A Change in the Wind: Higher Mortgage Rates, Inventory Rebound Could be First Steps Toward a More Balanced Market (March 2022 Market Report)

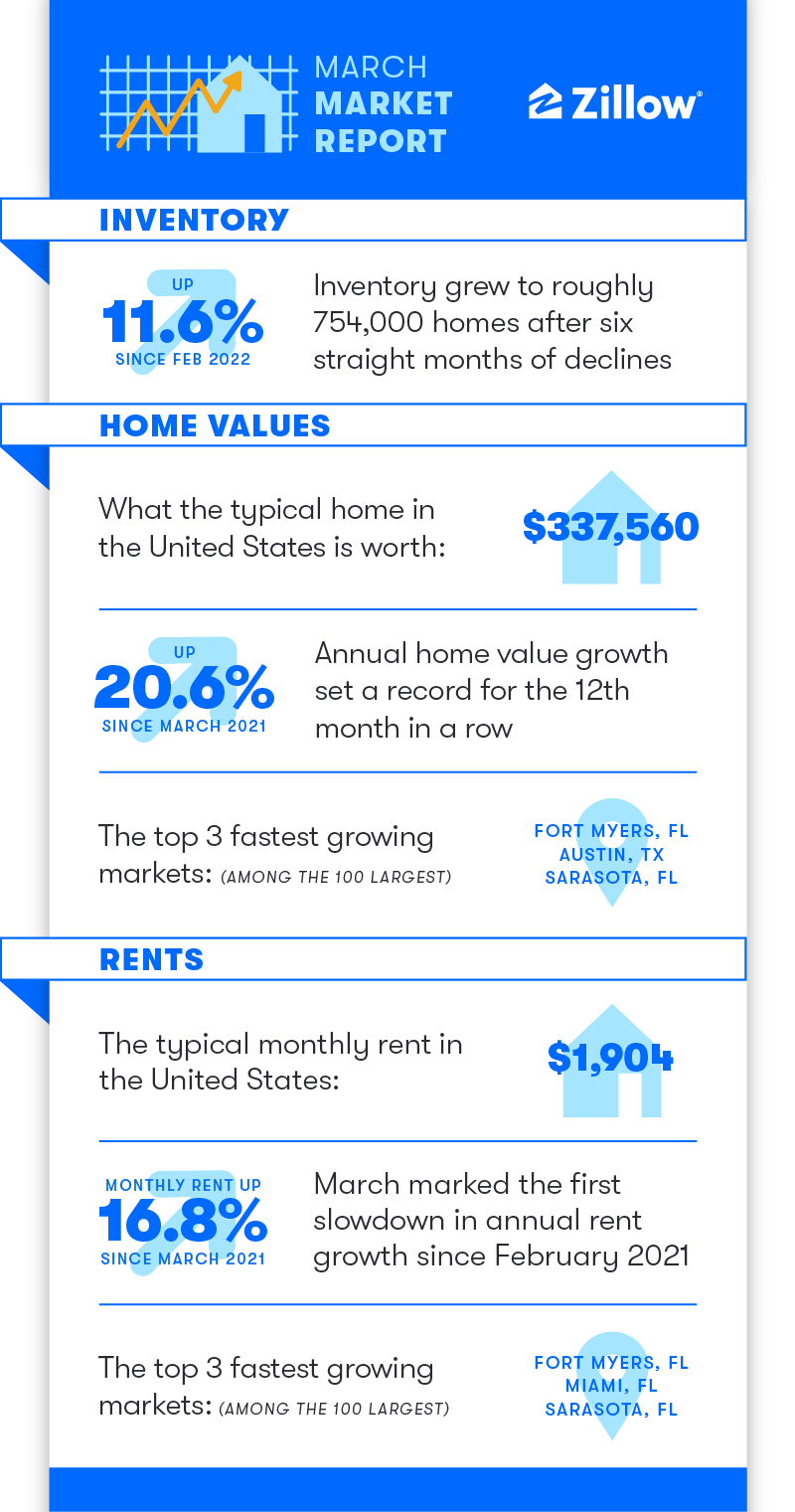

Inventory rose substantially in March, a welcome return to seasonal norms for the housing market.

Inventory rose substantially in March, a welcome return to seasonal norms for the housing market.

Home shoppers are facing a one-two affordability punch this spring: Quickly rising mortgage rates are compounding affordability challenges that have been brought on by record home value growth. Yet so far, in spite of rising costs, buyers remain ready to pounce on any inventory that hits the market. When the expected spring inventory boost finally arrived in March, the pace and volume of sales picked up in response.

Inventory — the count of active for-sale home listings on the market — finally began to lift off in March after falling consistently since August 2021. Total listings jumped 11.6% from February, the biggest monthly gain in data through 2018, providing enough of a jump beyond seasonal norms that the market began to make a little progress back up from seasonally adjusted record lows. Looking back to the first quarter of 2019 for a pre-COVID seasonal comparison, national inventory this March was 52.2% below its March 2019 level: a modestly smaller deficit than in February, when listings were down 53.9% from the same time in 2019.

