The Impact of Credit Insecurity on Homeownership Rates and Affordability

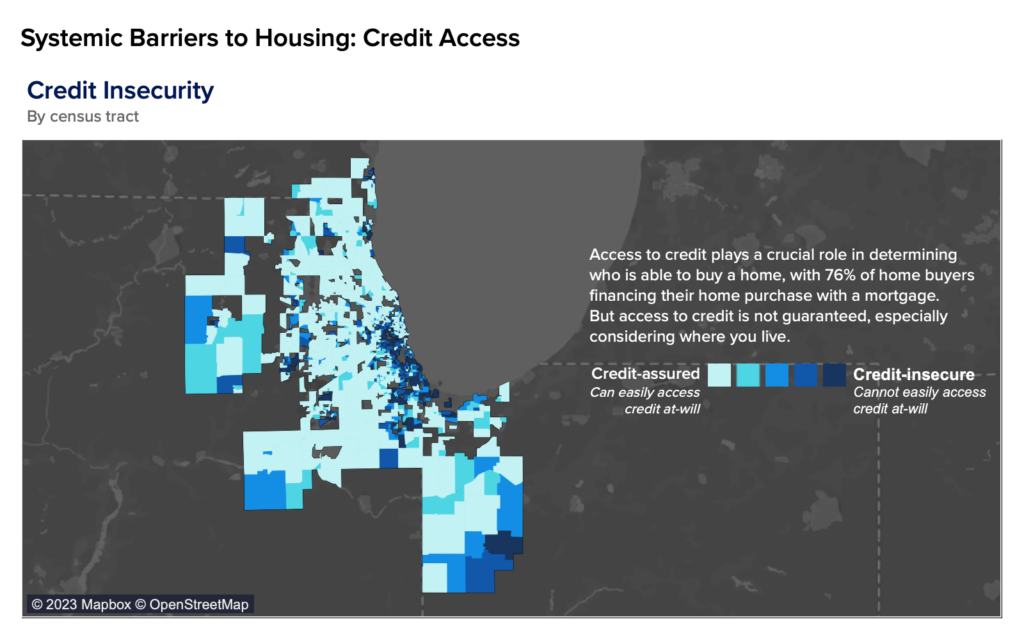

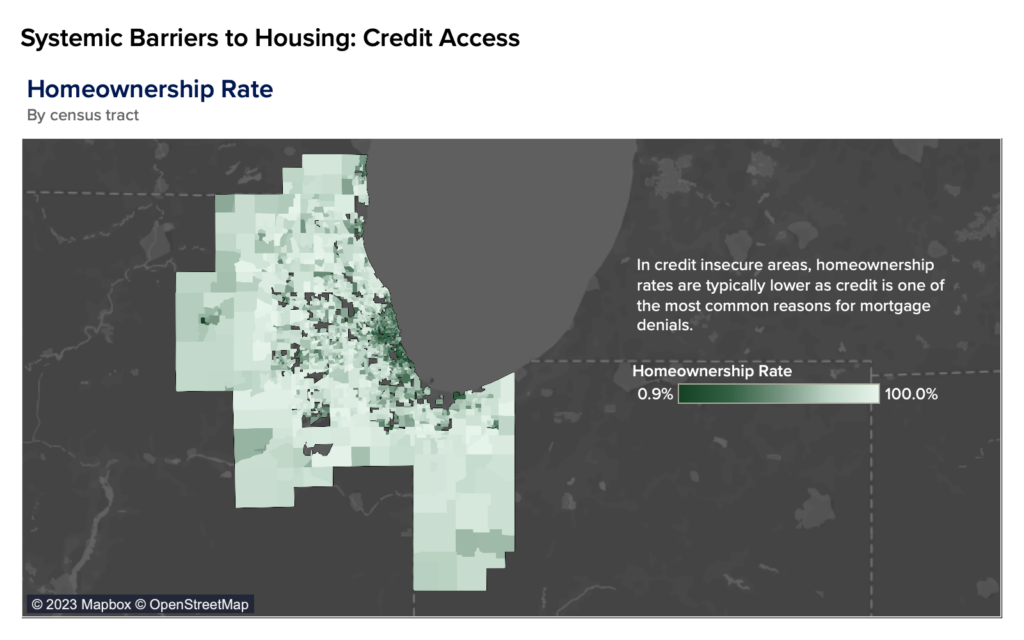

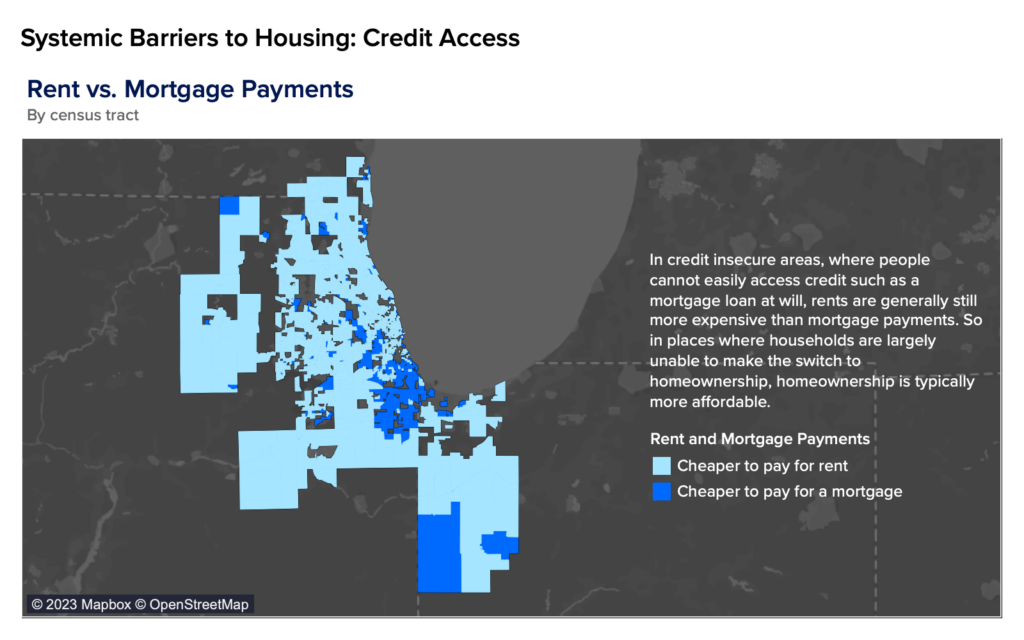

Access to credit plays a crucial role in determining who is able to buy a home, with 76% of home buyers financing their home purchase with a mortgage. But access to credit is not a given, especially considering where you live. In areas around the country with high levels of credit insecurity — meaning it is not easy to access credit at will — homeownership rates trend lower as fewer people have the credit background to allow access to home financing. What’s worse, despite the high costs of a mortgage in today’s market, it