December Case-Shiller Results and January Forecast: Why 2018 Looks A Lot Like 2017

The familiar patterns in the housing market that emerged in the second half of 2017 – lots of demand from home buyers, limited supply of homes available to buy, quickly rising prices and slow but steadily deteriorating affordability – are continuing to shape the start to 2018 as well.

The familiar patterns in the housing market that emerged in the second half of 2017 – lots of demand from home buyers, limited supply of homes available to buy, quickly rising prices and slow but steadily deteriorating affordability – are continuing to shape the start to 2018 as well.

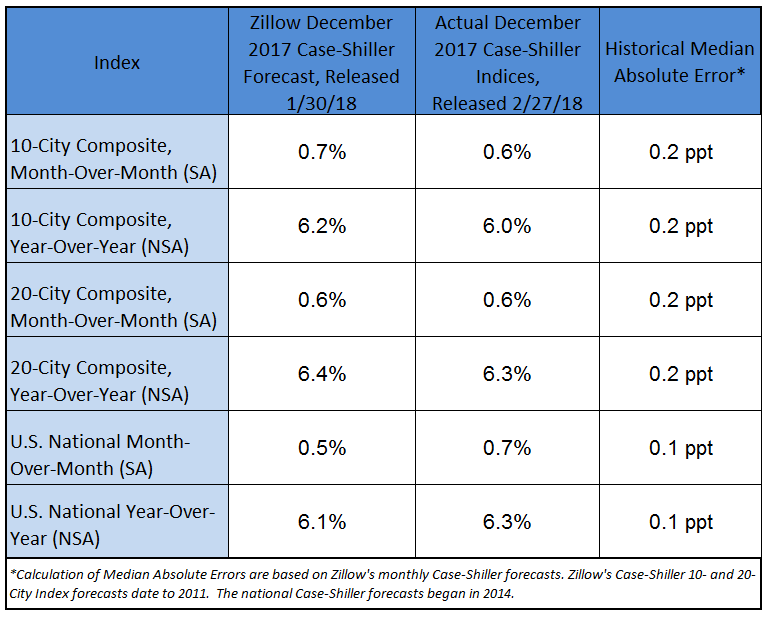

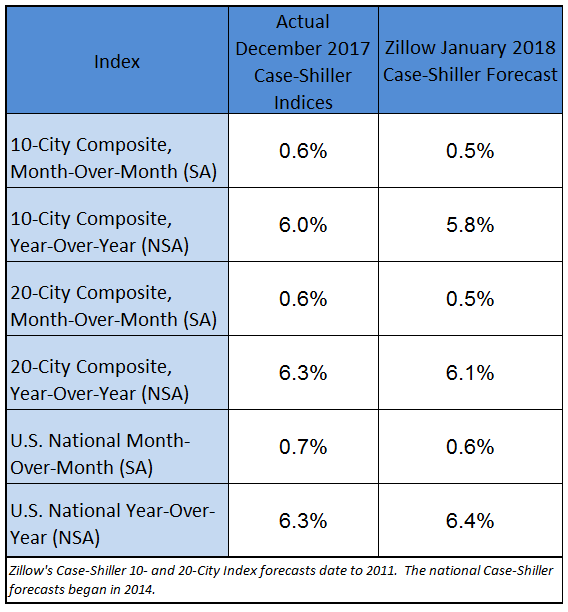

Zillow predicts the S&P/Case-Shiller national index will show a 6.4 percent gain in national home prices in January, a slight increase from the 6.3 percent annual gain home prices posted for December. The December increase was greater than November’s 6.1 percent annual gain. Case-Shiller will release January data on Tuesday, March 27.

Case-Shiller’s 20-city composite index rose 6.3 percent year-over-year in December, a slight slowdown from November’s 6.4 percent annual growth. The 10-city composite index climbed 6 percent, the same rate as the prior month.

Among cities included in the 20-city index, Seattle, Las Vegas and San Francisco reported the highest year-over-year gains in December, at 12.7 percent, 11.1 percent and 9.2 percent, respectively.

Mortgage interest rates have surged since the beginning of the year, remaining low by historic standards but – combined with fast appreciation – approaching levels where affordability may start to erode more quickly.

It feels like the market has been waiting for an inventory dam to burst, and for many more properties to magically appear for sale that might help cool competition and rapidly rising prices. But wishing has not made it so, and low inventory looks to be the norm going forward.

Builders are trying to do their part, but building conditions thus far in 2018 don’t look too different from 2017: Buildable land is scarce and expensive, labor is tight, and permitting and materials costs keep going up.

Given these challenges, more inventory needs to come from owners of existing homes choosing to list them for sale. For that to happen, would-be sellers need to feel confident that they can sell and then comfortably become buyers themselves; and they need to get to a point where they aren’t hanging on to their homes longer than they otherwise might have in hopes of extracting a higher profit.

One way to get there, perhaps counter-intuitively, might be to hope for a bit of a cool-down from the torrid pace of appreciation the market has been experiencing.

{kind=link}