Memphis and Other Southeast Markets Have the Shortest Buy-Rent Breakeven Horizons

The amount of time it takes for owning a typical U.S. home to make more financial sense than renting an identical home is now 1.96 years – or a little under a year and 11 months. It's a year and almost four months in Memphis.

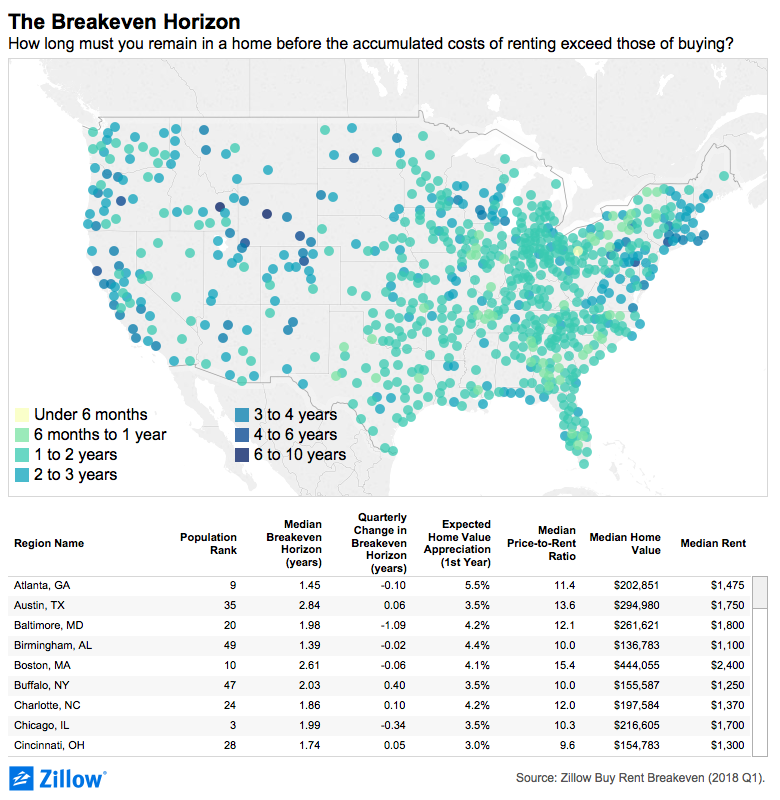

The amount of time it takes for owning a typical U.S. home to make more financial sense than renting an identical home is now 1.96 years – or a little under a year and 11 months – according to Zillow’s Buy-Rent Breakeven Horizon for the first quarter 2018. It dropped by a little more than a month from last quarter.

The breakeven horizon varies by region, with the shortest among major markets in Memphis, Tenn., where it takes just 1.32 years (a year and almost four months) for owning to financially beat renting. The longest breakeven is in Los Angeles, where it takes 3.7 years (three years and more than eight months) of owning the typical home for it to make more sense than renting.

The longest breakeven times tend to be in pricey coastal markets such as Los Angeles, Portland, Ore., San Francisco, Washington, D.C. and San Diego.

However, Hartford, Conn., Virginia Beach, Va., and Milwaukee also have relatively long breakeven horizons (3.23 years, 3.11 years and 2.8 years, respectively), despite their median home values being close to the national median of $213,100.

The reasons can be complex. Rents, home value appreciation and interest rates play a role in the breakeven equation. It also factors in the hefty transaction costs of buying and then selling a home in order to realize gains – as well as the savings and investment gains you could make as a renter by putting that down payment toward some other venture and avoiding homeownership expenses like real estate agent commissions and property taxes.

In addition to Memphis, other short breakeven horizons are clustered in the Southeast: Birmingham, Ala., Tampa and Orlando, Fla., and Atlanta, where it takes 1.39 to 1.45 years for buying to make more sense than renting. In four of those places, the median home value is below the national median; only Orlando’s is higher.

Here’s how Zillow calculates its Breakeven Horizon:

Zillow estimates a unique Breakeven Horizon for up to 3,000 individual homes pulled randomly from each ZIP code and uses the Zestimate and Rental Zestimate on the same houses, so we’re able to consider the costs of buying a house against the costs of renting that same house.

For buying, we assume:

- A 20 percent down payment

- Monthly payments on a 30-year fixed rate mortgage at the current interest rate for people with credit ratings between 680 and 740

- Property taxes

- Homeowner’s insurance

- 3 percent purchase costs

- 8 percent selling costs (because that’s how owners realize the gains)

- Annual maintenance costs equal to 1 percent of the home’s value

- For condos, 1.2 percent a year in HOA fees

- Home appreciation forecasts

- Federal tax deductions

For renting, we assume:

- A deposit equal to one month’s rent

- Rent payments

- Renter’s insurance

- 5 percent annual investment gains on money that would have been used as a down payment or gone towards other homeowner expenses the renter avoids

{kind=link}