is still cheaper to pay for a mortgage than to pay for rent in many credit insecure areas, when the opposite is true in areas that are credit assured, making rental affordability more challenging for those residing in credit insecure areas.

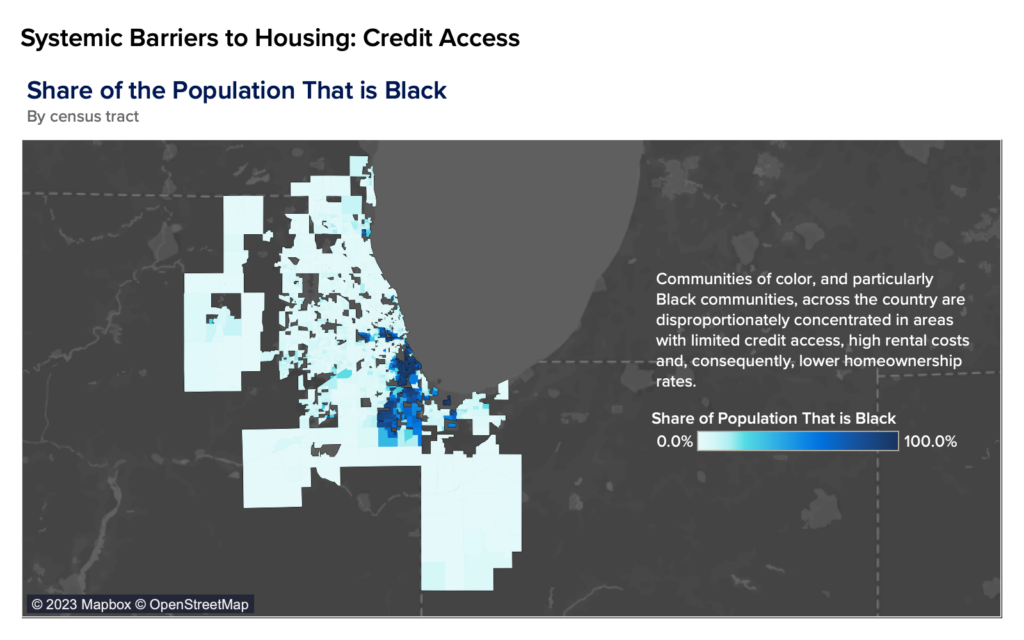

The unequal distribution of credit access disproportionately impacts Black households, who are more concentrated in credit insecure areas across the country. This adds to the systemic barriers that many Black households still face in the housing market, making the move to homeownership more difficult. Addressing the unequal distribution of credit is needed to help close the racial wealth gap and create a more equitable housing market.

