Homes You Can Afford for $3,000 Lose A Bedroom As Mortgage Rates Increase

Home size per dollar still largest in Memphis and the Midwest, despite declines driven by mortgage rates.

Home size per dollar still largest in Memphis and the Midwest, despite declines driven by mortgage rates.

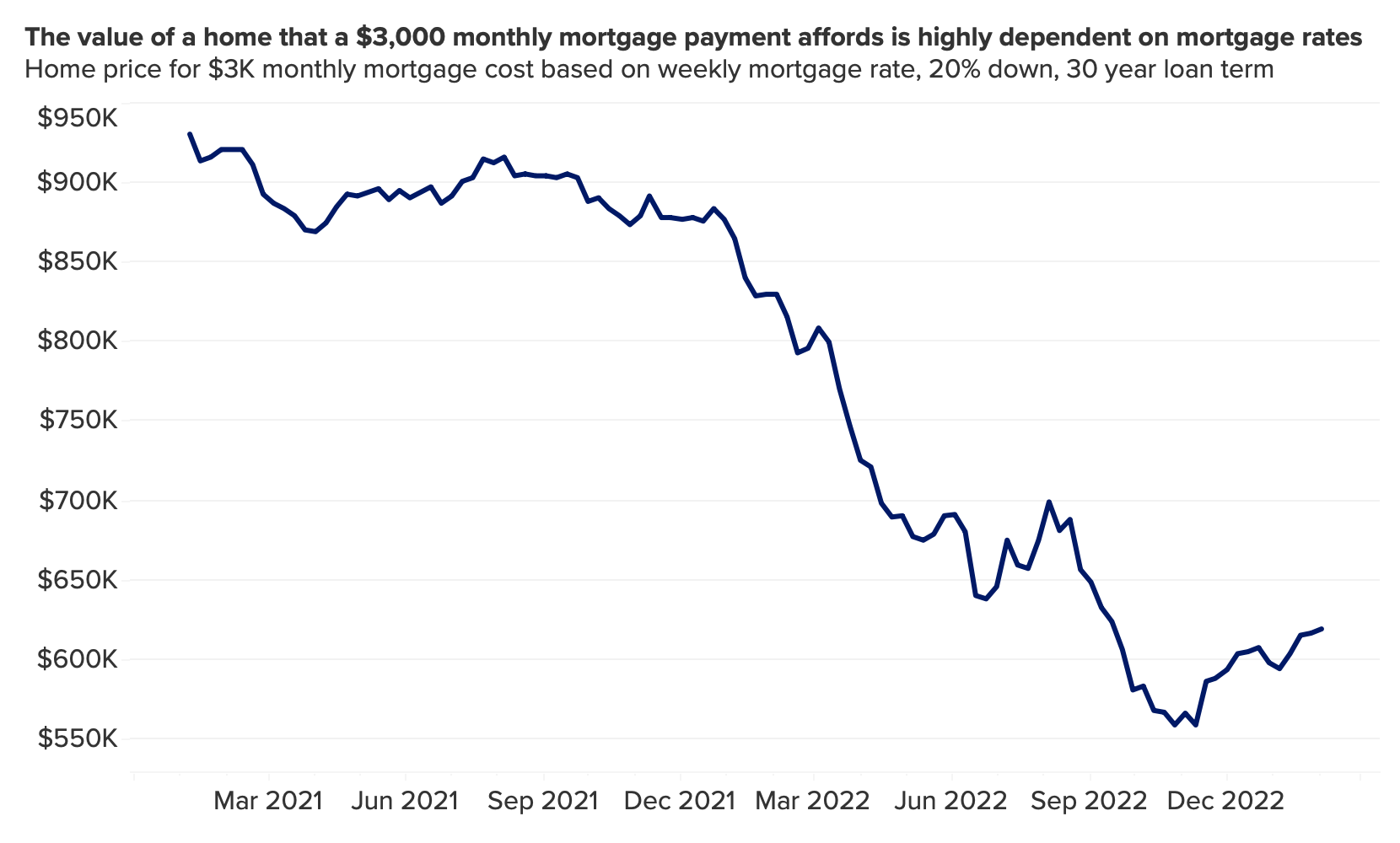

Last year’s drastic rise in mortgage rates turned the housing market on its head. Rates for prime borrowers more than doubled in 2022, often bouncing around wildly from week-to-week. Not only did this volatility make it difficult for homebuyers to confidently budget for their purchase, the increased rates alone substantially reduced the values and size of home an aspiring homebuyer could afford.

Specifically, at the beginning of 2021, when mortgage rates were at their lowest, a home buyer who made a 20% down payment and can spend $3,000 per month could afford a home worth $930,000. By mid-autumn of 2022, that same buyer looking to spend that same $3,000 could now only afford a home worth just shy of $560,000 – a whopping $370,000 difference in buyers’ purchasing power in less than two years. And while $3,000 is on the upper end of what a typical home buyer may consider affordable, it clearly illustrates the dramatic impact of changing mortgage rates, where a percentage point change in the mortgage rate will have a large dollar-amount effect on purchasing power.

The increase in costs significantly changes the type of home within a buyer’s reach, and has taken a chunk – quite literally – out of what shoppers can afford. On average, a $3,000 monthly mortgage payment today buys a home 140 square feet smaller than a year ago, meaning that, in many cases, buyers will likely have to sacrifice that extra bedroom when considering their options.

Despite major size declines, affordable areas still offer value

Like all things housing, the difference in how much square footage a $3,000 monthly mortgage payment affords a buyer is more stark when zoomed into specific markets. On the one hand, more affordable markets offer homes with larger footprints to begin with, leaving this measure with further to fall as climbing mortgage rates applied pressure to buyers’ purchasing power. Hartford, Connecticut had the largest drop in the size of home a $3,000 per month payment can afford, losing 1,200 square feet in the last year. Buyers in similar situations in Indianapolis and Cleveland both lost out on over 1,000 square feet.

On the other hand, buyers in pricey markets had less space available to lose, but their floorplans are shrinking all the same. San Jose homes that can be afforded at $3,000 per month are now the smallest in the nation at a median of 1,052 square feet, after dropping from 1,228 square feet just one year prior. Los Angeles, San Diego, and San Francisco are close behind, all below 1,400 square feet.

Homes in more affordable markets that saw some of the biggest declines in footprints still provide the biggest bang for 3,000 bucks per month. Southern and Midwestern markets like Memphis, Birmingham, and this year’s predicted hottest market, Charlotte, are among the twenty markets that still provide a spacious 3,000 square-foot home, despite shrinking last year.

Purchasing power trending up as sales season approaches

Despite last-year’s losses, purchasing power for buyers is trending up heading into the spring shopping season. As mortgage rates have eased down since October, buyers have gained an additional $60,000 in purchasing power, meaning the footprint of a home buyers can afford for $3,000 increased in all fifty major markets. Home size has increased the most in Salt Lake City (365 square feet), Minneapolis (357), Memphis (346), and Denver (340), and even the markets with the smallest homes had modest gains.

Buyer and seller experiences will differ greatly by market – an experienced agent can help navigate local currents. Further volatility in mortgage rates is expected heading into the spring. Tools like Zillow’s affordability calculator can help determine what kind of home will fit individuals’ budgets

{kind=link}