Despite 7% Mortgage Rates, One in Seven Families Could Still Afford To Take On A New Mortgage

In 2022, 39% of the roughly 134 million families [1] residing in the U.S. did not own the home they lived in, according to estimates from the American Community Survey. [2] While some families chose to rent, others simply could not afford to own a home. Among those who did not own their home, roughly 7.9 million of these families were “income mortgage-ready”, meaning the share of their income spent on a mortgage payment for the typical home in their local market [3] would have been 30% or lower.

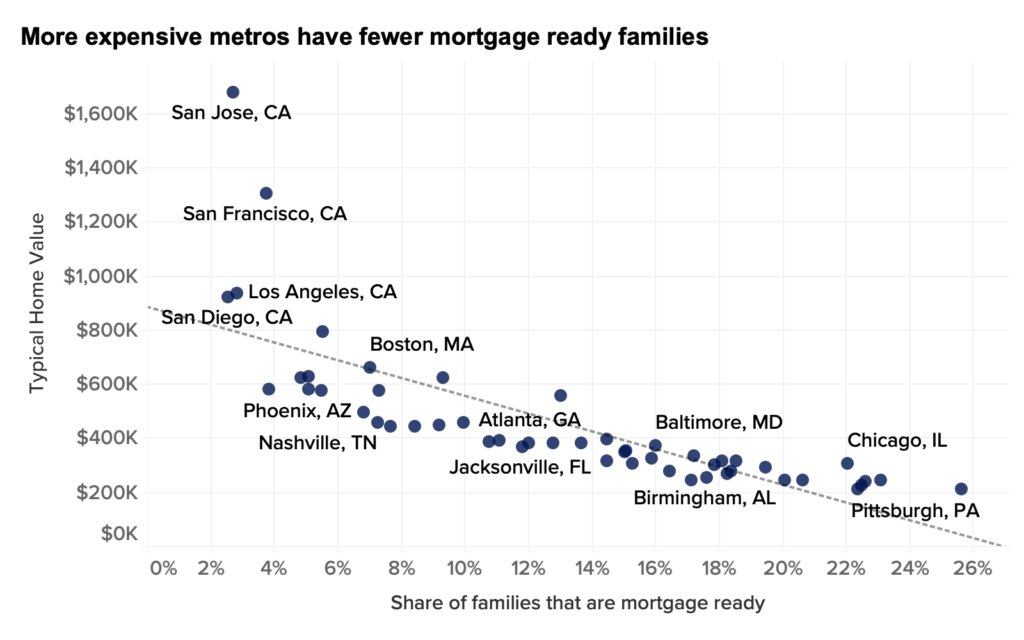

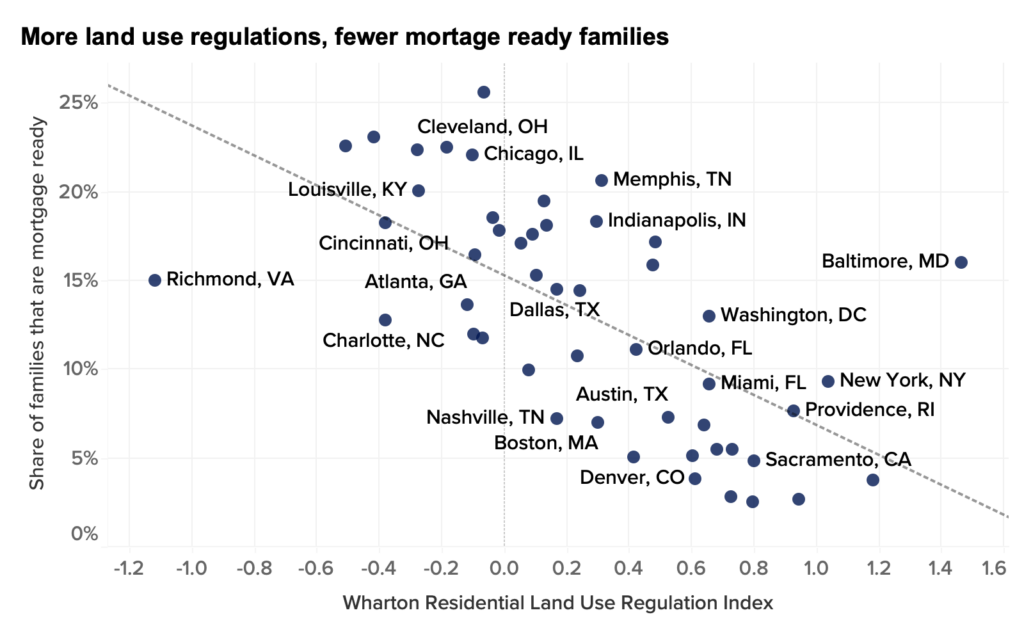

Families are more likely to be mortgage-ready in metros with fewer land-use regulations, even with relatively lower median incomes