Credit insecurity refers to the lack of access to credit at will, meaning it is challenging — or even impossible for some — to open a new line of credit for a credit card, secure a car loan, or get a new mortgage.

There are many reasons that an individual might be credit insecure, from having no credit history, having a subprime credit score or having a derogatory mark on a credit report, among other reasons. But what this research focused on is entire communities that are credit insecure. When entire areas have a high degree of credit insecurity — meaning many people are not able to access credit at will — it is disruptive and immobilizing.

Community-wide credit insecurity can also be read as a form of modern day redlining. Redlining refers to the discriminatory practice of denying financial services, such as loans or insurance, to specific neighborhoods based on their racial or ethnic composition. While redlining was officially prohibited with the passage of the Fair Housing Act in 1968, its effects continue to impact communities today, and credit is now one means that continues to prevent many Black households from accessing homeownership.

Previous Zillow research, in partnership with the National Fair Housing Alliance, found that communities of color generally have worse access to several key neighborhood amenities — including traditional finance outlets — than predominantly white communities. These disparities reflect the ongoing challenge of ensuring equal opportunity across racial lines when access to the basic building blocks of those opportunities remains unequal.

In credit insecure areas, homeownership rates are typically lower as credit is one of the most common reasons for mortgage denials. The inability to access credit hinders many households from making the switch to homeownership and benefiting from often lower monthly payments and wealth-building opportunities. And with a home being the largest asset many households ever own, especially for Black and Latinx households, the lack of generational wealth to pass on from lower homeownership rates will have an impact for generations to come.

Homeownership is usually the ideal for affordability in housing, as mortgage payments are typically lower than rents. But in the current high mortgage rate environment, that monthly cost equation has flipped, at least in most of the country. However, in credit insecure areas, where people cannot easily access credit such as a mortgage loan at will, rents are generally still more expensive than mortgage payments. So in places where households are largely unable to make the switch to homeownership, homeownership is typically more affordable. This leaves many households in credit insecure areas stuck in higher cost rentals, making planning and saving for future homeownership even more challenging.

The higher cost of rent in credit-insecure areas creates an additional burden for households. Analyzing the share of income spent on housing from the American Community Survey (ACS) by census tract reveals that households in credit-insecure areas are not only paying more for rent, but also paying a higher share of their income on rent. This double financial strain makes it even more challenging for these households to save up for homeownership in the future.

Examining the demographics in credit-insecure areas reveals that as credit insecurity worsens, there is a growing proportion of Black individuals within the population. While redlining practices may be illegal today, the underlying systems and structures that perpetuated racial disparities in homeownership still persist. Communities of color, and particularly Black communities, across the country are disproportionately concentrated in areas with limited credit access, high rental costs and, consequently, lower homeownership rates. This is the outcome of many systemic barriers that Black households face in housing going back to redlining, which forced many Black households to relocate to areas with fewer services and amenities including financial services. These communities often remain underserved by finance today. And until there is intentional action to create a more equitable housing market staked on equitable access to credit and financing, these problems will persist.

Credit insecurity significantly impacts homeownership rates, affordability and racial disparities in the real estate market. The challenges faced by households in credit-insecure areas extend beyond higher rents and limited credit access. It is essential to address these systemic issues and work toward creating equal opportunities for all communities to access homeownership and build wealth.

Policymakers could explore a number of solutions to help address this issue. Encouraging more financial institutions and landlords to report positive rent payments — and for government sponsored agencies to consider this data — would help renters build credit, especially in areas where building a credit profile is so difficult. Improving awareness of down payment assistance can help more renters overcome the cash barriers they face when trying to purchase a home. And supporting policies that build more homes can help open more doors to homes that are affordable and accessible. But it’s clear that whatever policies are imagined to help solve this problem need to be intentional about removing these systemic barriers set in place nearly a century ago with the introduction of redlining.

{kind=link}