Case-Shiller August Results and September Forecast: Gains to the Horizon

The predictable rhythm leaves us wondering which of these trends might break in 2018 – if any.

The predictable rhythm leaves us wondering which of these trends might break in 2018 – if any.

The U.S. housing market has settled into a predictable rhythm that shows very few signs of changing. There is incredibly strong demand, driven by a largely healthy overall economy and aging millennials entering their home buying prime, and there is too-low inventory, driven by limited home building activity. Together, those two factors continue to push housing prices up.

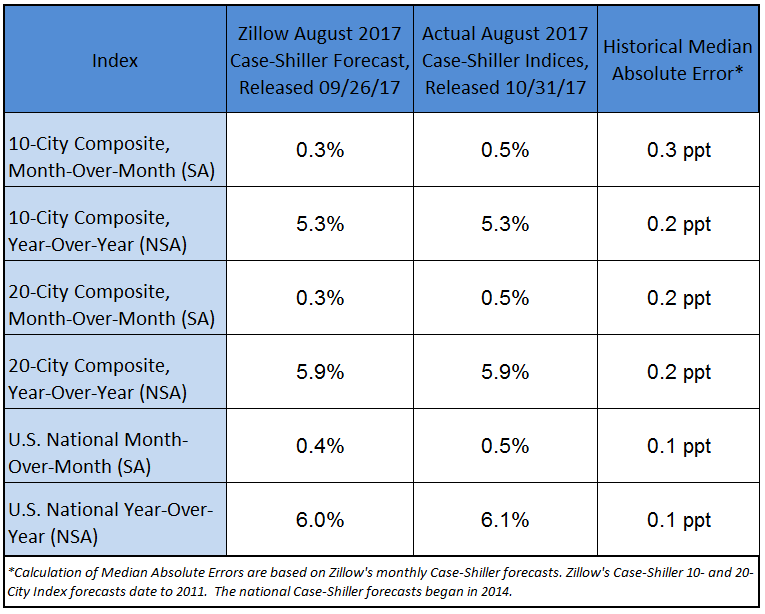

Case-Shiller’s U.S. National Index for August showed home prices again gained 0.5 percent month-over-month. Year-over-year, the index rose 6.1 percent, up from 5.9 percent year-over-year growth in July.

The 10-city composite gained 5.3 percent year-over-year, while the 20-city composite rose 5.9 percent year-over-year. Cities in the western U.S. continue to lead gains, with Seattle, Las Vegas and San Diego climbing the most among the 20 cities, with year-over-year price increases of 13.2 percent, 8.6 percent and 7.8 percent, respectively.

Mortgage interest rates are incredibly low, which everyone used to think seemingly couldn’t last much longer but which have now persisted for a half decade, helping keep homes affordable and contributing to high demand. And there is the same general feeling that for those home owners, buyers and sellers already in the market, things are markedly easier than for those would-be buyers trying to get in on the bottom rung.

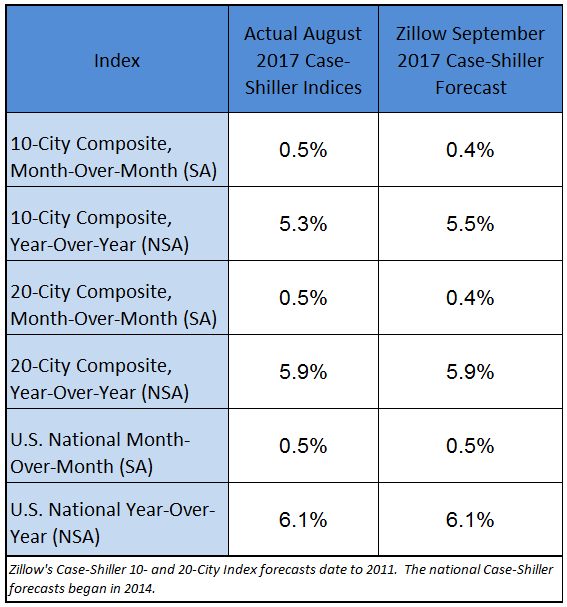

Our home-price forecast for September, which Case-Shiller will not release until Nov. 28, is for more of the same: We expect the national index to maintain its 0.5 percent month-over-month trend, with both city composites climbing 0.4 percent month-over-month, which is slightly slower than they have been.

It all leaves us wondering which of these trends might break in 2018 – if any. It looks likely the next Fed Chair will largely stay the course, meaning low rates and decent affordability for the foreseeable future. Building activity took a strong step forward last month, but we need many more months of that kind of growth before real progress is made toward building our way back to par. And nobody is rooting for, or expecting, any kind of economic slowdown that would otherwise take some of the starch out of high demand.

This status quo could certainly be a lot worse, and it’s very important to recognize that. But there are also real imbalances emerging between renters and owners, buyers and sellers, and hot markets and cooler ones that could grow into real long-term problems if left unaddressed.

{kind=link}