While roughly 7.9 million families were income mortgage-ready across the country, there is substantial variation across metropolitan areas. The share of mortgage-ready families varies from 25.6% in Pittsburgh to just 2.6% in San Diego.

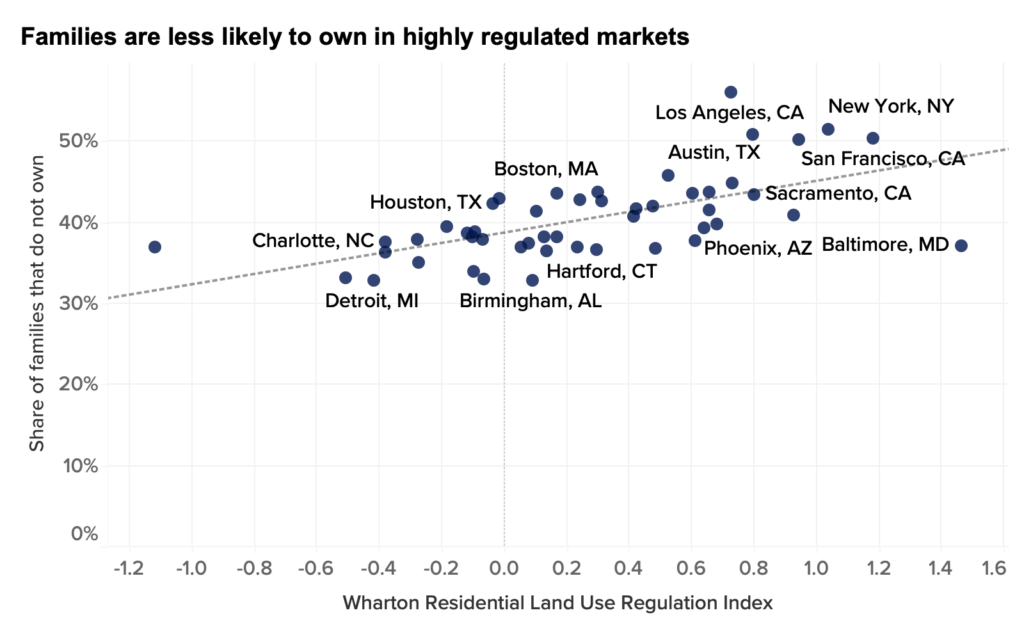

Even in markets with higher-than-average incomes, those who live in highly regulated housing markets are least likely to be mortgage-ready. This is because housing supply persistently falls short of increases in housing demand.

Removing barriers to homeownership that aren’t related to income — credit assistance programs, down payment assistance or help with closing costs, for example — would likely improve access to homeownership for more than one in seven families nationwide. However, the fact that the majority of families don’t have the income necessary to comfortably afford the typical monthly mortgage cost in their local market suggests that removing roadblocks to building more affordable housing would have the most significant impact on improving access to home ownership.

[1] We define families as groups of related individuals in each household using the FAMUNIT variable in IPUMS USA. While not all families want to own their home, it is likely that families that are not related to the household head could potentially want to form their own household.

[2] Steven Ruggles, Sarah Flood, Matthew Sobek, Daniel Backman, Annie Chen, Grace Cooper, Stephanie Richards, Renae Rogers, and Megan Schouweiler. IPUMS USA: Version 14.0 [dataset]. Minneapolis, MN: IPUMS, 2023. https://doi.org/10.18128/D010.V14.0

[3] This assumes a family can only afford a 3% down payment at the highest home value – measured by ZHVI – and the highest mortgage rate recorded each year based on applications submitted to the Freddie Mac from lenders across the country. A lower down payment implies higher monthly mortgage payments, raising the threshold income needed to be considered mortgage ready in this analysis. We also assume PMI is 1% of the original loan amount. These assumptions make our estimates a lower bound for the number of families that could comfortably take on a new mortgage payment since most buyers (88%) had a down payment larger than 3% in 2022.

{kind=link}