Zillow’s Insights on CPI and ZORI: Understanding the Future of Shelter Inflation

Zillow Economics predicts shelter CPI inflation – and the results remind us that unless active rental markets moderate even more, the U.S. economy as a whole will continue to grapple with the strain of rising costs of living well into 2025.

What Happened?

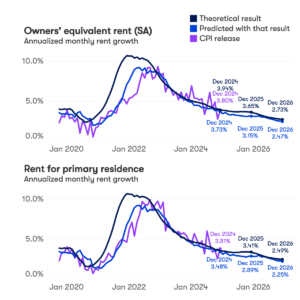

In line with today’s CPI shelter release, we expected seasonally adjusted CPI for owner’s equivalent rent (OER) to increase by 0.31% in December, an annualized rate of 3.73% (actuals = 3.80%). Using current on-market rent forecasts (ZORF) to push this dynamic further into the future, this implies a year-end OER inflation rate of 3.15% in 2025. Similarly, we expected CPI for renting your own residence to increase by 0.29%, an annualized rate of 3.48% (actuals = 3.81%). Based on current on-market rent forecasts, this implies a year-end inflation rate of 2.9% in 2025.

Source: Zillow Economics modeling of Shelter CPI released from the BLS.

This effort goes beyond a simple forecasting model. To form our expectations, we use our unique view into the incredible shock to on-market rents (the Zillow Observed Rent Index) and structural economic thinking to create a theoretical measure of how full-market rent (what CPI attempts to capture) will evolve over time. Structural modeling is the key to understanding full market rent – a composition of new leases and renewed leases as well as traditional and informal rental markets.

Why it matters?

Ultimately, it is a reminder that unless active rental markets moderate even more, the U.S. economy as a whole will continue to grapple with the strain of rising costs of living. The inflation debate rages on. One of the stickiest, and largest components, is shelter costs. With a unique dataset and lens from operating a rental market, Zillow Economics proposes that the shelter components of the consumer price index will remain elevated for some time. Long after excessive heat dissipated from the active market for new rental leases, rents averaged across the full market would continue to increase so long as newly mobile renters continue to pop out onto housing markets much more expensive than when they last moved. This will be a dynamic monetary policy makers at the Federal Reserve will have to consider as they continue to weigh inflation numbers and future policy moves.

How we did it: Rental market modeling in Zillow Economics

Zillow economics tracks changes in asking rent on active individual listings, and then weighs that data to reflect the full rental stock. That’s the tool we have in Zillow’s Observed Rent Index.

To help anticipate the shelter component of CPI, Zillow Economics creates a model of the rental market behind our view of the active market for new leases. This requires setting a few assumptions, like how often people move (we looked at census data for a good ballpark), and applying some structure, like the logic a landlord may use to increase rent for an existing tenant – a kind of “catch up” mechanic between rent for renewed leases and active market rents.

Using this economic model, we shock the system with observed ZORI and its newly released forecast, ZORF, to generate a theoretical CPI. This theoretical CPI is the result if all landlords and all renters were as simple and straightforward as our assumptions. The Shelter CPI numbers that dropped today reflect the tapestry of a more complex reality – different renters, different landlords, randomness, and mismeasurement – complexity that can be better anticipated by playing out a little structure. That’s why we love economics.

{kind=link}