Of the 50 largest U.S. metros, those with the largest inventory deficits relative to March 2019 are Raleigh (-70.7%), Miami (-67.5%) and Nashville (-66%). Those with the smallest decreases are San Francisco (-9.2%), San Jose (-14%) and Minneapolis (-29.7%).

Buyers not deterred (yet) by higher prices

The cumulative effect of months of low inventory can be seen in still robust price appreciation. The typical U.S. home is now worth $337,560 — up 20.6% from March 2021. This is the 12th consecutive month in which a new record for annual price appreciation has been set.

Coupled with this year’s rapidly rising mortgage rates, those prices imply a monthly mortgage payment of $1,316 (principal and interest only, assuming a 30-year fixed-rate mortgage with a 20% down payment), which is 38% higher than in March 2021 and almost 20% higher than a mere three months ago.

All 50 of the nation’s largest metro areas experienced double-digit year-over-year growth in March. Annual growth was fastest in Austin (42.7%), Raleigh (34.9%) and Tampa (33.1%), and slowest in Washington, D.C. (11.4%), Baltimore (11.6%) and Milwaukee (11.7%). On a monthly basis, growth was fastest in Tampa (3.0%), Raleigh (2.8%) and Las Vegas (2.8%), and slowest in New Orleans (0.6%), Richmond (0.7%) and Providence (0.9%). Sixteen of the 50 largest markets saw decelerating monthly growth in home values, the most since November.

March proved to be the biggest test yet of whether enough buyers can meet the new asking prices to keep home values growing at a record pace, and the answer was a resounding “yes.” Newly pending sales rose 11.6% in March — the exact same increase as inventory. The median listing went pending after just nine days — two days faster than in February and 24 days faster than the last March before the pandemic, in 2019.

Early signs of a rebalancing

While there is plenty of fuel in the tank as home-shopping season kicks into gear, there will be a point when the cost of buying a home deters enough buyers to slow price growth, and signs are emerging that we may be nearing the peak for home value appreciation. Month-over-month price growth was 1.6% for the second month in a row in March — a pace that, if compounded for 12 months, would yield 20.7% annual growth.

Newly pending home sales this March lagged behind their pace from a year ago, with 19% fewer than in March 2021, after February notched a 15% year-over-year decline. The slowdown in sales volume could be attributable to the one-two punch of high prices and rising mortgage rates denting demand this spring.

A looming swing back toward a more balanced housing market should not be confused with a market crash, which remains very unlikely. In all probability, slowing price growth will not end with prices actually falling, and in fact, the market should remain hot by historical standards for many months to come. Supply is on the upswing, and demand will eventually cool as prices rise out of reach for enough households, but there is a long way to go before we reach a supply glut, and there is plenty of pent-up home-buying demand to work through.

Rental market still hot, but modestly cooling

The for-sale market is the most obvious place to observe the effects of limited supply, but the rental market is not immune, either. Home shoppers, especially aging millennials, who strike out in today’s competitive and sparse for-sale market are likely to stay renters longer. At the same time, the large Generation Z cohort is beginning to enter the rental market. Largely because of these two factors, this high rental demand is keeping rental vacancy rates near all-time lows and pushing rent prices — after a brief, early pandemic pause — up at an almost equally fast pace as home values.

Rents in March rose 0.7% from February and 16.8% from a year earlier. That marks a slight deceleration in both monthly and annual rent growth, after February’s record-high 17.2% year-over-year growth. Typical rent across the U.S. is now $1,904 per month, $295 higher than in March 2020. Rent growth was slow in 2020 after the outbreak of the pandemic, but skyrocketed in 2021. Florida metro areas made a clean sweep on the podium for fastest annual rent growth in March: Miami (32.6%), Tampa (28.1%) and Orlando (24.7%) had the fastest-growing rents of the 50 largest U.S. metros. Colder markets saw the slowest year-over-year growth in March: Minneapolis (7.0%), Milwaukee (7.6%) and Pittsburgh (8.9%) brought up the rear.

Looking ahead

Zillow’s home value forecast now calls for 14.9% growth through March 2023, down from a year-ahead forecast of 16.5% growth made in February. Zillow’s existing home sales forecast has been lowered as well, to 6.09 million sales in 2022, which would mark a slight decline of 0.5% from 2021. Affordability headwinds have strengthened faster than expected, largely due to sharp increases in mortgage rates, leading to the downwardly revised forecast. Still, these figures would represent a remarkably competitive housing market in the coming year. Annual home value growth of 14.9% would have been the highest ever recorded by Zillow before June 2021, and 6.09 million existing home sales would mark the second-best calendar year total since 2006.

{kind=link}