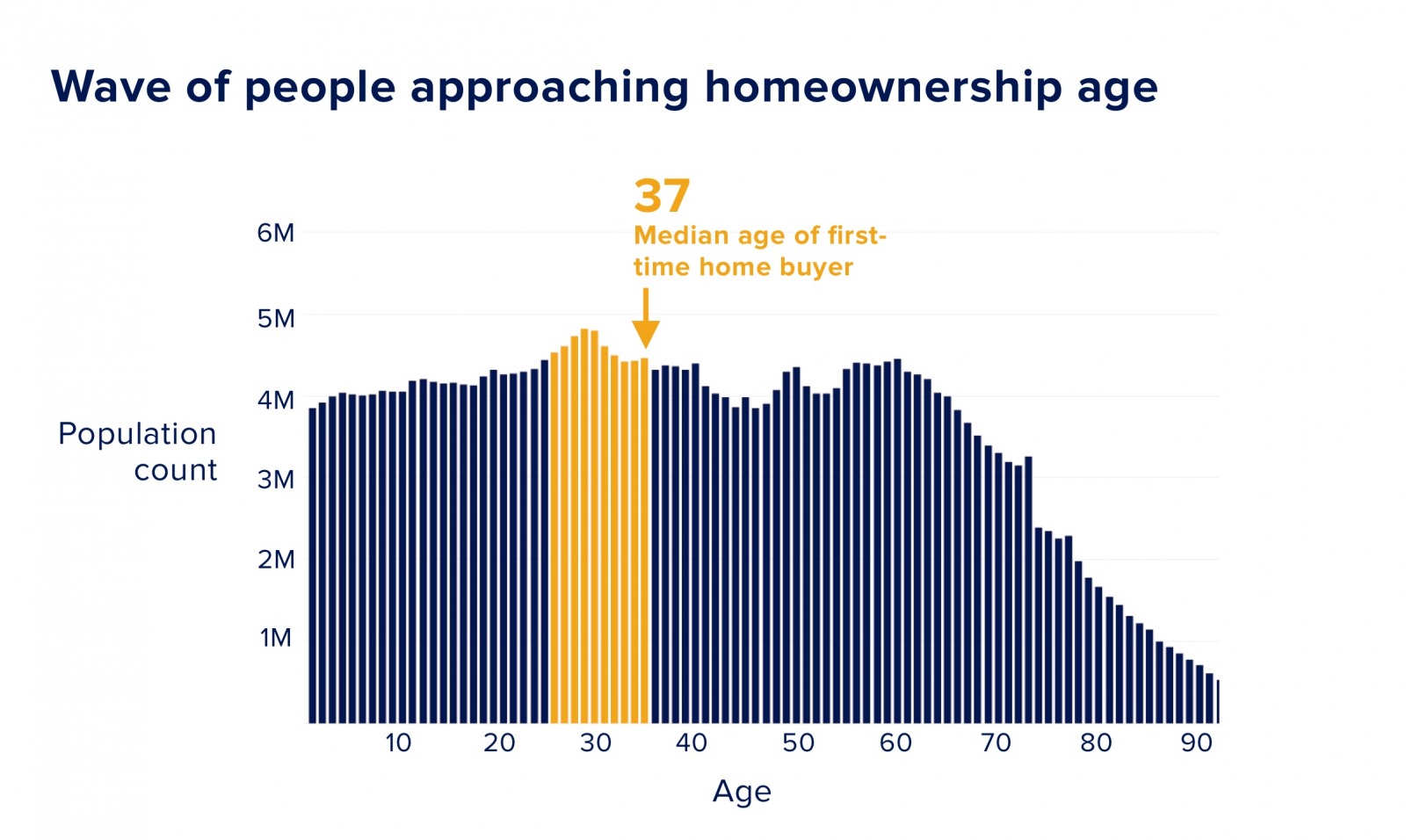

More buyers than sellers = housing shortage

In order for home builders to keep pace with the number of new households formed in the U.S., they need to build 1 million homes every year. Building has lagged far below that pace, mainly because the home-building industry was decimated during the Great Recession and had only started showing signs of come back earlier this year.

The Great Recession also disrupted the retirement and downsizing plans of older generations: Their savings took a big hit, and their adult children -- facing under-employment, record student loan debt and fast-growing rents -- moved back home. With retirement on hold and more adults to house, fewer baby boomers were putting their homes up for sale, further constraining supply.

The timing coincided with the emergence of a new crop of buyers from the massive millennial generation, who are just now hitting their peak home buying years.

With a relative scarcity of newly built homes, the inventory of for-sale homes has consisted mainly of existing homes.

Historically low interest rates fuel demand

Interest rates on mortgages, which have been at historic lows for some time, also have fueled demand.

Low mortgage interest rates boost buying power and make homes more affordable.

A home is typically considered affordable if the monthly payment (mortgage + taxes + insurance) consumes no more than 30% of a buyer’s monthly income. This allows the household to handle a housing payment and other debts and still have enough left over to spend and save.

“The low mortgage rate is the deal right now, not falling prices,’’ Olsen said. “That is a huge boon for buyers.”

But it becomes less of a boon if the shortage of homes for sale keeps prices growing at a fast rate. After all, the mortgage rate can’t help you build a competitive down payment in the first place. And since credit is tight, buyers who planned to put down 5% might not get a loan unless they put down 10%.

New construction

The home-building industry appeared ready for a comeback in January, when construction began to finally keep up with the formation of new households.

The sudden uncertainty around COVID-19 caused builders to pull back. Some began offering buyer incentives to reduce the inventory on their books, offering one of the few opportunities for a “deal” right now, Olsen said.

The incentives helped lower the median price of a brand new home to about $300,000, which is an affordability sweet spot for many buyers, according to Olsen.

Whether those promotions and incentives hold depends on the demand for new homes and the cost of building under safety restrictions to minimize infections on job sites — both of which will affect the supply of new homes coming down the pipeline. A lot will depend on whether buyers keep showing up, she said, and whether buyers are confident enough to stick with their long-term plans.

Deciding whether to buy or continue renting

Zillow’s economic research team predicts that home prices will hit their softest moment in October 2020.

The forecast depends on a lot of moving parts, including the willingness of federal and state legislators to continue to give breathing room to homeowners by protecting them from new foreclosure actions, boosting unemployment benefits and sending aid to individuals and small businesses.

“Those measures keep delinquencies low and distressed properties out of the market, but that expires July 31,’’ Olsen said. “When you ask whether the price stability we’re seeing will last or whether it will get softer — those questions depend on whether we’ll continue the support that people need if job recovery, when we do start to recover, is slow, especially if you have another round of COVID in the fall.”

Since timing the market is difficult even for seasoned investors, agents should help buyers focus on their own personal situations, said Olsen.

“If I’m a potential buyer, all I really need to know is if I’m going to stay for several years to make buying a better financial decision than renting — which is what most people expect when they buy homes in the first place,’’ she said. “It’s very hard to time the market, so instead focus on ensuring the right match between you and your future home. In a tight inventory environment that means being always on the lookout and ready to go when you find that fit. Don’t wait for signals that prices are hitting a low point.”

People who want or need to buy during this time should get pre-approved by a mortgage lender to see if they can get financing, and what interest rate will be available to them. Lenders have tightened up available credit, giving more favorable rates to people with excellent credit, larger down payments and simple, conforming mortgages. But all signs indicate that mortgage rates are likely to remain low for the foreseeable future.

How your clients can prepare to buy during COVID-19

Given the current conditions, Olsen said buyers should get ready to move if a home they want becomes available.

“In an environment where home prices could fall — we’re not seeing it yet but these recession dynamics and the loss of the jobs and the lack of credit availability may start to soften things — it’s important to plan ahead,’’ she said.

Her advice for helping buyers prepare:

- Embrace all the tools that allow homes to be toured remotely and safely so your clients can move quickly if the home is a good fit.

- Determine their budget and how high they want to go.

- Ask them to reflect on must-haves and things they’re willing to trade-off, especially if working at home is a long-term option not just in their current job but in their industry. Can they handle a longer commute? Is a home office a must-have?

- Help them think about what their life might look like three to five years down the line. “The house has to work for them in five years for this to be a really confident home buying decision.”

With pre-planning and expert knowledge of the market, she said, you can help your clients strike quickly when the opportunity comes.

Tips for top-performing listings

Backed by new research, this guide reveals what today’s top listings do differently to capture buyer attention and outperform the rest.

Learn more